There is no way this bull market doesn’t end very badly. We all know that is the reality of this liquidity-fueled market, but we keep investing for “Fear Of Missing Out.”

An excellent example of investor exuberance came recently in “Investors Go All In:”

“More importantly, over the past 5-MONTHS, more money has poured into the equity markets than in the last 12-YEARS combined.”

If that chart alone doesn’t get your “Spidey senses” tingling, I am not sure what will. However, I have a few more charts to share with you.

Technical Deviations

In the short term, fundamentals don’t matter. Such is because over a few days, weeks, or even months, what drives prices higher or lower is the psychology of investors. As such, we can look at technical deviations to determine how exuberant or not the market currently is.

For moving averages to exist, prices must trade both above and below that average. As such, moving averages act like gravity on prices. When prices deviate too far from the moving average, eventually, prices will revert to, or beyond, that average.

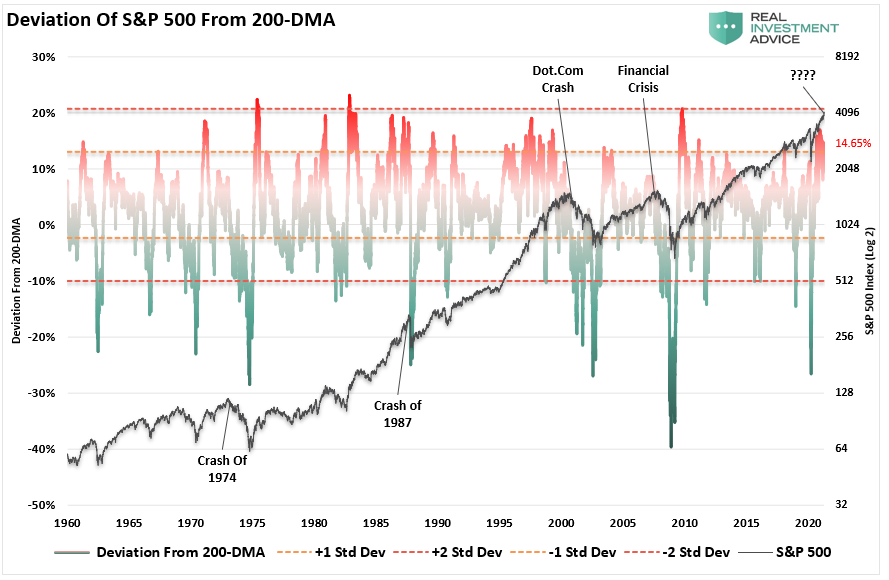

We can visualize the reversion in the chart below of the S&P 500 index versus its 200-dma. With the index currently more than 14% above its 200-dma, such should be a short-term warning to investors.

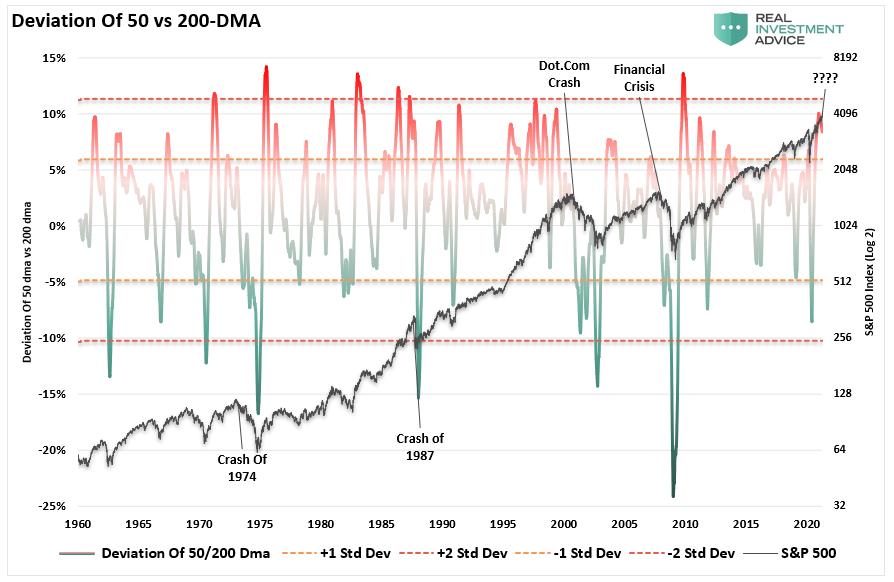

The following chart says much the same. Currently, the 50-day moving average is also significantly deviated above the 200-dma. Such suggests that not only will prices retest the 50-dma but eclipse that level in a reversion back to the 200-dma.

Notably, technical deviations in the short term do NOT mean the market will “crash” tomorrow. Markets can remain deviated for quite some time. However, when the deviations begin to diverge from the price index negatively, such has previously preceded more important corrections and bear markets.

A Very Leveraged Market

“Margin debt isn’t an issue. It provides the fuel for asset prices higher.”

That is a correct statement.

Rising levels of margin debt are a measure of investor confidence. Investors are more willing to take out debt against investments when shares are rising. The more prices increase, the more they can borrow. However, the opposite is also true. Falling asset prices reduce the amount of credit available, and the liquidation of assets must occur to bring the account back into balance.

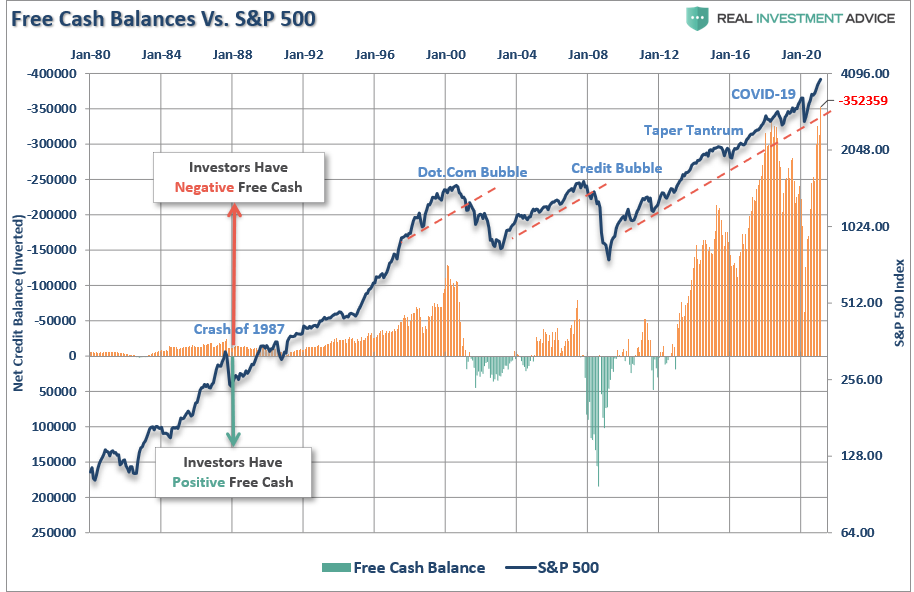

As discussed previously, “negative cash balances” are at a record.

I want to make a critical point here. Margin debt, like valuations, are “terrible market timing” indicators and should not be used as such. I agree and disagree that margin debt levels are simply a function of market activity and have no bearing on the outcome of the market.

As we saw in March of 2020, the double-whammy of collapsing oil prices and economic shutdown in response to the coronavirus triggered a sharp sell-off fueled by margin liquidation.

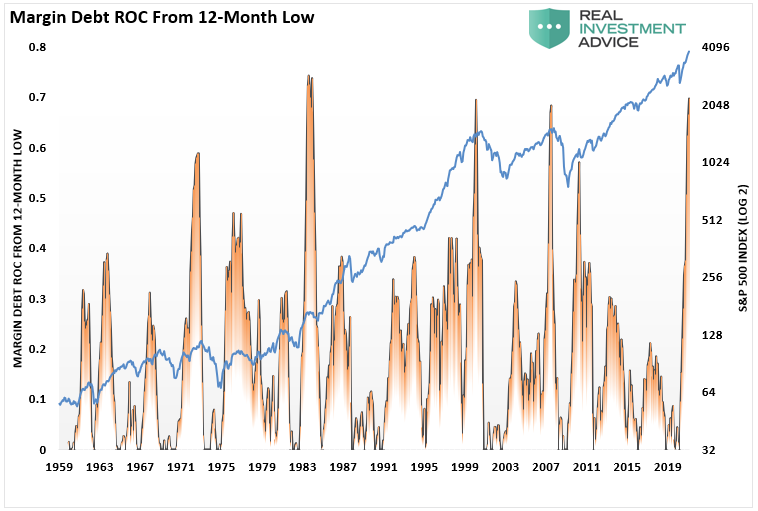

However, since then, the surge in margin debt has reached extreme levels. More importantly, as shown in the chart below, it isn’t the “level” of margin debt that reflects investor exuberance but rather the rate of change. In this case, we can see a very sharp spike in debt from the previous 12-month low. Such has only occurred near previous market peaks and bear markets.

As Jason Zweig recently penned:

“Where ignorance is bliss, ‘tis folly to be wise,” wrote the British poet Thomas Gray. One of these days, perhaps sooner rather than later, stocks will stop going up and the importance of understanding what you own will reassert itself. For the time being, though, investors who used to think of themselves as wise may continue to look foolish.”

Fundamentals Will Matter, Eventually

As stated above, in the short term, fundamentals do not matter. However, in the long term, they matter a lot.

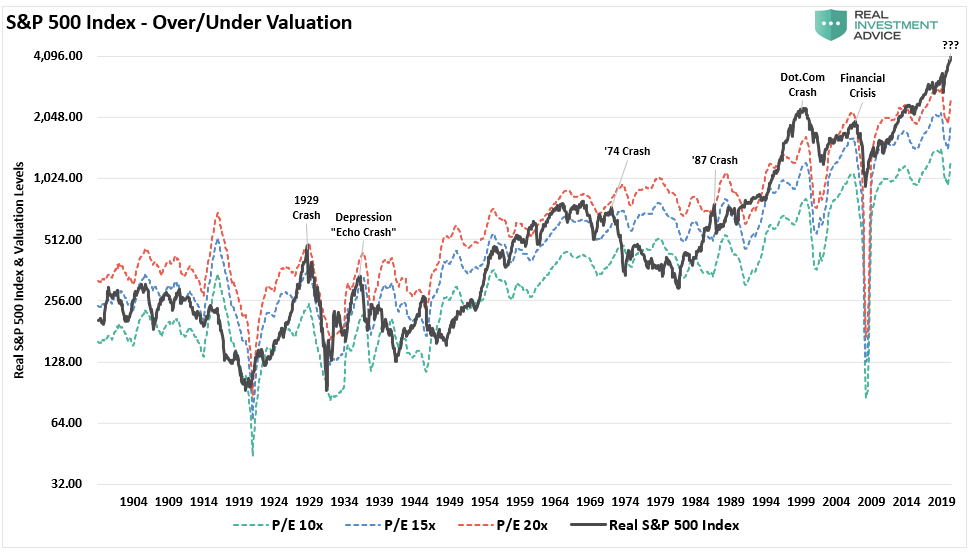

Currently, investors are overlooking fundamentals on the expectation the economy and earnings will improve to justify the market overvaluation. There is scant evidence over the last 20-years such will be the case.

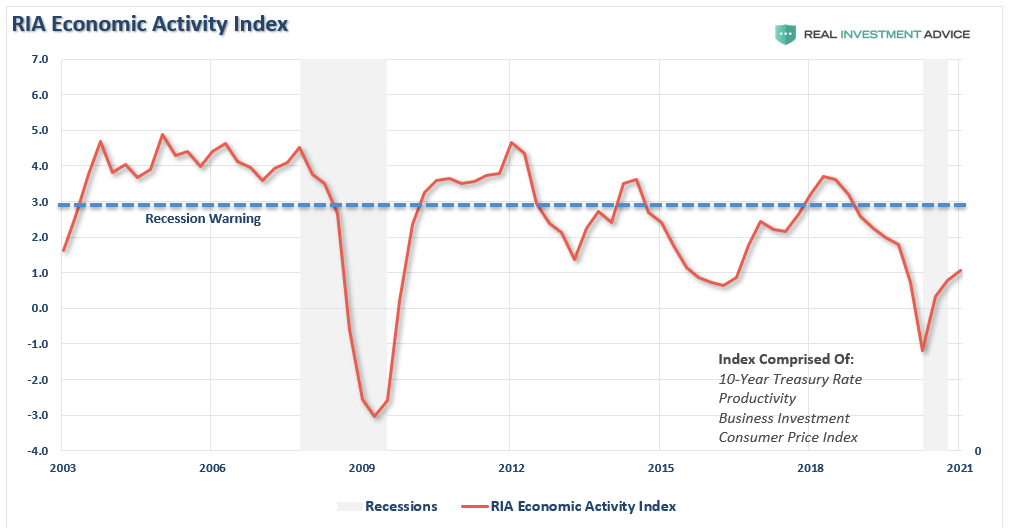

The “Economic Activity Index” is an average of the 4-most essential components of organic economic activity. Interest rates have a long historical correlation to economic activity, along with inflationary pressures. Without productivity and business investment, jobs do not get created to support consumption which is ~70% of the GDP calculation.

Through the first quarter of 2021, the economic recovery expected by economists is running well ahead of what the index approximates. Furthermore, given much of the market’s advance is based on optimistic expectations, there is potential for disappointment.

Such is where fundamentals become extremely important. When, or if, expectations of recovery are disappointed, the market will begin to reprice itself for its intrinsic value. Given that the market is currently trading more than twice the level of underlying economic growth, which is where corporate profits come from, such suggests a significant risk.

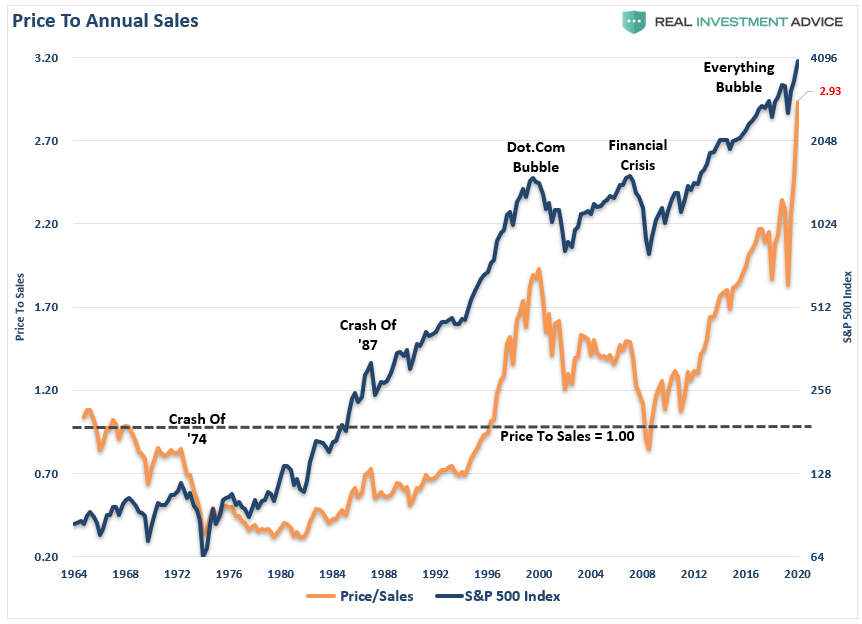

The level of price versus sales, which occurs at the top of the income statement (and much less subject to manipulation, also suggests a risk.

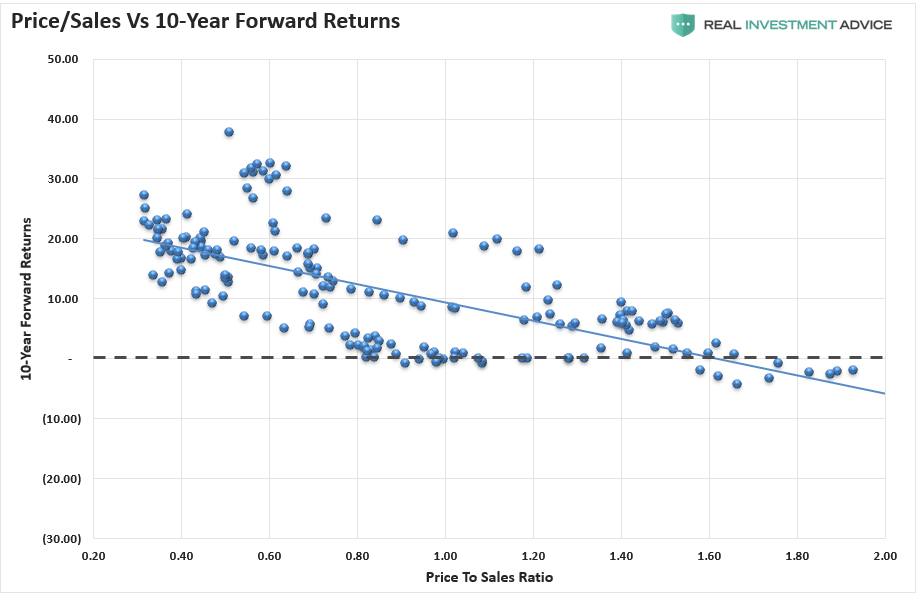

10-year forward returns are below zero historically when the price-to-sales ratio is at 2x. There has never been a previous period with the ratio climbing to near 3x.

Of course, with markets trading well above 20x earnings, history further suggests that investors are likely to be disappointed in the future as markets reprice value.

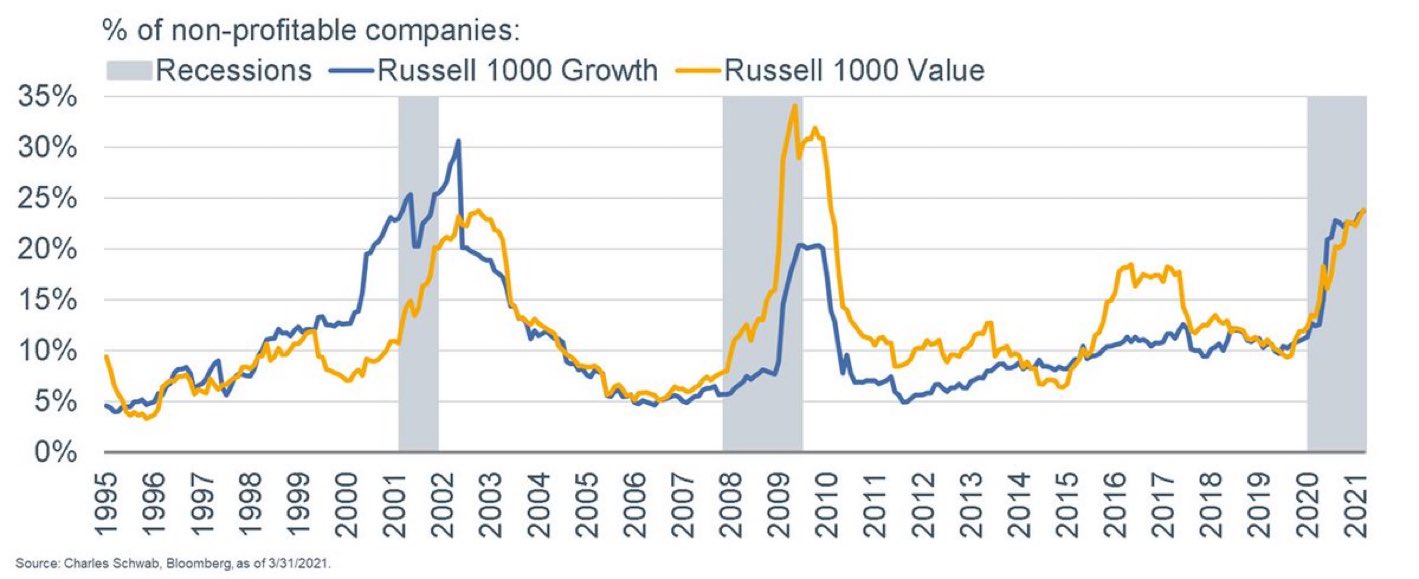

Such is particularly problematic when investors chase stocks with no profits.

Conclusion

While we remain long-biased in our equity portfolios, we are chasing performance like everyone else. As I noted in “Fully Invested Bears:”

“While the mainstream media continues to skew individual’s expectations by chastising them for “not beating the market,” which is impossible to do, our job is to participate in the markets with a bias toward capital preservation. As noted, the destruction of capital during market declines has the most significant impact on long-term portfolio performance.

From that view, as a portfolio manager, the idea of ‘fully invested bears’ defines the reality of the markets we live with today. Despite the understanding that the markets are overly bullish, extended, and valued, we must stay invested or suffer potential “career risk” for underperformance.

Such is the consequence of the Federal Reserve’s ongoing interventions. Portfolio managers must chase performance despite concerns of potential capital loss. In other words, we are all ‘fully invested bears.’ We are all quite aware this will eventually end badly. However, in the short-term, no one is willing to take the risk of being grossly underexposed to Central Bank interventions.”

While it certainly may “feel” like the market “can’t go down,” it is worth remembering the sage words of Warren Buffett.

“The market is a lot like sex, it feels best at the end.”

We remain “bullish” on the markets currently as momentum is still in play. However, we are also continually taking precautions to monitor and manage risk accordingly.

For us, that means putting a spin on Warren’s quote:

“If you engage in the market in an unprotected fashion, you may not want the unexpected surprise.”

Related: Earnings Optimism Explodes