Trending

Written by: Stephanie Aliaga

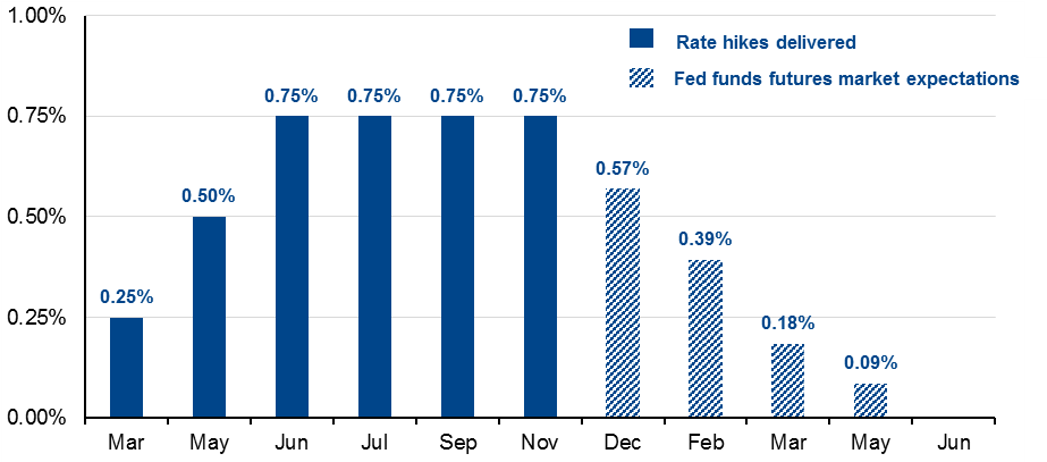

In line with expectations, the Federal Open Market Committee (FOMC) unanimously voted to raise the federal funds rate by 0.75% to a target range of 3.75%-4.00% at their November meeting. The committee’s tone remained hawkish and inflation-vigilant, but investors took initial relief at new statement language acknowledging the significant amount of tightening the Federal Reserve (Fed) has already delivered and the lags with which it will affect the economy and inflation. However, Chairmen Powell’s rhetoric in the subsequent press conference was increasingly hawkish, suggesting that the risk of Fed overtightening remains.

The statement still made no mention of any easing of inflation pressures, but new commentary around the future path of rate hikes suggested that the Fed may move to smaller rate hikes as soon as the December meeting. In determining the appropriate path to “sufficiently restrictive” policy, the Committee added that they will account for the “cumulative tightening of monetary policy” and the lags with which it affects the economy and inflation.

However, at the press conference, Charmain Powell walked back any perceived dovishness.

- Powell suggested that a smaller pace of rate hikes may come as soon as the next meeting, but emphasized that the more important question is how high rates need to go, and for how long. On the former, Powell emphasized that they still have a “ways to go”.

- The Fed is still focused on seeing official data improve and Chairman Powell expressed that data since their September meeting have increased the terminal rate expectation from previous communications.

- While Powell acknowledged that economic growth has slowed significantly this year and tighter financial conditions have contributed to this, he also emphasized that the labor market is extremely tight and wage growth remains elevated.

Following the initial statement release, bond yields fell and stocks rallied. However, this trend quickly reversed after Powell said the ultimate rate level is now higher than previously communicated. The yield curve continued to invert, with 2-year yields rising to 4.6% and 10-year yields rising to 4.1%.

While the logic of the statement changes suggest that a rate hike path of 50bps in December, 25bps in February and then a pause may be appropriate, Chairman Powell’s hawkish rhetoric afterwards suggests the Fed may have a longer runway ahead on rate hikes, pushing the terminal rate above the previously communicated 4.6%. Fortunately, we see gathering evidence that inflation will fall in the months ahead: global delivery times are back at their long-run averages, commodity prices are off their highs and wage growth looks sets to moderate. If the Fed ultimately exercises patience, as suggested in the statement language, and allows the official data to reflect improving inflation dynamics, there may still be hope of a soft landing for the economy.

After hiking rates 3.75% year-to-date, a shift to smaller hikes is in sight

Per-meeting rate hike in the federal funds rate

Source: Federal Reserve, Bloomberg, J.P. Morgan Asset Management. Data are as of November 2, 2022.

Related: What Are the Investment Implications of China’s Party Congress?