Trending

Written by: Gabriela Santos

As usual, China has been going through its own economic, policy, and political cycle. While the rest of the global economy is slowing down and facing the possibility of recession ahead due to elevated inflation and rapid policy tightening, China’s economy began to slow down over a year ago and already went through a contraction in the second quarter. In the third quarter, economic data showed a reacceleration beginning aided by low inflation and policy easing. The question for investors is how much speed China’s economy can pick up this quarter and in 2023. This depends on an improvement in local consumer and business confidence, providing a boost to domestic demand. Politically, other countries are embarking on some key transitions (U.S. Midterm Elections, change in UK and Italian Prime Ministers), while China has just concluded its twice a decade political reshuffle, the Party Congress. What are its investment implications for China’s economy and markets?

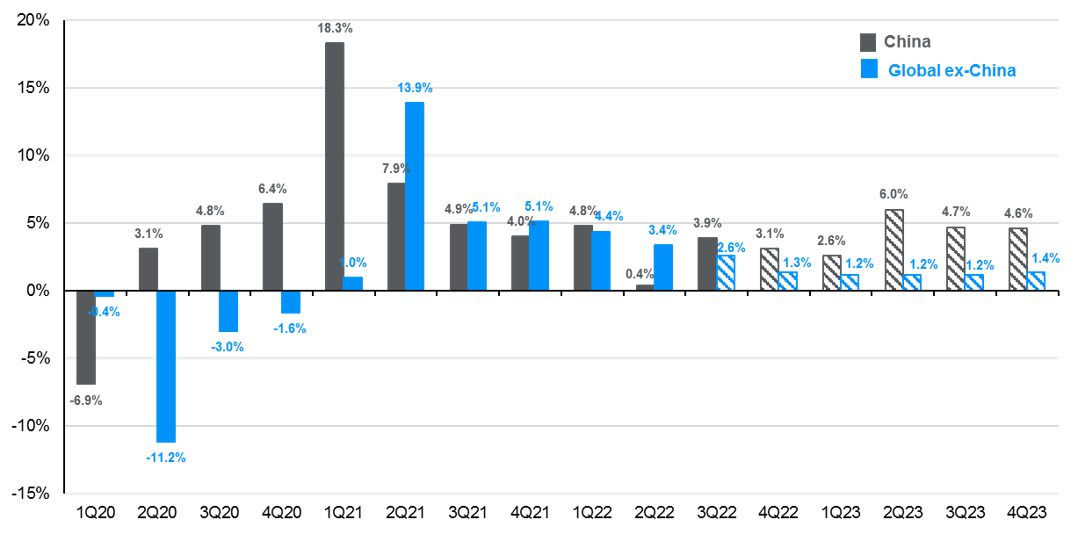

In 2Q21, China’s economy grew 7.7% year-over-year (y/y), eventually decelerating to only 0.4% y/y in 2Q22 (or -7.3% quarter-over-quarter annualized). This week’s data showed China’s economy picking up some speed in 3Q, with GDP increasing 3.9% y/y, as activity and mobility improved from April’s lows. Looking beneath the hood helps shed some light on the nuances:

- Positives: The manufacturing side of the economy expanded 5.2% y/y, helped in part by exports (which contributed 27% to 3Q GDP). Policy support continues aiding manufacturing and infrastructure investment, which grew over 10% y/y in September.

- Room for improvement: The services side of the economy grew a more modest 3.2% y/y. Retail sales disappointed in September, growing 2.5% y/y (versus 5.4% in August). The unemployment rate moved up 20bps to 5.5%.

- Challenges: Housing continued its deceleration, with residential real estate investment contracting 12.1% y/y in September.

Boosting domestic consumption, strengthening the labor market, and smoothing the pace of real estate deceleration requires an improvement in local consumer and business confidence. Now that political uncertainty has been removed with the conclusion of China’s Party Congress, investors are focused on whether policy uncertainty can also decrease. Questions remain about modifications to the “Zero COVID” strategy, implementation of reforms in the real estate sector, and the long-term success of the focus on innovation. Now that the country’s leadership structure has been settled for the next five years, some of this may now become clearer in the weeks ahead. Investors will now turn their attention to the Economic Conference in December and the National People’s Congress in March.

Initial market reaction was negative the day following the conclusion of the Party Congress (with the MSCI China falling 8.2% and the Chinese Yuan depreciating) due to policy concerns and technical factors. Local and foreign investor confidence is already low, reflected in MSCI China’s price-to-earnings (29% below its 20-year average) and the Chinese Yuan (weakest level since 2008). Small shifts towards lowering uncertainty could already spark a market rebound ahead. Ultimately, investing in China is about focusing on the “new new China” sectors, with a clear understanding of the portfolio risks involved.

While the rest of the world is slowing down, China's economy has started to reaccelerate

Real GDP, year-over-year % change

Source: FactSet, J.P. Morgan Asset Management.

Shaded figures represent J.P. Morgan Investment Bank estimates for GDP growth.

Data are as of October 25, 2022.

Related: What To Do With Fixed Income?