Written by: Jon Gumpel | Aubrey Capital Management

Well, 2022 has been quite the year, hasn’t it? Proving once and for all that things can change swiftly from impossible, to probable, to incoming.

As well as all the other more important, more extraordinary, and more bizarre things that happened this year, it has been the launch of Aubrey’s new defensive strategy that has kept me most busy.

March 2022 proved to be an interesting time to take over the Sentinel Navigator Fund mandate. This was followed, in September, with the launch of the Aubrey Citadel Fund, during one of the most extensive market repricing events seen for many years.

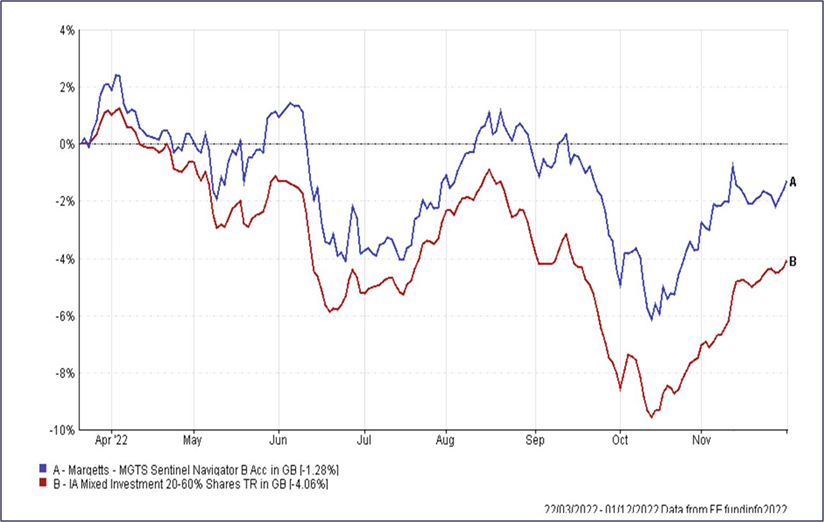

We managed to ride out volatility amid the repricing of inflation and political risks and I am pleased with the Strategy’s performance so far (see below[1]).

We are trying to construct the ideal defensive income growth portfolio and, by harnessing the defensive benefits of selected bonds and alternatives, together with the driving force of a portfolio of Aubrey selected global equities (demonstrating quality, value, and good income & growth prospects in various combinations), we think we are getting there.

We also seek to actively manage our exposures to take account of market fluctuations, with both constant small adjustments on the tiller as well as sharper moves if, and when required.

I see the point of a defensive manager is to focus on the un-priced risks ahead, and in particular on the key risks that could ruin the journey, while coping with day-to-day changes and flows.

We will not always be ahead of the pack or in line with the last quarter. There will be times when our solid qualities may not be in vogue, but we should always be adding value to both your returns and your portfolios on a risk adjusted basis. Furthermore, we aim to compound our income so that the starting yield of 3.4% can rise and help ameliorate the effects of inflation, without taking either the full risk of equity volatility or the inflation risk of simply holding a US Treasury bond.

I have been asked quite a lot why my focus is now on defensive income, why we are not in the Targeted Absolute Return sector and why I am at Aubrey.

My focus is on defensive income because in a world that has lost its compass on many things, and quite particularly in the investment world, a sustainable growing income is, I believe, the surest way to both maintain valuation discipline and to chart a course through the difficult waters ahead. I do not want my hands tied by anything that hampers the steering. The absolute return sector adds that burden on a manager and, while that was fine in the last 10-15 years of low inflation, it is not appropriate going forward. In an inflationary world, benchmarking to cash simply does not make sense.

For the same reason I think that equities, or rather a specific subset of global equities, is going to offer the best hope for enduring defensive income growth returns. That is why Aubrey is such a good home, with the ability to help me create a cost-effective portfolio of global equites to suit the environment. I have known some of the team here for a long time and quite apart from anything else it is a great group of people and a very nice place to work, which is an important thing in itself.

I think I may have exceeded the budget of time my readers have allowed, so I will end this note now with best wishes for a happy Christmas and a peaceful new year.

Related: European Equities: Towards Calmer Waters

1] Data from FE fundinfo 2022