Trending

If you have known me for any time, you know that I generally eschew the annual forecasting published by all the major firms and their strategists.

Why?

My opinion is that it’s nothing more than guessing. But that doesn’t mean it’s not fun to review or think about, so I’ll go over some of the predictions and compare them to the previous year’s forecasts (to the extent I can go dig them up – but I’m saving them all this year to use next year).

Let me just get this out of the way…it’s kind of unfair of me to pick on these forecasts, and here’s why.

The publishing analysts and their whole team are intelligent, professional, well-educated, credentialed, and impressive. I hold them ALL in the highest regard. Forecasting is what they do, and all of their research reports are grounded in rigorous research and analysis.

I hold all of these folks in the highest regard. I read what they write, and I deeply appreciate their reasoning for these annual forecasts.

But…I don’t believe it should be used as “actionable advice” in and of itself.

But let’s review them because, well, it’s fun and educational.

Goldman Sachs

Goldman publishes from two different groups: their Investment Services Group (ISG) and Global Investment Research (GIR).

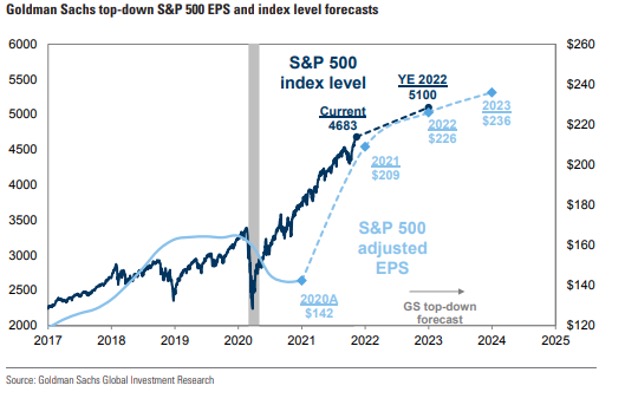

David Kostin writes the annual outlooks for GIR, and he and his team have forecasted the S&P 500 index will climb by 9% to 5100 at 2022 year-end …so that’s a prospective TOTAL RETURN of 10% when you include dividends.

They predict that S&P 500 earnings per share (EPS) will grow by 8% to $226 in 2022 and 4% to $236 in 2023. Not bad. (See below for the chart from the report.)

JP Morgan

Marko Kolanovic published the JP Morgan (JPM) Global Markets Outlook in early December and has the S&P 500 finishing up 2022 at 5050 and EPS coming in at $240. So their index level forecast is close to Goldman’s, but they are forecasting a much higher EPS. Their estimate for the 2021 S&P 500 index level was the highest on the street at 4700.

So as JPM looks ahead, they see moderate market upside on better than expected earnings growth.

LPL Financial

I love LPL research…it’s elegant in its simplicity, and their analysis is easy to read and relatively jargon-free. But don’t make the mistake of thinking that it’s not the output of serious analysis.

They just have their own style…just like we do, and I like it.

They publish their stuff to the public, which I think is cool. You can follow it all on Twitter: @LPLResearch, Ryan Detrick @RyanDetrick, and the very sadly retiring Burt White @_BurtWhite.

LPL is forecasting the S&P 500 to end 2022 between 5000 and 5100…so in line with JPM and Goldman. Their EPS forecast is coming in a little lower than the others at $220.

SO WHAT?

Again, I love the forecast reports that come out at the end of the year, and it’s all based on good solid, intelligent thinking. Said differently, none of it is grounded in stupidity.

But…

It’s still all guessing. Educated guessing, and fun to read, but guessing nonetheless.

And that’s a problem for anyone who uses forecasts as an investment decision-making tool to adjust portfolios.

Ok, by now, you get it…you know we eschew the actual forecasting. But if you KNOW us, you also know THIS about us – we provide unfiltered opinions and straightforward advice.

SO, here it is.

Our philosophy is centered on determining where the greatest odds are in your favor. That’s it…much like a casino can’t control the short-term volatility of gamblers’ hot streaks at the craps table, the casino knows that the odds of positive returns are in their favor over time, and they stick to those odds.

So are the odds suitable for investors? We think yes.

It’s our opinion that we are in the middle stage of an economic cycle. The Fed usually starts raising rates towards the end of the economic cycle, so because they are not yet raising rates, it stands to reason we are not in the late stage of the economic cycle.

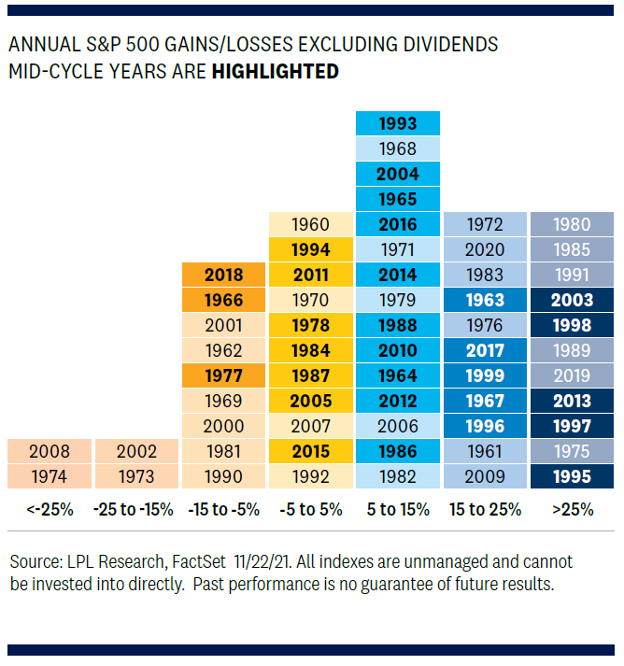

In looking at the past 60 years, the S&P 500 Index was up an average of 11.5% during the 30 mid-cycle years identified, and 80% of those 30 years had positive returns. (See chart below – the highlighted years are considered mid-cycle years.) 1966 and 1977 were the only two years with double-digit losses (2018 was a loss but not double digits).

It’s widely believed that the Fed will not start to raise interest rates until 2023, so we are confident in our opinion that we are mid-cycle.

BOTTOM LINE

Take a look at the skew of returns below – it’s showing that the odds are in favor of investors being in the equity markets.

Don’t mess around guessing next year…be in the market because we believe the odds are in your favor.

Of course, there is the chance that odds go against you, BUT that’s where a solid plan comes into play. A good plan should account for those times that the odds go against you. That means a reliable cash flow plan and resources to fund your cash needs in times when things don’t go as planned.

Get help creating a plan! (Pro tip – an asset allocation and portfolio is NOT A PLAN.)

KEYS TO REMEMBER FOR 2022 (AND ALWAYS):

- Don’t risk what you have and need for what you don’t have and don’t need – a good plan helps with this.

- Be financially unbreakable – have the resources available to fund your cash needs during market downturns, so you don’t have to sell investments when they are down.

- The market has had a great run. LOOK AT YOUR CASH NEEDS AND RAISE THEM NOW. Nothing will make you happier than seeing your cash needs sitting nicely in your account when the market goes down. Bonus – if you don’t need that cash when the market sells off, you can buy the dip.

As for Monument’s strategies, we continue to follow our rules-based models that guide us by facts rather than emotions and speculation.

This first appeared on Monument Wealth Mangement.

Related: Real Opinions vs. The Ivory Tower of Zero Accountability