Written by: Gabriela Santos and Mary Park Durham

For over a year, investors have been hyper-focused on the performance of just seven U.S. companies, nicknamed the “Magnificent 7”,1 and rightfully so, given their outsized returns, earnings growth, and long-term tailwinds. At this point, some investors may wonder if they should invest in different U.S. asset classes or regions. However, concerns are growing about being overly concentrated in a few names: these companies are now behaving independently rather than as one single block and other companies are catching up more (with the contribution of the “Mag 7” to S&P 500 index returns dropping to 86% from its peak of 120% last year). Investors should not ignore what is happening overseas either, with several indices hitting all-time highs and companies in other developed markets consistently being on the world’s “top performers” list. This suggests that current deep underweights to developed markets outside the U.S. could leave opportunities on the table.

It has made sense that U.S. investors have wanted to avoid other markets, not only because of the buzz generated by some U.S. companies, but also due to negative global headlines. This includes “recession” headlines (with Japan and the UK dipping into technical recessions in the second half of 2023), geopolitical tensions (with two horrific wars in Europe and the Middle East and ongoing tensions with China), and a busy upcoming calendar of global elections. Despite this, investors may be surprised that:

- U.S. market is not the only one hitting all-time highs: In the past year, Japan, Germany, and France all hit all-time highs. Impressive milestones have been reached: Japan’s Nikkei 225 hit a new high for the first time in 34 years and European markets followed suit, surpassing their high last reached in January 2022.

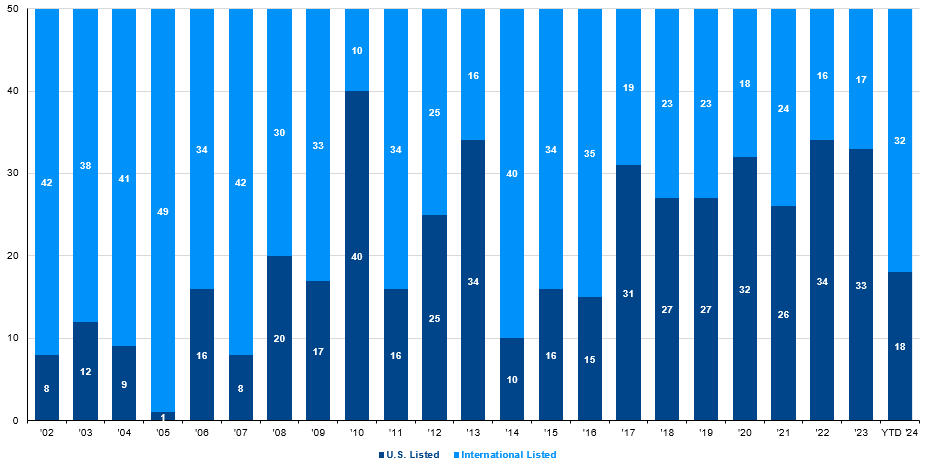

- “Mag 7” companies are not the only ones delivering eye-catching returns: So far this year, 32 of the top 50 best performing companies are internationally listed. Even last year, 17 of the top 50 companies were international. Over the past 25 years, on average over half of the top 50 best performing companies have been listed overseas.

- Weak macro data doesn’t mean weak market performance: Companies in Europe and Japan derive a high percentage of their revenues from abroad. For example, Japanese companies derive 53% of their revenues from abroad and benefit from a weaker Yen. Beyond that, international companies have a lot of exposure to long-term structural trends: artificial intelligence via semiconductor related companies in North Asia and Europe, GLP-1 drugs pharmaceutical companies in Europe, and growth of the EM middle class via leading luxury companies in Europe.

- Domestic picture has improved in DM ex-U.S.: While challenges exist for the international economy, the direction of travel is important. For Europe and Japan, the return of inflation and positive interest rates is a game changer: earnings have improved as a result of higher end-consumer prices and European and Japanese banks have awoken from their post-GFC slumber (up over 25% last year). In addition, corporate governance reforms are helping companies in DM ex. U.S. markets focus on shareholder value, especially key for the Japanese market.

Investors should certainly not chase past returns, but the impressive statistics above help to highlight the positive change in international markets. Momentum will likely continue to build as a result of still favorable valuations and currencies, as well as superior dividend income in some markets. Rather than go overweight international, these changes argue for a reduction in deep international underweights in portfolios. This is already underway, as international exposure within average U.S. equity portfolios has gone from 20% in December 2022 to 23% in January 2024.2 At the same time, this still represents a 12% underweight to the asset class. Some markets, like Japan, even deserve to be overweight given the positive tailwinds. Investors should consider increasing their exposure via active management to gain exposure to high-performing markets and companies around the globe.

On average, over half of the top 50 best performing companies in developed markets are listed abroad.

Top 50 performing companies in the MSCI World Index by year, based on total returns in USD

Source: FactSet, MSCI, Global Equities - J.P. Morgan Asset Management. Companies ranked in no particular order. Data are as of February 21, 2024.

Related: How Can Investors Avoid Falling Into the “Cash Trap”?