Trending

Written by: David Lebovitz

The Inflation Reduction Act (IRA) is a legislative package that includes climate spending, prescription drug pricing reform, and tax reform. The IRA seeks to raise approximately 737 USD billion in revenue over ten years through a 15% corporate minimum tax on companies earning over 1 USD billion in profits, a 1% tax on stock buybacks, greater IRS enforcement, and allowing Medicare officials to negotiate directly on prescription drug costs.

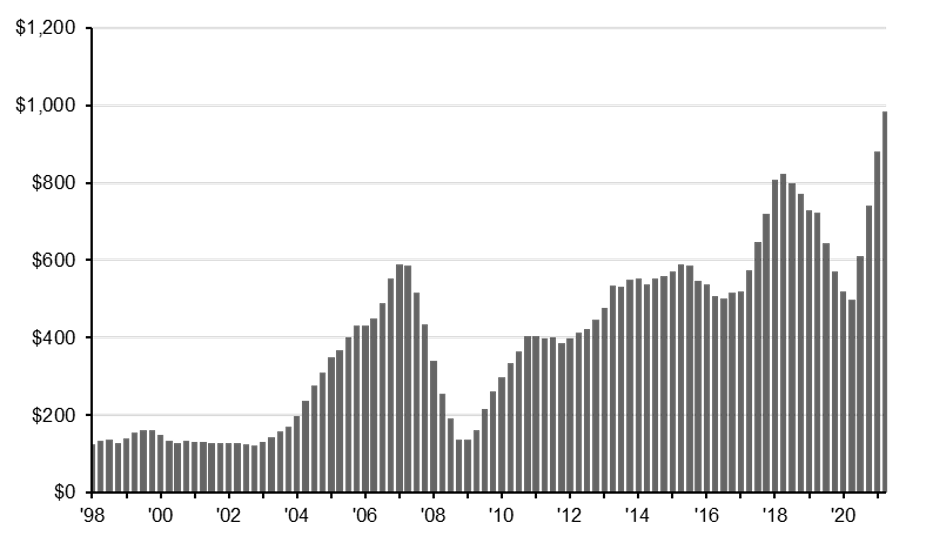

The tax on buybacks will be particularly relevant for equity investors given the role share repurchases played in enhancing profit growth during the post-GFC cycle. The big question is whether or not this buyback tax will lead companies to reduce share repurchases and increase dividend payments going forward.

As a shareholder, distributions are always taxed – the question is when those taxes are realized and at what rate. Dividends are taxed as ordinary income, meaning the shareholder receives a portion of the dividend that a company pays on a recurring basis. Buybacks are technically distributions as well, as they increase the share of earnings that each shareholder receives (and in theory, the share price). Unlike dividends, however, the tax on buybacks is realized in the form of capital gains and only when the security is sold.

Using this framework, we looked at how dividend payments have historically responded to changes in the capital gains tax rate. In general dividend payments rise over time, as dividend cuts tend to be reserved for when a company is facing significant financial hardship or a changing regulatory environment.

Since 1954, aggregate dividends paid rose by an average of 5.3% for every 1% change in the capital gains tax. If we isolate for periods when the capital gains tax increased, however, dividends rose by 7.5% for every 1% change, while when the capital gains tax decreased, dividends rose at a slower rate (2.2%). This suggests that dividend payments could increase more than expected when this tax goes into effect next year. At the same time, it also seems reasonable to expect that some future buyback activity will be pulled forward into 2022 before this tax goes into effect.

Buyback activity could accelerate into year-end

S&P 500, trailing 4Q sum, billions USD

Sources: Standard & Poor's, J.P. Morgan Asset Management.

Data are as of August 23, 2022.

Related: How Will the Inflation Reduction Act Impact the Economy?