Trending

Written by: Thomas Van Spankeren, CFA, CFP® | RISE Investments

- Purchasing your first home is a great time to begin estate planning for young adults

- Avoiding probate should be a priority and can be achieved by proper estate planning techniques

- When undergoing estate planning, make sure your mortgage and insurance information is up to date

What is Estate Planning?

Estate planning is essential to young homeowners. Estate planning involves putting together a strategy to manage your financial situation, including your home, in an event of incapacitation or death.

Additionally, estate planning provides guidance into important topics such as healthcare decisions should something happen as well as guardianship to young children. Estate planning ensures asset protection, legacy, clarity, and care for your loved ones, including your children.

Starting estate planning when purchasing your first home is often appropriate as it tends to correspond with other major life events such as having a child or accumulating wealth.

Given your home is likely the single largest asset on your personal balance sheet, ensuring your home is handled according to your wishes is particularly important.

What is Probate and Why Should it be Avoided?

Without proper estate planning, upon passing your family would be stuck with the burden of dealing with probate which is a lengthy, public, and pricey process where a judge oversees the administration of your estate instead of your loved ones.

Probate can create problem for your heirs. For instance, without proper estate planning, your home may be inherited by relatives that you had no intention of having an ownership interest in the home creating family conflict for an illiquid asset.

How Can Homeowners Avoid Probate?

There are two common ways in which homeowners can avoid probate.

Revocable Living Trust

A revocable trust is a document created to manage your assets, including your home, during your lifetime and distribute the remaining assets after your death as you desire. The trust can be changed during your lifetime as your circumstances change. A successor trustee is chosen who is responsible for distributing the assets to the beneficiaries according to the rules of the trust agreement. A successor trustee will also make important decisions on your behalf should your incapacity occur.

Creating a revocable trust allows for bypassing probate and more control over assets to your loved ones, including your children. It is important to not only create the trust but to fund assets such as your home into the trust. This generally involves legally changing the property’s title from the owner’s name to the trust’s name.

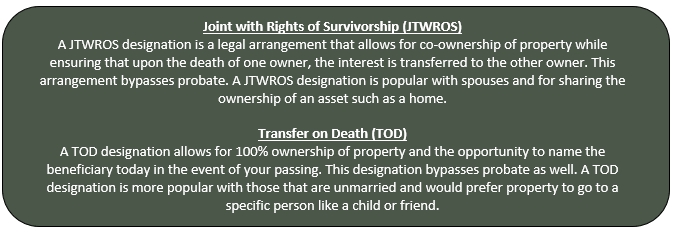

Designate a Beneficiary

Homeowners that do not have a revocable living trust may opt to designate a beneficiary in the event something should happen. Two common ways to designate a beneficiary include Joint Tenancy with Rights of Survival (JTWROS) and Transfer on Death (TOD) designations.

What Happens to your Mortgage Should Something Happen?

If there are two or more borrowers on a mortgage and a borrower passes away, the first thing you should do is reach out to the current mortgage servicer. You will have to let them know that a borrower has passed away. If the surviving borrower is able to make the mortgage payments on their own, there will not be any changes to the terms of the existing mortgage. Payments will still need to be made because if the mortgage stops getting paid, the servicer or bank could start foreclosure proceedings.

When you do call the mortgage servicer, they will ask for a certificate of death so make sure you have that handy. If you are unable to afford the mortgage on your own, you could also reach out to the servicer to see if there are any loan modification or refinancing options available to the remaining borrower(s).

Should I Update my Mortgage and Insurance after Estate Planning?

After estate planning and closing on your home, you may want to look into mortgage protection insurance and life insurance. Both types of insurance offer financial protection in case you or a loved one passes away.

Mortgage Protection Insurance can help payoff the remaining balance of the mortgage if one of the borrowers passes away. Life Insurance can be used in a variety of ways, including choosing to payoff a mortgage in full in the event of someone passing away.

Conclusion

Buying your first home is a major life milestone. It is important to carefully plan for the home in unlikely but possible scenarios such as death or incapacity. Being aware of what happens to your home and mortgage is valuable information to share with loved ones.