Trending

Written by: Adam Schrier | New York Life Investments

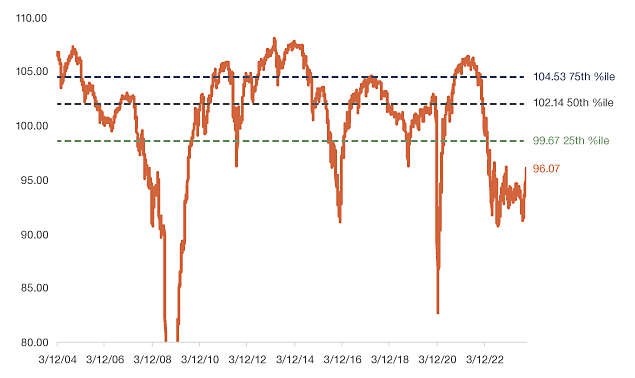

Bond prices declined in 2022 due to widespread market volatility that drove yields higher. As market yields increased, outstanding bond coupons became low relative to those market yields, resulting in bond prices below par. For short-duration high yield, an average price below par is not very common, occurring just 25% of the time over the last 20 years. This situation creates total return potential beyond just income. In a yield environment where short-term Treasuries are yielding over 5%, it is important for investors to consider total return when deciding on a fixed-income allocation.

Short-duration high yield, as represented by the ICE BofA Cash Pay High Yield (1-5 Year)(BB-B) Index, consists of relatively higher-quality, seasoned bonds or bonds that were issued at least a few years ago. Typically bonds with longer maturities have higher coupons than similar credits with shorter maturities. So as time passes, and high yield bonds move into the shorter-duration part of the market, their coupons will be high relative to their yield, which results in a premium, or bonds trading above par. This is why the median short-duration high yield price is 101.9. The current price is 96.1 — below the 25th percentile and six points below the median.

Figure 1: Current price opportunity: Price below 25th percentile

Source: FactSet, for the period 3/12/04-3/12/24. Short duration high yield represented by ICE BofA Cash Pay High Yield (1-5Y)(BB-B) Index. It is not possible to invest directly in an index. Past performance does not guarantee future results.

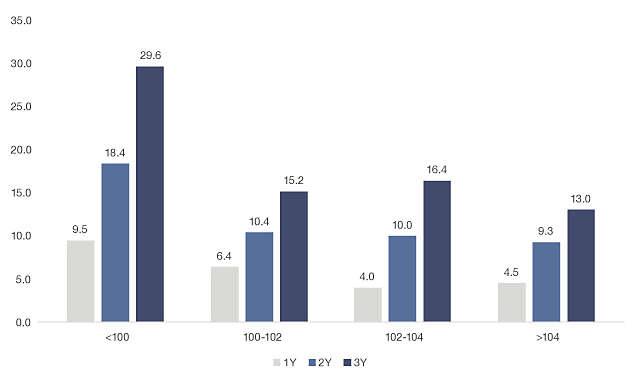

One of the ways bonds differ from stocks is that bonds have math on their side, due to coupons and maturities. As time passes, a bond becomes closer and closer to its maturity. In simple terms, a bond will either mature, or it will default, and if default seems unlikely, it will be “pulled to par” meaning its price will appreciate toward par as it nears maturity. Since short-duration high yield excludes CCC-rated bonds, which are the most likely to default, most of these bonds are pulled to par. Looking back 20 years, the median one-year forward return of short-duration high yield following a price below par is almost 10%. This is largely attributed to the avoidance of CCC-rated bonds as well as high coupons and short maturities.

Figure 2: Higher median returns when prices are below par

Source: FactSet 3/31/04 - 2/29/24. Short Duration High Yield represented by ICE BofA High Yield 1-5 BB-B Index.

When talking about high yield valuations and return potential, it is important to also discuss fundamentals. Within the U.S. high yield bond market, credit trends remain stable. The leverage level of high yield issuers is near historical lows, according to JP Morgan. During the pandemic, there was a massive wave of downgrades from investment grade into high yield, including three of the largest on record — Kraft Heinz, Ford and Occidental Petroleum. All three have already become “rising stars,” making their way back to investment grade. Similarly, the upgrade-to-downgrade ratio in the high yield market is above one, meaning credit rating agencies have been upgrading more bonds than downgrading. While this ratio has declined since its peak in 2021, it indicates that overall credit trends continue to be strong.

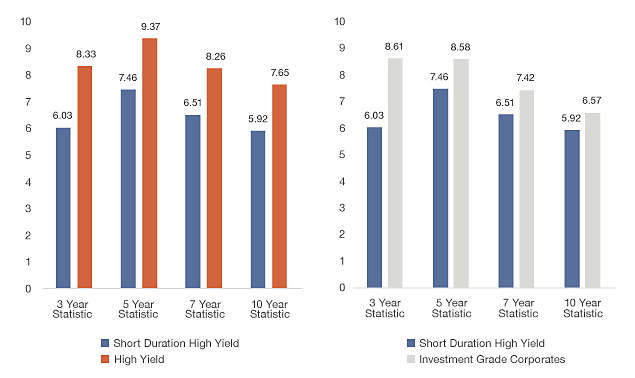

High yield bonds that are closer to maturity are less sensitive to rate moves. Similarly, spread widening and tightening impacts prices of shorter-duration bonds less than longer-duration ones. In 2022, the broad high yield market was down 11.2%, while short-duration high yield was only down 5.5%. For this reason, and the fact that the index excludes CCCs, is why the asset class can be characterized as a lower-volatility segment of high yield. Not only does it have less volatility than the broad high yield market, but it also has less volatility than investment grade corporate bonds.

Figure 3: Short duration high yield has had less volatility than both the high yield market and investment grade corporates

Source: FactSet, as of 2/29/24. Short duration high yield represented by ICE BofA Cash Pay High Yield (1-5Y)(BB-B) Index; US Corps IG represented by ICE BofA US Corporate Index; High yield represented by ICE BofA US High Yield Index. It is not possible to invest directly in an index. Past performance does not guarantee future results.

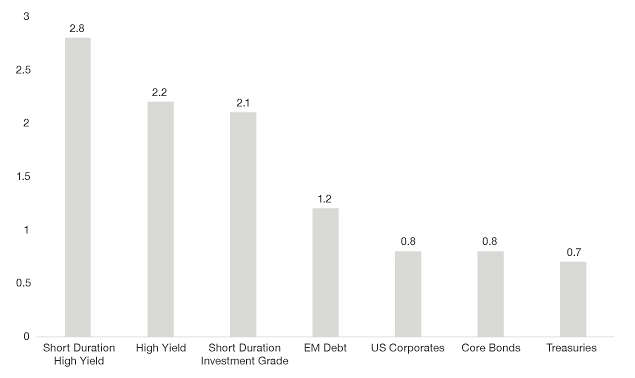

Short-duration high yield can be considered an “all-weather approach” to high yield investing because of its lower-volatility profile and higher quality bias — it has tended to be more resilient than the broad market. Historically, it has generated a greater yield per unit of duration than most other areas of fixed income, including short duration, investment grade corporates, emerging-markets debt and core bonds. Therefore, this asset class can be used as a “through-the-cycle” holding to generate income and provide diversification.

Figure 4: Competitive yield per unit of duration compared with other areas of fixed income

Source: FactSet as of 2/29/24. Short Duration High Yield represented by ICE BofA High Yield 1-5 BB-B Index. High Yield represented by ICE BofA U.S. High Yield. Short Duration Investment Grade represented by ICE BofA U.S. Corporate (1-5 Y). EM Debt represented by JP Morgan EMBI Global Diversified. U.S. Corporates represented by ICE BofA U.S. Corporate. Core bonds represented by Bloomberg U.S. Aggregate. Treasury represented by ICE BofA U.S. Treasury. It is not possible to invest directly in an index. Past performance does not guarantee future results.

With investors paying more attention to the longevity of short-term yields and reinvestment risk, they are looking to step out of cash while keeping a watchful eye on risk. Given its rare discount, short-duration high yield may be the right mix of quality and return potential that advisors are looking for in order to start shifting away from cash.