Written by: Emily M. Harper

It may surprise you to hear that I, a financial planner, am not big on making New Year’s resolutions. In the past I’ve resolved to keep a house plant alive, and maybe this year I will try to feed my chunky lab less human food (it’s hard to say no to the Director of Mischief). These small optimizations feel good, help us improve ourselves and others, and encourage us to try new things – I love that many people embrace this! However, I prefer to focus on the big picture of what I want life to look like both now and in the future, and less on “what do I want to do this month or year”. This keeps me honest and disciplined about the consistent actions required to move the needle.

Successfully meeting long-term goals requires more than December 31st ambition. Whether you are accumulating wealth for goals like retirement or creating a legacy, enjoying the lifestyle that your wealth enables, or you just want to be financially unbreakable, consistent behavior is a key to success. Read on for some things to consider as the new year unfolds – recent legislation may change your approach to saving and investing for the long term.

Save & Invest No Matter the Environment

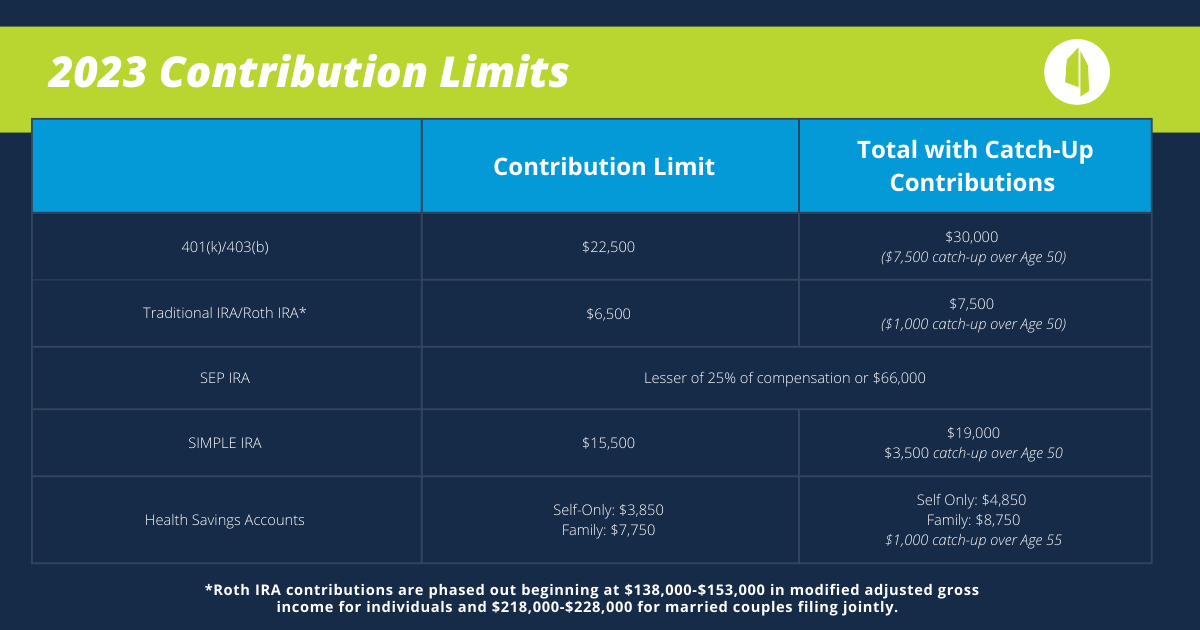

The start of the year is a great time to review current contribution limits for tax-deferred accounts like retirement accounts and Health Savings Accounts. Make sure you are set to effortlessly maximize these as you are able. Saving and investing consistently regardless of the noise in the world around us is easier said than done – I’m even guilty of accumulating more cash than I need for healthy emergency savings. Setting up regular automated contributions to retirement and even taxable investment accounts makes it more likely that we will continue investing and not get derailed when things get tough in the market like they did in 2022. Our behaviors are a key driver of success when the world around us is unpredictable and outside of our control.

Automating doesn’t mean set it and forget it…limits change annually (brutal inflation in 2022 had a silver lining in driving higher contribution limits for 2023), and the “Secure Act 2.0” passed in December 2022 as part of a broader omnibus spending bill makes things a little more complicated.

2023 Contribution Limits

What Changes with the “Secure Act 2.0”?

Provisions in the “Secure Act 2.0” are set to kick in over a number of years and will impact how we save for retirement. Not a whole lot is changing in 2023, but there are a few things to be aware of in the near-term as you think about your saving strategy. This is not an exhaustive list but contains the details most likely to impact you when it comes to both saving for the long-term and maintaining tax-efficiency.

A Focus on Roth Money for High Income Earners & Business Owners in Workplace Plans

One big change for self-employed individuals and small businesses in 2023 is the introduction of Roth SEP & SIMPLE IRAs. While Roth contributions won’t decrease your taxable income now, they will give you flexibility when it comes to tax planning in the future with the benefit of tax-free withdrawals in retirement.

Beginning in 2024, employees may also start receiving Roth matching contributions from their employer – these contributions will be included in the employee’s taxable income. Previously, employers could only make matching contributions on a pre-tax basis. Not all employer plans have a Roth option – but this may compel more businesses to include a Roth in their plan design.

Also beginning in 2024, those over 50 wishing to make catch-up contributions whose wages exceeded $145,000 in the previous year will be required to make them to a Roth source in their employer-sponsored plan. While this removes one tax-reduction strategy in the form of pre-tax contributions, catch-up contributions to a Roth source are still worth it when it comes to building wealth with tax-deferred (and eventually tax-free) earnings. There are a lot of nuances to this rule – best to talk through this one with us to see how this might apply to your unique situation!

Higher Catch-Up Limits to Maximize Savings

Starting in 2024, catch-up contributions for IRAs and Roth IRAs will increase with inflation in $100 increments rather than remaining a flat $1,000/year.

By 2025, catch-up contributions to workplace retirement accounts will increase even more for those between 60-63, allowing you to save more in what may be your highest-earning years. The enhanced catch-up will be the greater of $10,000 or 150% of the catch-up contribution amount from the previous year. Keep in mind that the Roth catch up rules will apply to those with wages above a certain amount (likely $145,000 adjusted for inflation).

Ability to Keep Tax-Deferred Funds Invested Longer & Enhanced Tax-Planning Opportunities in Retirement

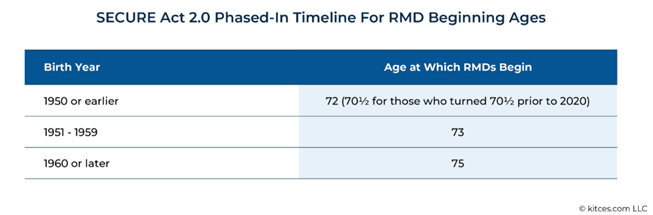

Starting this year (2023), Required Minimum Distributions (RMDs) will be mandatory starting at Age 73, one year later than under the original “Secure Act”. This will get pushed out even further to Age 75 by 2032. Because nothing is ever totally clear with legislation that gets jammed through the week of a holiday, inconsistent language related to this provision is creating some confusion. This handy chart from our friends at Kitces.com removes the guess work when it comes to knowing when you need to take an RMD:

By 2024, RMDs from employer-sponsored Roth retirement plans will no longer be mandatory, making these Roth plans more like Roth IRAs, where RMDs are not required. This will allow you to keep your Roth dollars invested longer if you still have money in an employer plan after you retire.

Qualified Charitable Distributions (QCDs) will still be permitted starting at Age 70 ½, allowing you more time before RMDs begin to bring your IRA balance down. Additionally, the current limit of $100,000/year for QCDs will start adjusting for inflation in 2024 – this represents the potential for significant tax savings for those retirees who don’t need their RMDs to maintain their lifestyles.

Focus on YOUR Big Picture – Don’t Follow Someone Else’s Recipe

While the importance of saving is universal, your vision and plans for the future are uniquely yours and require your own recipe for success. Those resolving to exercise more starting January 1st will see better results with a customized training plan they can stick with. Meeting your wealth goals is no different – facts and tips can never replace a customized plan built just for you. If you are into resolutions and haven’t made one yet, commit to 2023 being the year that you take stock of your big picture and determine if the actions you are taking are the actions that will successfully get you to where you want to be. If they are, great! Keep doing what you are doing and think about what else might be possible.

Related: Portfolios Should Never Be Set in Stone, but Strategies Are a Different Story