Trending

There’s too much leverage in portfolios… so buyout returns must be doomed

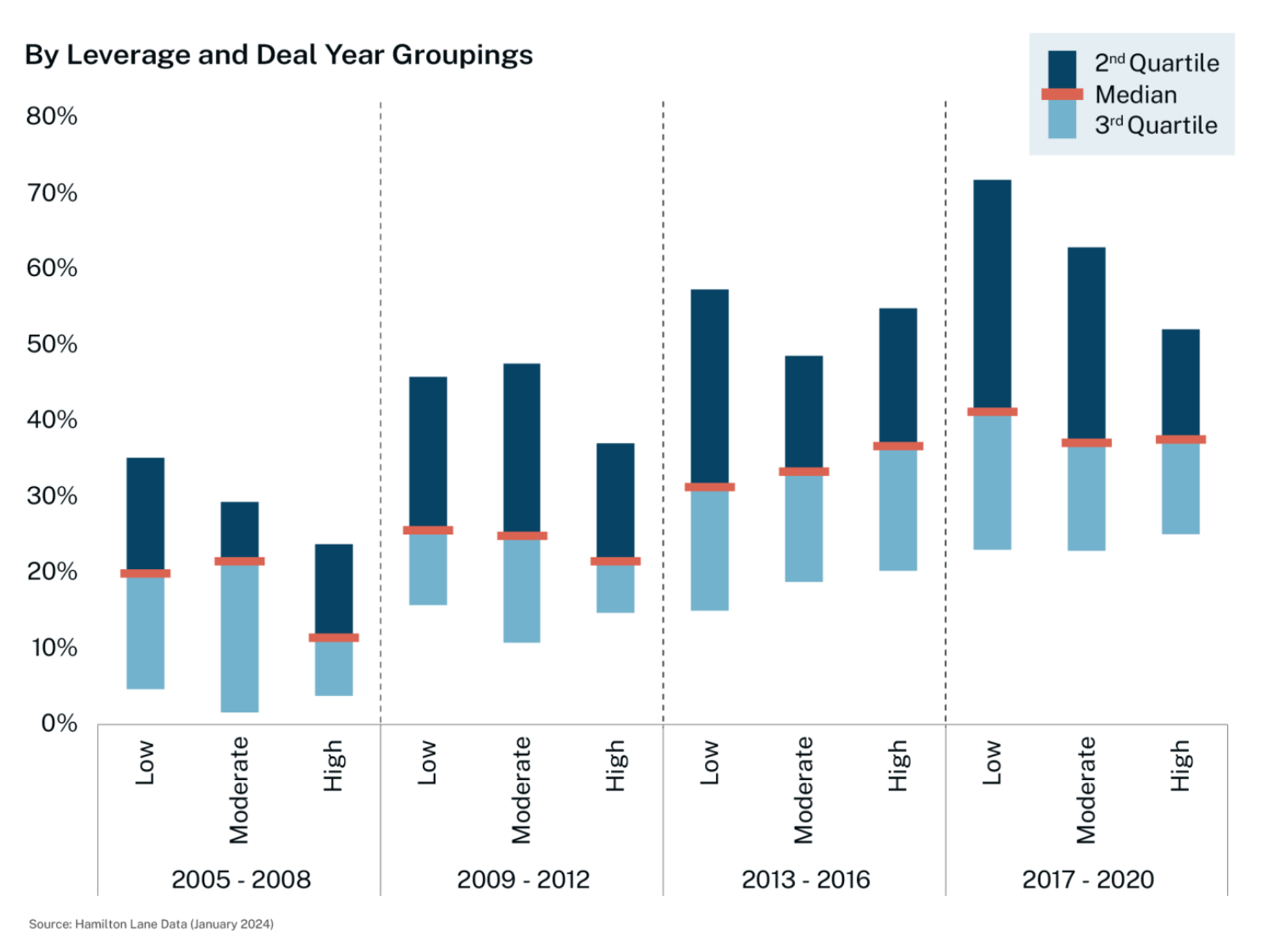

This is an argument we hear often. Today, it is based on the premise that higher rates, coupled with the higher leverage levels being taken, means buyout returns will suffer drastically. Yes, there has been an upward trend in acquisition leverage multiples, but we haven’t moved a lot over a longer timeframe like the last 15 years. Our data shows median net debt / EBITDA is around the 5.0x mark right now. So yes, there is leverage – but is it so excessive that it can hinder return outcomes altogether?

This week, we look at returns of realized buyout deals by leverage and deal year groupings.

No, your eyes don’t deceive you; there is indeed a significantly lower dispersion of returns for highly levered deals across all cycles. Fascinating. Returns don’t appear to be consistently better for one level of leverage versus another. Sure, pre-GFC, high leverage levels hurt returns, but is that an environment we believe will return?

Interestingly, while lower leverage produced better returns, it was not so much better that you can conclude that high leverage in itself means returns will suffer.

Catch up on Chart of the Week.

Related: Private Market Outlook Amidst Macroeconomic Uncertainty

Definitions: Corporate Finance/Buyout: Any PM fund that generally takes control position by buying a company.