Trending

Digital Money was the title of TBAC’s April 30, 2025, presentation to the U.S. Treasury Department, and an important topic worth discussing. TBAC, short for the Treasury Borrowing Advisory Committee, is comprised of senior investment professionals from the largest banks, brokers, hedge funds, and insurance companies. Most often, the committee informs the Treasury staff on market conditions and makes recommendations on debt issuance. The group’s recommendations typically carry significant weight with the Treasury. At its most recent meeting, the TBAC discussed digital money, better known as stablecoins, as a “new payment mechanism” that can benefit the Treasury by generating “materially heightened demand” for Treasury bills.

Given that digital money is now a reality and the TBAC is advising the Treasury Department on it, it’s worth summarizing the TBAC report and discussing how it may impact the Treasury bond market and change the financial system.

For more information on digitizing assets, which may help you better understand stablecoins, we recommend reading our article: Tokenization: The New Frontier For Capital Markets.

What Are Stablecoins?

Stablecoins are a unique type of cryptocurrency designed to maintain a constant value. Unlike most cryptocurrencies, such as Bitcoin, which fluctuate wildly in value, stablecoins aim for near-zero price fluctuations. Typically, stablecoin values are pegged to a currency, such as the US dollar.

Because their value is nearly constant, stablecoins are much more suitable for digital transactions than other cryptocurrencies. Like the roles of money market funds and savings/checking accounts in the traditional financial ecosystem, stablecoins serve as a store of value in the digital currency ecosystem.

To achieve stability, stablecoin issuers collateralize their tokens with dollars, Treasury securities, repurchase agreements (repo), and other assets. Among the most well-known stablecoins are Tether (USDT) and USD Coin (USDC). They are widely used in decentralized finance (DeFi) and for cross-border payments due to their low volatility and compatibility with blockchain networks.

The graph below indicates that over 80% of the assets backing Tether consist of cash, cash equivalents, and other short-term deposits. The remaining 20% are in assets that are riskier than most money market funds can hold.

Stablecoins offer faster and cheaper transactions versus the traditional banking system. They also facilitate financial inclusion for individuals without access to conventional banking services. Lastly, they serve as a form of “cash” in the cryptocurrency world, allowing for digital transactions or simply holding funds within the digital marketplace without a minimal risk of fluctuating value.

Per the TBAC report:

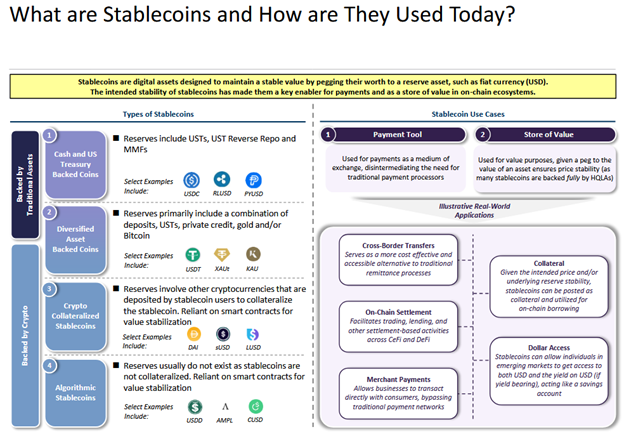

Stablecoins are digital assets designed to maintain a stable value by pegging their worth to a reserve asset, such as fiat currency (USD). The intended stability of stablecoins has made them a key enabler for payments and as a store of value in on-chain ecosystems.

The graphic below, from its report, shows that some stablecoins are incredibly secure, as they are backed by Treasuries, Repo transactions, and money market funds. However, as you move down their graphic, others use riskier assets such as algorithms and smart contracts.

Benefits To The Treasury

The TBAC presentation discusses how stablecoins might benefit the Treasury.

According to a diagram in the report, as shown below, there is currently approximately $234 billion worth of stablecoins. TBAC believes the number could multiply to $2 trillion by 2028. They think that roughly $120 billion of Treasury Bills collateralize stablecoins today. Furthermore, based on its $2 trillion estimate for stablecoin growth, they believe over $1 trillion of Treasury Bills could be used to support future growth.

If true, such an influx would mean that stablecoin issuers would own more Treasury securities than the UK ($779 billion) and China ($765 billion), the second and third-largest sovereign holders of Treasuries. Only Japan would hold more, with $1.13 trillion.

Shifting Treasury Issuance Patterns

The TBAC views the increased demand as a positive development for Treasury financing. In their mind, it could potentially lower yields by providing a new buyer base. Furthermore, diversifying from foreign buyers better supports U.S. fiscal stability and strengthens the dollar’s global dominance.

An additional $1 trillion demand for Treasury Bills would likely require a shift in how the Treasury issues debt. An increase in the supply of Treasury Bills to meet the new demand would result in less issuance of the longer-term maturities. Everything else being equal, that outcome should lead to lower, longer-term interest rates. However, shifting more issuance to shorter from longer maturities introduces risk. For instance, it could be costly if the yield curve inverts and short-term rates exceed long-term rates.

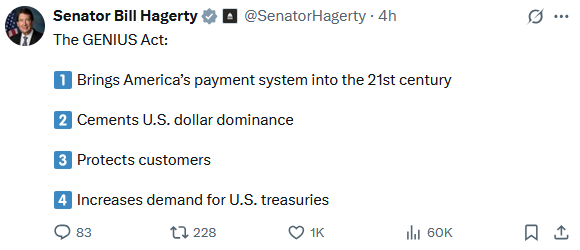

The GENUIS Act

The GENUIS Act, legislation proposed in February, requires stablecoin issuers to maintain reserves on a one-for-one basis with high-quality assets. GENIUS stands for Guiding and Establishing National Innovation for U.S. Stablecoins.The act explicitly mentions US Treasury Bills with a maturity of less than 93 days. Moreover, the act tries to limit the ability of stablecoins to offer yields.

The following tweet from the bill’s sponsor, Senator Bill Hagerty, summarizes the benefits of the proposed GENIUS Act legislation.

Bank Risks

While the Treasury may benefit from the new demand, the banks may suffer as a result. If stablecoins offer competitive yields, some traditional bank customers may opt for the convenience of digital stablecoins. Thus, banks would have to increase yields to keep deposits with the bank, or risk losing a vital funding source.

Bear in mind that banks use deposits to make loans. Thus, lower levels of deposits could result in fewer long-term loans and, therefore, slower economic growth.

The Fed

The Fed is currently able to use interest rates and its balance sheet to significantly impact bank lending, which in turn directly affects the money supply. However, keep in mind that the Fed doesn’t print money. Instead, all money is lent into existence. The Fed provides reserves to banks, which incentivizes them to lend money.

If banks play a lesser role, the Fed’s ability to impact the economy through its reserve operations may be reduced. While it has less control over the money supply, it could also be more challenging for the Fed to support non-banking crypto institutions during a crisis.

To help avoid a crisis caused by stablecoins, the government will need to enact strong requirements regarding the type of collateral and the amount of reserves backing stablecoins.

Summary

The Fed and the US Treasury will do everything in their power to ensure the US Treasury achieves the lowest possible funding costs. As we wrote in our Daily Commentary in May, Bank Regulators Will Help The Treasury:

Per an article in the Financial Times titled US Poised To Dial Back Rules Imposed In Wake of 2008 Crisis, US bank regulators are preparing to reduce bank capital requirements. Of particular interest to the bond market is the supplementary leverage ratio, better known as SLR. Unlike other risk-based capital rules that banks adhere to, SLR applies a minimum capital requirement to all bank balance sheet assets. The rule was put in place in 2014 to limit excessive leverage.

Reducing leverage ratios for the largest banks will enhance their ability to hold more Treasury securities. Similarly, stablecoins, backed by US Treasuries, offer another source of funding for the Treasury.

Stablecoins and the concept of digital money represent a significant shift from the current system. While there are lots of risks with digital money, there is also promise. Lower transaction fees and quicker transactions are two such benefits. Of course, as we mentioned earlier, a new buyer for US Treasuries is another significant benefit.

Related: Sell in May and Go Away: Myth, Mistake, or Market Strategy?