Trending

How you pay the advisers in your business can be the source of many of your problems. And I’m not only talking about self-employed advisers here.

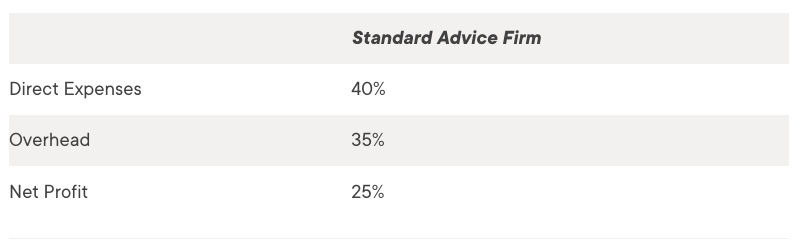

Let’s start with the basic maths of a financial planning business:

- Your direct expenses (i.e. what you pay away to selling directors and advisers) shouldn’t exceed 40% of gross revenue.

- Your overhead (i.e. every other cost of running the business) shouldn’t exceed 35%. That’s really hard to hit.

- Your net profit is then 25% of your gross revenue, AFTER everyone in the business, including the owners, gets paid a full whack market salary for their day job.

Here’s The Problem

If you pay away too much revenue to advisers it’s clearly a problem. However, I’m going to argue that the real problem is advisers getting paid variable remuneration.

Even in many good financial planning firms, advisers are paid a lower fixed salary and then some form of variable remuneration (a bonus) for hitting certain levels of revenue that they manage. Typically that includes ongoing remuneration and any new business income generated.

Why does variable remuneration cause unnecessary problems?

Let me work through two different examples to illustrate:

a. Disengaging from smaller clients

Most firms at some point on their journey have to address the small client issue. The decision eventually gets made to elegantly disengage from some of their smaller or legacy clients.

That might mean they get sold off as a bundle to another firm, or it might be as simple as resigning as the servicing adviser and letting go of any entitlement to ongoing remuneration.

Even when the owners in the business decide that disengaging from their smaller clients makes sense, they can run into resistance from the other advisers in the firm. There can even be disagreement among the owners themselves.

The driver of this resistance?

How the advisers get paid.

If advisers get a basic salary and a bonus that’s calculated on the total revenue that they manage, then when you explain that you’d like them to let go of some clients, all they hear is that you’re asking them to take a pay cut. No amount of education or explanation can get them to budge from this position and it’s all because of how they’re paid.

b. Moving clients between advisers to improve productivity

When you are trying to generate more productivity and make life more fun for yourself or your existing advisers, it often makes sense to move the client load around. There’s no point in having one adviser at maximum capacity when other advisers still have room for more clients.

Instead of waiting five years or more for newer advisers to get to maximum capacity one client at a time, why not have yourself or your senior advisers pass across the bottom 50% or even two-thirds of your client book to less busy advisers?

The experienced adviser can retain the top half or one-third of their clients, which may still account for 66% – 75% of the income.

Now the newer adviser is productive and the experienced advisers are freed up to see the biggest and best new leads that come through the door. They’re no longer maxed out.

The driver of resistance to this approach?

How the advisers get paid.

Why don’t you want to hand over clients?

There are emotional issues for sure, however, the biggest sticking point is often around money. For example, do you believe you’d have to pay the junior adviser some fixed percentage of the new higher revenue that they manage and that this is uncommercial?

Can you see how remuneration is getting in the way of a good decision?

The Solution

Stop paying advisers variable remuneration.

Let’s say you currently pay an adviser a base salary of £30,000 and a production bonus of 35% of all revenue above £90,000 (i.e. a 3x salary qualification level).

Let’s also assume that if you sat down with the adviser you can estimate their total production for this year within a relatively small margin of error and it comes in at £200,000 of total revenue.

So they’ll get paid £68,500 this year give or take.

Why not tell your adviser how much you value them and that you’d like to give them another chunk of clients to look after. The new chunk of clients will be another £250,000 of annual revenue (the bottom half of your own client bank).

You’re also going to move them onto a salary package of £100,000. No variable component. Just paid monthly.

All they have to do is keep the clients happy and slowly build the revenue stream by handling any new work that arises.

There’s no mention of percentages of revenue. There’s just a fair salary for an important job in the firm.

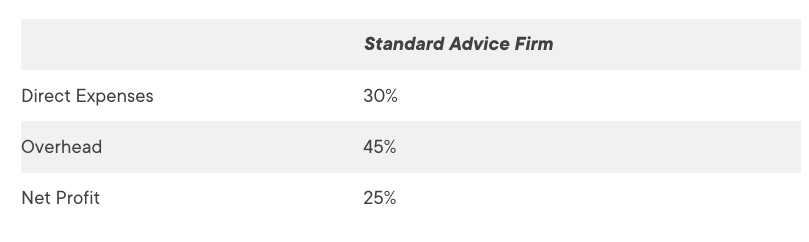

As it turns out, you’ve now lowered your direct expenses for this adviser to 22%. Well below the 40% maximum outlined earlier. Some of the savings can be spent on more support staff – admin, paraplanners etc – to keep all the advisers in the firm uber-productive, focused on sales and client relationships.

The effect on your business numbers is significant as it starts to reduce your direct expenses whilst allowing you to increase your overhead. Your numbers might now look like this:

How is this of benefit?

Well, it means you’re paying your people well without silly targets and bonus structures that create unintended consequences. People feel respected in your business.

And you have more revenue to spend on valuable support staff that makes life fun and enjoyable for the advisers in your firm because they don’t have to handle that admin and paraplanning work. They spend more time in front of clients – the bit they enjoy the most.

Yes, your overhead percentage is higher, but you still hit your 25% net profit target because your direct expenses (money paid to advisers) are under control.

Get rid of the variable remuneration. It’s a hangover from a bygone era.

Let me know how you go.