Trending

Written by: Jordan Jackson

In a highly anticipated policy decision, the Federal Open Market Committee (FOMC) voted to raise the Federal funds rate by 0.25% at its May meeting to a target range of 5.00%-5.25%, the highest level since June 2006. Compared to its first meeting of the year just three months ago, the statement language has shifted from “ongoing increases will be appropriate” to a data-dependent approach “in determining the extent to which additional policy firming may be appropriate”, hinting the committee is ready to pause rate increases.

On balance, recent data point to greater risk of more material slowing in the economy further supporting a pause:

- 1Q23 real GDP growth come in weaker than anticipated, and while consumption growth in the quarter was robust, much of that pop was driven by a generous bump in social security payments in January and a relatively mild winter.

- The ~1.6 million decline in aggregate job openings this year1 suggests excess demand for labor is declining which in turn should allow wage inflation to continue to moderate.

- Bank failures have led to tighter lending conditions. Given both the access to credit and the cost of credit have become more restrictive, this is expected to lead to further weakness in overall activity.

- While inflation remains above target for now, the disinflation trend is poised to continue as food and energy prices moderate further, and shelter inflation begin to reflect a recent stabilization in rents.

Notably, during the press conference, the Chair of the U.S. Federal Reserve, Jerome Powell, pushed back against the potential for rate cuts later this year given the committee expects inflation will move down at a slower pace than what markets anticipate. Elsewhere, when asked about the committees’ perspective on the recent bank failures, Powell generally tried to instill confidence that the worst is behind us, though the committee will continue to assess and exercise its supervisory authority over the sector to ensure stability.

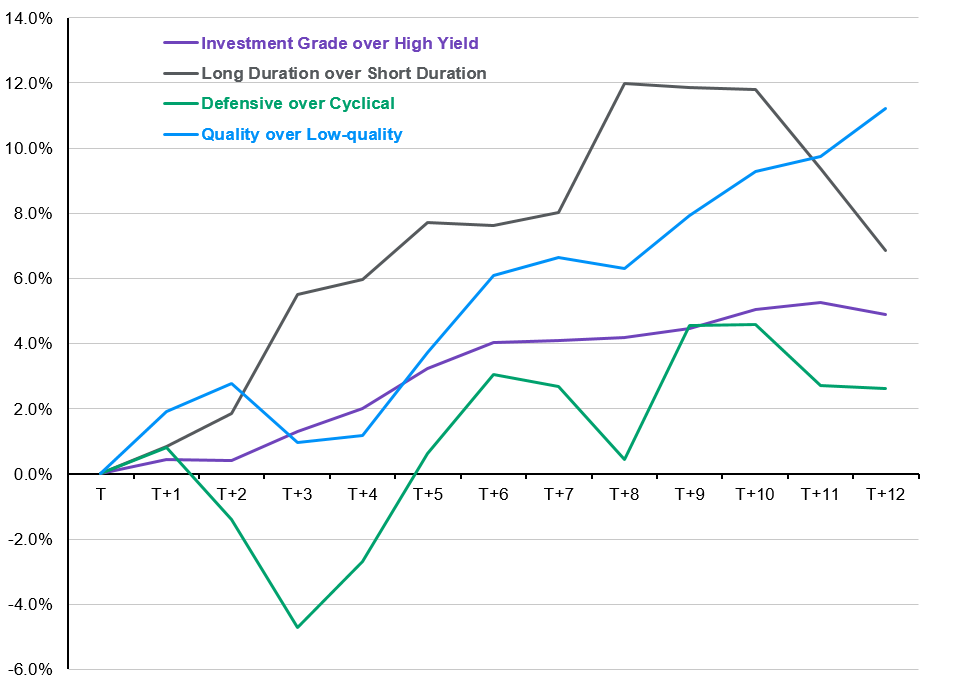

While market pricing of policy rate expectations has swung wildly over the past few weeks, today’s announcement was generally in line with consensus. We now expect the Fed to pause at the current target range. Even though, the committee continues to push back on rate cuts, a deteriorating economy may force the Fed to begin reducing policy rates later this year. For investors, as the Fed concludes the current tightening cycle, this suggests an overweight to quality and duration, and a more defensive posture within equities.

Cumulative outperformance after final Fed rate hike in a cycle

Average cumulative outperformance, total return, T = month in which the last rate hike occurred

Source: Bloomberg, MSCI, Standard & Poor's, J.P. Morgan Asset Management. Investment Grade: Bloomberg US Corporate Bond Index, High Yield: Bloomberg US Corporate High Yield Bond Index, Long Duration: Bloomberg US Long Treasury Index, Short Duration: Bloomberg US Short Treasury Index, Defensive: MCSI Defensive Sectors Index, Cyclical: MSCI Cyclical Sectors Index, Quality: S&P 500 Quality Index, Low-quality: S&P 500 Quality - Lowest Quintile Index. Due to data availability, Investment Grade over High Yield averages outperformance from the past 6 rate hiking cycles, Duration over Short Duration averages outperformance from the past 5 rate hiking cycles, Quality over Low-quality averages outperformance from the past 4 rate hiking cycles, and Defensive over Cyclical averages outperformance from the past 3 rate hiking cycles. The calculations are based off of monthly returns, and begin at the month-end price for the month in which the last rate hike occurred. Data are as of May 3, 2023.