Trending

Gen X has spent most of adulthood being told two contradictory things:

-

You’re on your own.

-

Don’t worry, it’ll work out.

We are the generation that got a front-row seat to every American system slowly turning into a choose-your-own-adventure… with many of those routes leading to surprise fees.

-

College for kids? Congrats, you’re the co-signer.

-

Retirement for you? Here’s a 401(k) and a shrug.

-

Healthcare for all generations of your family? Please hold while we drop you into a maze.

I recently had a conversation with a mentor of mine, aging policy expert Howard Gleckman. He is my go-to authority for quick interpretation of state and federal policy changes that impact my clients. This time, I asked him to paint in broad strokes for Xers and young Boomers to understand what’s coming.

“Nobody’s coming”

When I asked Howard what Gen X needs to understand about aging policy, he didn’t lead with Medicaid eligibility charts or budget line items. He led with this:

“You should assume nobody is coming to help you.”

Howard is not being nihilistic. He’s telling us, don’t build your plan around government rescue. Build it around reality. And that reality has sharpened as the year turned.

The real retirement risk isn’t retirement

Most retirement planning still assumes a clean story arc:

work → stop working → enjoy yourself → fade out peacefully.

That’s not how aging actually works.

The real disruption isn’t retirement, it’s frailty—the period where someone is alive, cognitively or physically limited, and needs help. That’s the part that wrecks plans, marriages, finances, and adult children’s schedules.

Gen X doesn’t like to picture this but ignoring it doesn’t make it less likely—it just makes it more chaotic when it arrives.

Here’s the mental trap: we assume this is a “future us” problem. In reality, it’s already a current us problem, because it’s showing up first through our parents.

The big problem with our parents’ generation: House rich, cash poor

A lot of today’s older adults didn’t transition well from pensions to DIY retirement savings. Some never opened a 401(k) or IRA. Others saved too little. So they’re sitting on equity—but not liquidity.

They’re often in the same homes they raised us in. Great memories, bad stairs. Lots of home equity, not much cash. The practical question becomes:

How do you turn a paid-off house into care dollars without wrecking everybody’s life?

Then comes the part Gen X needs to prepare for because nobody’s coming: If your parents can’t pay for the care they need, a big chunk of that becomes your issue—financially, logistically, emotionally.

This is where AATM’s planners/procrastinators/crashers framework gets painfully real:

-

Planners have the hard talks early, do the paperwork, and map out the “if X happens then Y” plan.

Procrastinators (agers) wait for the hospital discharge planner to hand them a clipboard and a panic attack.

Crashers learn everything the week after something goes wrong—while trying to keep their job with no more PTO.

Howard’s point to me was simple and unsettling: building your expectations around expanded government support is a losing strategy in the current political and fiscal environment. Housing subsidies, middle-market long-term care options, broad-based supports—all of those are constrained and likely to stay that way. Instead, the default model is shifting to:

-

families doing more,

-

caregivers being unpaid relatives,

-

and gaps being filled informally, imperfectly, and under stress.

Once you accept that, your planning questions change.

Preparing for probabilities

Great financial planning incorporates the chance that something goes right along with the chance that something goes wrong. Yet many families who come to me for financial advice can’t get their heads around dealing with probability. They might be willing to pay for the illusion of certainty in an uncertain world, but that’s not realistic.

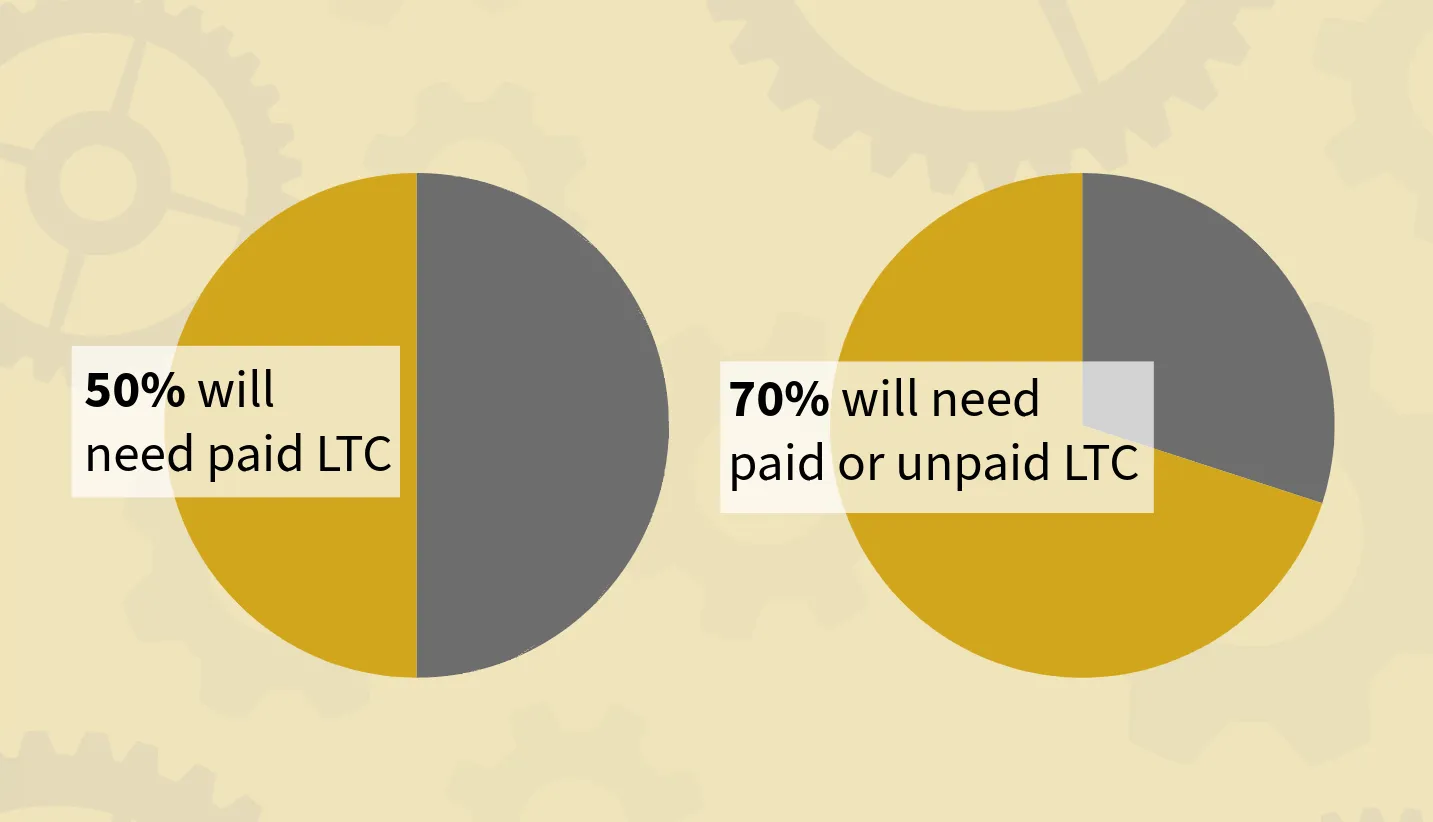

Here’s what’s realistic: Howard shared with me that we have a 50% chance of needing paid long-term care help and 70% chance of needing paid and/or unpaid long-term care help. Not only is no one coming, but you won’t be able to do it on your own.

Nobody’s coming, part II: You can’t get help even if you can pay for it

Direct care work (home care aides, nursing home aides) is facing a historic crunch:

-

COVID amplified a shortage of workers that was already trending down before 2020.

-

Increasing numbers of direct care workers are in their 50s and aging out of physically punishing work.

-

Stricter immigration policies are impacting the availability of immigrant workers who make up a large share of long-term care staff.

As Howard stated bluntly: Sometimes you can’t find a home care aide at any price.

I have already seen this in my older clients, and it leads to families patching it together. Children attempt to do long-distance caregiving, daughters disproportionately become caregivers, and everyone is worn out in the process.

Here comes prior authorization for original Medicare

The Centers for Medicare and Medicaid Services is implementing prior authorization requirements in traditional (fee-for-service) Medicare in select states beginning in 2026—something that used to be mostly a Medicare Advantage headache. This is one of those “sounds technical” changes that becomes very real when you’re trying to get a procedure approved for your parent or for yourself.

Howard’s worldview fits here: the system is moving toward more gatekeeping, not less. Sometimes for fraud control, sometimes for cost control, sometimes because we’ve all decided suffering builds character (I assume). For an even greater degree of difficulty, Medicare Part B premiums and Part D deductibles have moved upward for 2026, even while some protections (like the Part D out-of-pocket cap) remain in place. These changes all put more burden on caregivers to keep a close watch on premiums and out-of-pocket costs.

3 Things Gen Xers can do

None of this is easy, but it’s also not insurmountable. Whether you are a planner, procrastinator, or crasher, you are extremely likely to have to care for a parent and later need care yourself. There are three things you can do to know what you may deal with and be ready when that time comes.

-

Run a baseline scenario that’s realistic

Your planning should assume you will need to help your parents. You should also assume you will need help yourself. If you don’t, great! But it’s better to plan for “functional but frail” and not assume you’ll golf forever. -

Treat care as a core financial risk

Treat long-term care planning as a required part of your financial planning. It is as essential as what you have in your 401k or in your portfolio. All of that saving and planning will go poof if you slam into an unforeseen long-term care situation. -

Plan for friction and support

There will be paperwork. There will be prior authorization. There will be shortages for care workers. Design something that will still move forward when systems are bottlenecked. And think of your own emotional support to get you through all of this. Lean on friends and family, do what you need to ensure you get the mental relief you will need on occasion so you can recharge and regroup.

Gen X has always been good at adapting. The question now is whether we adapt early—or under duress. That’s one of the biggest reasons Age Against the Machine Exists: to help you choose the first option.

Related: 5 Sedating Lies We Tell Ourselves and the Toll They Take