Trending

The Bucket Plan™ can be a crucial part of the way ahead.

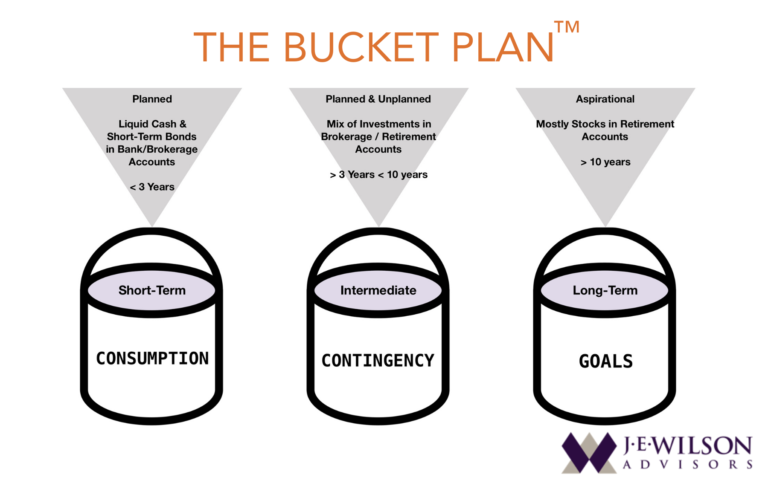

Following this structure can help reverse the current state of anxiety so that your emotions can begin to calm. Thinking of your investment portfolio as three discrete parts helps you regain focus on your longer-term objectives. The three segments of The Bucket Plan™ are titled Consumption, Contingency, and Goals. These buckets are allocated to short-term needs (Consumption), intermediate term expenses (Contingency), and long-term (Goals).

The Bucket Plan™ is designed primarily for those investors with retirement on the horizon or already retired. The concept revolves around connecting particular parts of your portfolio with specific goals and timeframes. The Bucket Plan™ acknowledges that markets move both up and down without a predictable pattern.

Since it’s impossible to know if stock prices will rise or fall in the short-term, it’s prudent to allocate a portion of the portfolio to low risk, fixed income investments. The Planned segment of the overall portfolio will be what you rely upon for anticipated expenses with a timeline of three years or less. The reasoning for this timeframe is based on market history. Since the end of World War II, there have been 15 bear markets (defined as a drop of roughly 20%) in 75 years. The longest of these market declines was just over three years in duration and the average length was a little more than one year. If you have at least three years of planned expenses in short-term, fixed income investments, this should alleviate concerns about short-term stock market fluctuations because you aren’t relying upon these to meet current needs.

The next portfolio bucket is dedicated to Planned & Unplanned needs with an expected timeline of three to ten years in the future. Within this bucket you should include a diversified mix of investments, including stocks. This segment of your portfolio is mainly oriented to growth but also recognizes the need for income from dividends, interest, and capital gains.

The third bucket is fully dedicated to long-term aspirational Goals at least ten years into the future. The grand majority of this portion of your portfolio should be invested in stocks since you can be historically confident about stock values increasing over that time period.

A Place and a Purpose

When you combine all three buckets into a portfolio you may have 40-80% stocks and 20-60% fixed income depending upon your stage of life and particular goals. Each bucket has a discrete purpose so it’s important to look at the investment performance of each bucket from that perspective. That is, in heady markets, the tendency is to cast shadows on the lower risk, fixed income bucket. Conversely, in periods of short-term market distress (like the present), many investors dislike riskier investments. Just remember both have a place and a purpose.

The opposite of panic is calm and that’s the desired outcome of The Bucket Plan™ . Making financial decisions in an environment free from the stress of today is a vitally important part of the way ahead. Start there.