Trending

Sometimes, it’s the most basic concepts and strategies that help advisors convey their value-add propositions. Said another way, advisors don’t always have to venture into the exotic to prove their mettle to clients.

Yes, there will always be those clients that want access to private credit, private equity, non-listed real estate and the like. That’s their prerogative and there is utility in those asset classes, but there are instances when the blocking and tackling of financial advice carries.

The intersection of women and retirement planning is a prime example of a simple avenue through which advisors can drive considerable value for clients. Smart advisors are already thinking along these lines because there’s no shortage of research documenting the trillions of dollars poised to flow from baby boomers to younger women via the great wealth transfer.

However, this isn’t solely about capturing great wealth transfer business. It’s more about helping female clients establish retirement foundations so they feel more educated and empowered. Fortunately, getting there can be accomplished with some basics.

Start in the Workplace

Advisors know that their female clients and prospects are in the workforce and that earnings power is rising. Where things get interesting is that many women aren’t taking advantage of employer-sponsored retirement plans.

Twenty-eight percent of women “working full-time, part-time or looking for employment didn’t contribute to their retirement savings between 2024 and 2025, compared to 18% of working men. The share of Black and Hispanic working women who didn’t put money away for retirement between 2024 and 2025 was even higher (33%),” according to Bankrate.

Reasons vary as to why so many working women aren’t engaged with workplace retirement plans, but it’s not a stretch to assume that lack of financial education and a long-held preference for conservative cash investments are among the top reasons. In either case, advisors can be forces for good while delivering to female clients basic, but vital information.

“Today, you can invest online with as little as a dollar in 401(k) plan, individual retirement account or Roth individual retirement account — and it can cost little to do it online from the comfort of your home,” adds Bankrate.

Every Little Bit Helps

As noted above, some women prefer to be in cash while others may not realize that they can invest, in a retirement plan or taxable brokerage account, with small amounts of money. Moreover, many would-be investors, regardless of gender, don’t realize that starting small is way better than not getting in the game at all.

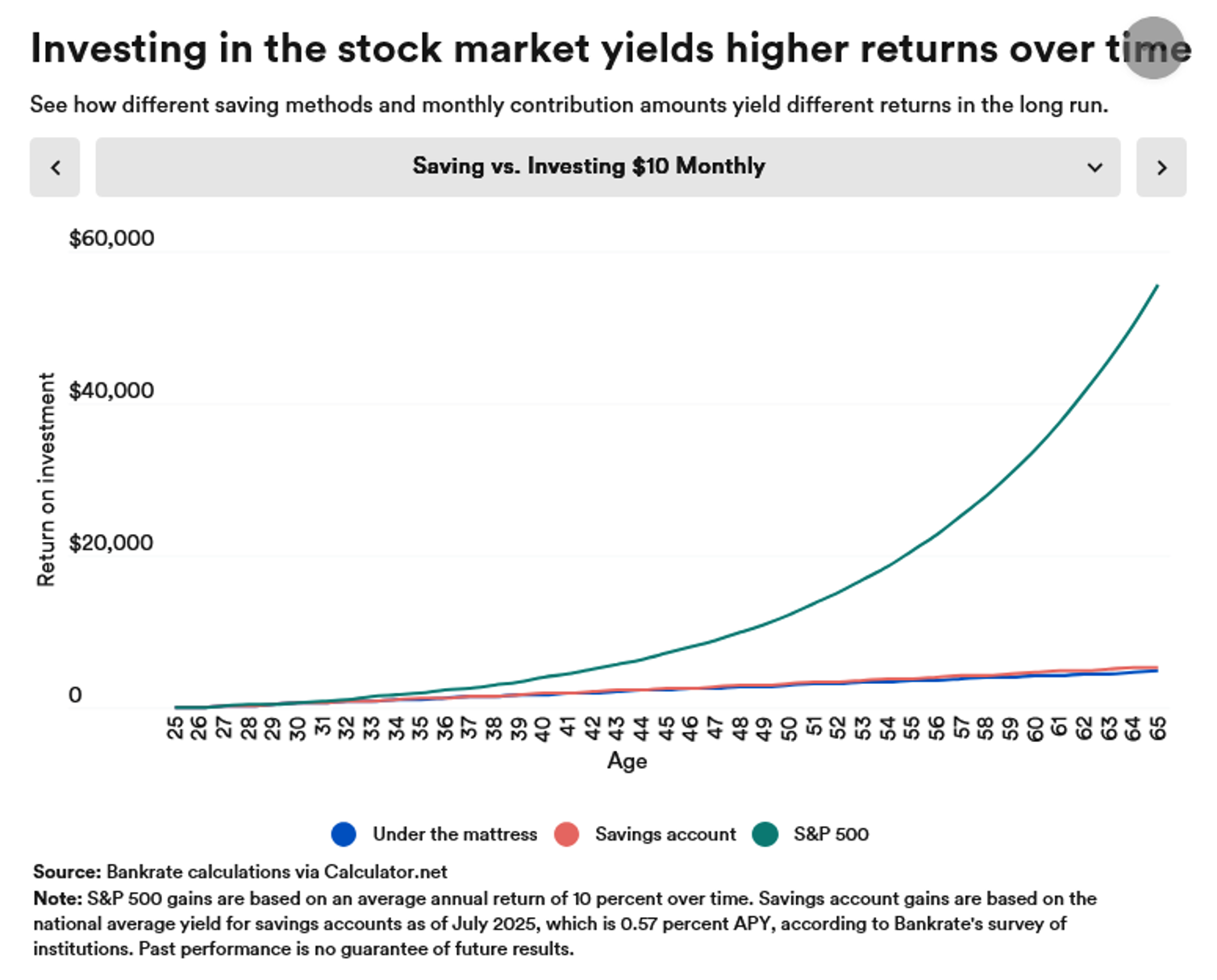

(Image: Bankrate)

That chart is important and is worth presenting to female clients because it shows the power of investing for the long-term – something studies indicate women are more apt to do than men. Said another way, women already have the advantages of perspective and prudence on their sides. They just need to capitalize on those traits and that includes, with the assistance of an advisor, exploring all the retirement account options they have, particularly if their employers don’t offer one.

“If you can’t access a 401(k) plan, other free options like IRA accounts are available. A traditional IRA allows you to contribute pre-tax money earned through income, but a Roth IRA works a little differently,” concludes Bankrate. “With a Roth IRA, you can only contribute after-tax dollars and there are income limits. If you like the idea of opening a traditional IRA or Roth IRA, look for a retirement provider with low fees.”

Related: Why Money Is Still More Taboo Than Politics—and What That Means for Your Finances