Trending

Presented by: Bob Keebler, CPA/PFS, MST, AEP, CGMA | Keebler and Associates, LLP

Webinar Replay:

The 2022 SECURE 2.0 Act provides incredible sales opportunities for financial and wealth planners, but every planner will need to master the important new rules contained within the bill.

Read on to discover the most significant aspects of SECURE 2.0 and how you can utilize the new legislation to help strengthen your clients' financial readiness for retirement now and in the future.

Bob Keebler: Today we're gonna talk about a bill President Biden signed into law on December 29, 2022. Let's call it SECURE 2.0 for easy, easy math. SECURE 2.0 is going to affect your individual clients for their retirement. It's going to affect people that are already retired.

Some of the provisions affect public safety, military individuals, nonprofits, and educators. There's gonna be disaster relief we'll go through, we'll talk about some areas related to employer plans and technical notices.

This course is going to focus on what the practitioner helping wealthy individuals needs to know. I'm not going to spend a lot of time with what to do if you're a plan administrator, or what it means to you. This is going to be geared for the CPA, the PFS, the CFP, or the financial advisor that's there every day in the trenches with real families that need help.

We're going to discuss the following aspects of the SECURE2.0 Act and how it impacts:

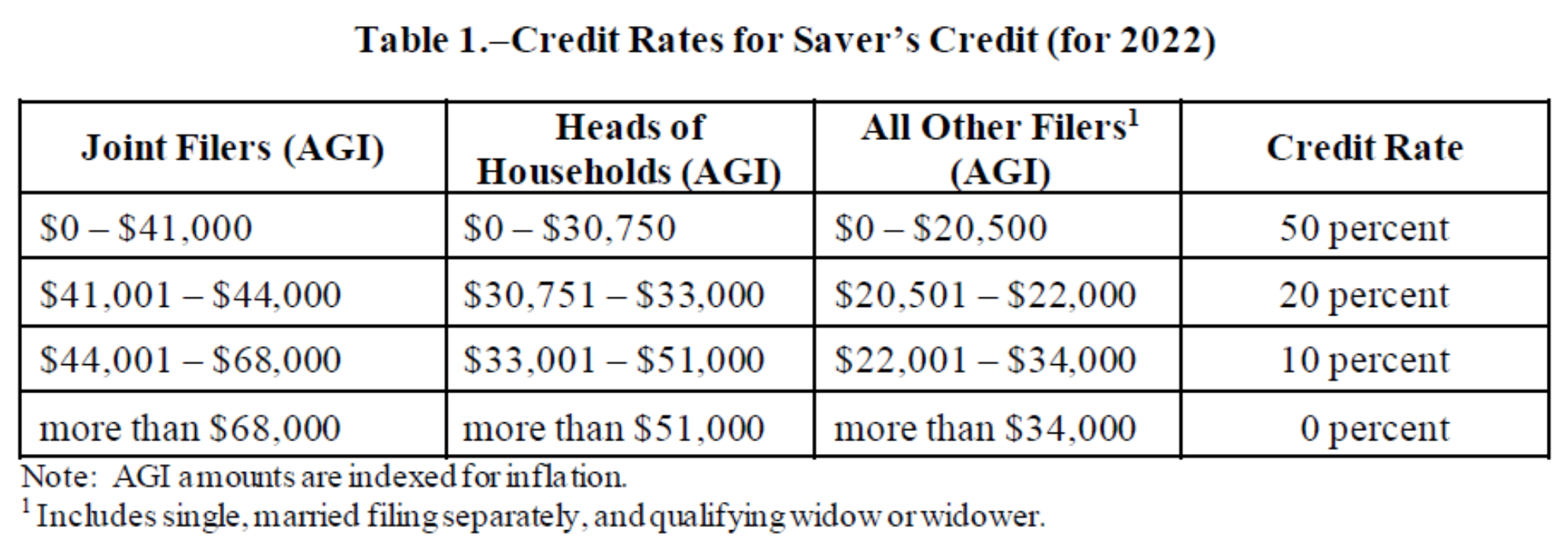

Changes to the Saver's Credit

First of all, a small change, but there will be a Saver's Credit change where you're going to be able to get a credit based on your income and how much you save now. The current law (Act § 103) is represented on the table below. You can see once you hit $68,000 you can't get this credit any more.

Now, looking at this though SECURE2.0 takes away the credit and provides a match. Basically, this refund would be treated as a direct contribution to your retirement account.

We don't know exactly how that's going to work from a practical perspective, because it's going to take time to implement. The change begins in 2027. But just know that this credit exists, and it's changed. And a lot of these changes are going to impact your work, so keep a running list of how this might impact financial projections you're doing for clients now.

Changes to the Saver's Match

- Refund made as a direct contribution to a retirement account

- The credit would also be restructured:

- Equal to 50% of up to $2,000 (not indexed) of contributions

- Includes any elective/voluntary contributions; reduced by distributions over a 2 year testing period

- The 50% rate would be phased out to 0% based on a MAGI range (indexed for inflation):

- MFJ: $41,000--$71,000

- HoH: $30,750 --$53,250

- Single: $20,500--$35,500

- Taxpayer must have attained age 18 and not claimed as a dependent

- Effective in 2027

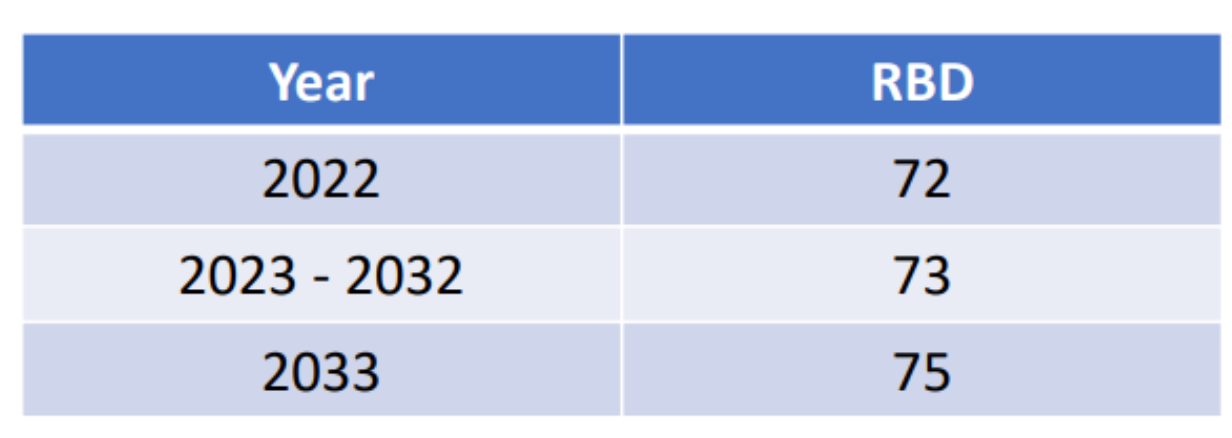

Required Beginning Date (RBD) Increase

If you're going to be in a 12%, or 22%, or 24% rate on your journey to age 75, and then at age 75, those RMDs are going to kick you into a higher rate, you probably should be doing Roth conversions along the way.

Because you see, it's all about bracket management. You're going to have two or three types of clients:

-

You're going to have clients who have been good savers outside of all their plans? maybe they have a really nice pension or maybe they're still working. Those clients are not going to need this money to consume, it's going to pass to their children. That type of client is probably more likely to be looking at Roth conversions, etc.

-

You're also going to have clients that spend every penny they can get, then in all likelihood, they're not going to have access to capital. Those clients will likely be drawing on their IRAs earlier. But you still want to look at how do you avoid flying into the eye of the storm and being in a 22% bracket at age 65, 70, and 74 for those clients, and then suddenly jumping into a 32%, or 35%, or 37% bracket.

Now, you also have to remember that the current tax brackets sunset on January 1, 2026. As part of the Tax Cuts and Jobs Act, we go back to that 39.6% rate. So again, we have to learn to do the new calculations here.

Indexing IRA Catch-Up Limit

Under Section 108 of the bill, taxpayers over age 50 can contribute an additional $1,000 to their IRA annually. That's current law. This applies to both Traditional and Roth IRAs. The $1,000 limitation is not indexed for inflation. All this does is indexes the catch-up limit for inflation. This is effective starting in 2024.

So this year, you might be able to put $7,000. And next year, it might be $7,100 or something similar. Now, if inflation is 9%, it will likely be much more than a $100 increase? something like a $700 increase probably rounded in $1,000 increments.

You want to be aware of this in order to help your clients make these contributions (also, for any projections you're doing).

Keep in mind that generally depending on state law, assets put into an IRA are also protected from the claims of creditors. So, that becomes important.

The full-length webinar transcript is available to Financial Network Subscribers.