Trending

Growing wealth happens over decades. Within these decades are many bullish and bearish cycles. While investors tend to focus on making the most of the bullish cycles, it is equally important to avoid letting bear markets reverse your progress. The amount of time spent in bear markets is minimal, but the time lost recovering your wealth can be substantial. Given the possibility that we are in the early innings of a bear market, it is worth revisiting bear market wealth management strategies and the math showing why such a strategy is essential.

Is This Time Different?

Over the last two decades, investors have gravitated toward passive buy-and-hold strategies. Who can blame them? Such strategies allow investors to sit back and relax. Avoiding having to time markets and picking winning stocks is not only simple, but it has been effective.

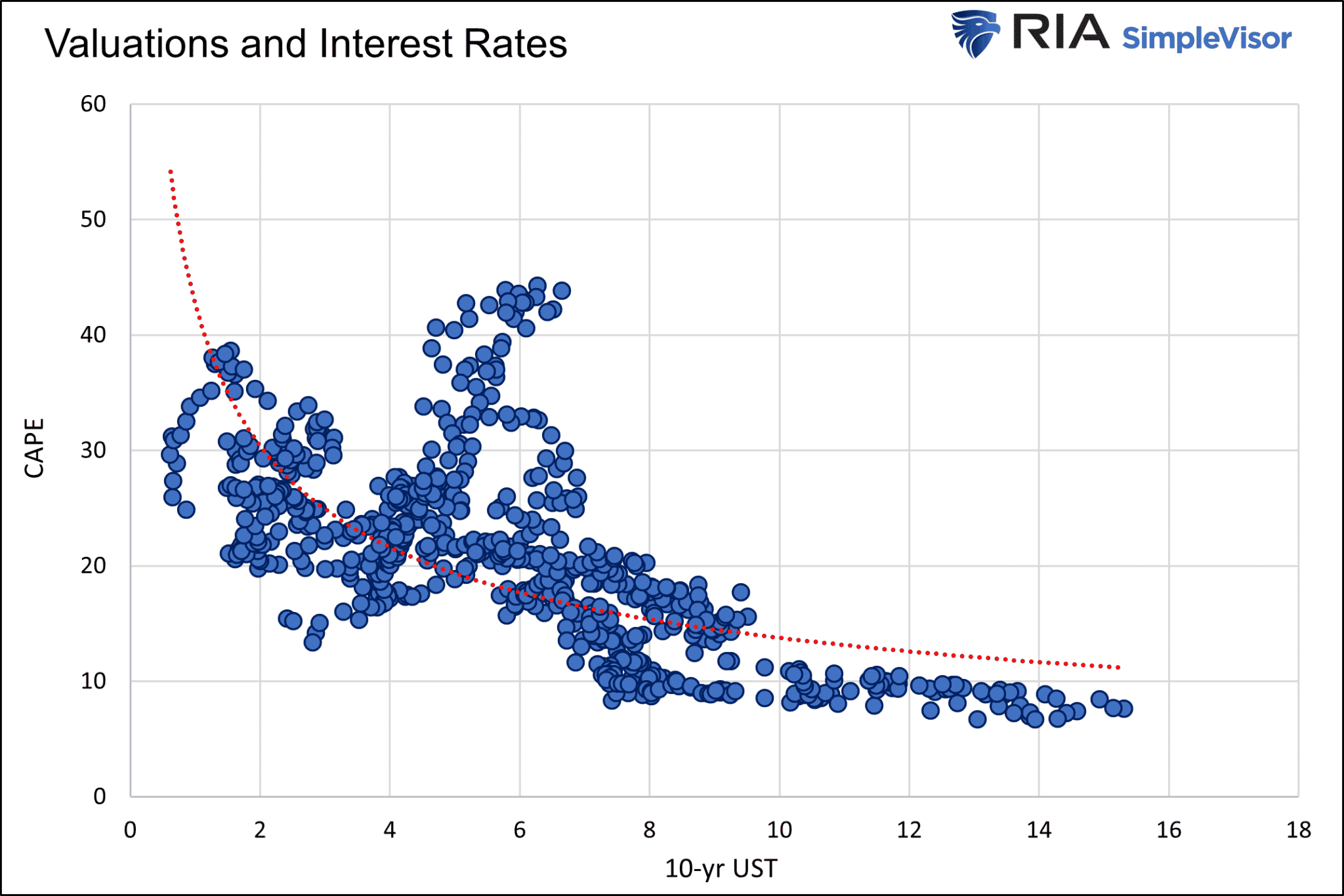

Passive buy and hold strategies work in large part because the low inflation regime of the last thirty years allowed the Fed to support markets with plenty of excess liquidity when markets felt some turbulence. Low-interest rates and QE support high valuations and asset prices, as shown below.

Is the low inflation regime changing? In Persistent Inflation Scares The Fed and Deglobalization and Central Banking, we make a case that a persistent price-wage spiral and deglobalization may cause inflation to run hotter than it has in quite a while. Instead of assuming inflation will normalize and monetary policy will return to normal, we must ask tough questions.

- What if inflation proves persistent and doesn’t retreat by as much or as fast as investors expect?

- What if central bankers must keep administering the harsh monetary medicine the markets are struggling to digest?

As we wrote in Deglobalization and Central Banking:

They (central bankers) are very adept and have the tools to control demand. They do not have the tools to manage supply. We are potentially on the cusp of enormous change.

Persistently higher inflation may keep the Fed focused on the prices of goods and less so on asset prices. Passive strategies in such an environment will likely have much less success than it has during most of our careers. Bear market wealth management strategies may be the key to keeping your wealth goals on track.

Buy and Hold vs. Bear Market Wealth Management

Nothing is complicated about a bear market wealth management strategy, but it differs vastly from a buy-and-hold passive approach.

Bear market strategies boil down to managing equity exposure. As a real example, in Liquidity and Valuations, we examined how we repositioned our client’s portfolios at the start of 2022 and managed through the 20+% drawdown. To wit:

Sensing the Fed was about to pull the liquidity rug from the markets, we started reducing our risk starting on the first trading day of 2022. Not only did we sell shares to reduce our gross equity exposure, but we rotated from higher beta growth stocks to lower beta value stocks.

Without getting into details, we reduced our exposure to the stock market regarding the percentage allocated to stocks and the types of stocks we held. As a result, we are handily outperforming our benchmark and all primary stock indexes year to date.

The Compounding Math Supporting Bear Market Wealth Management

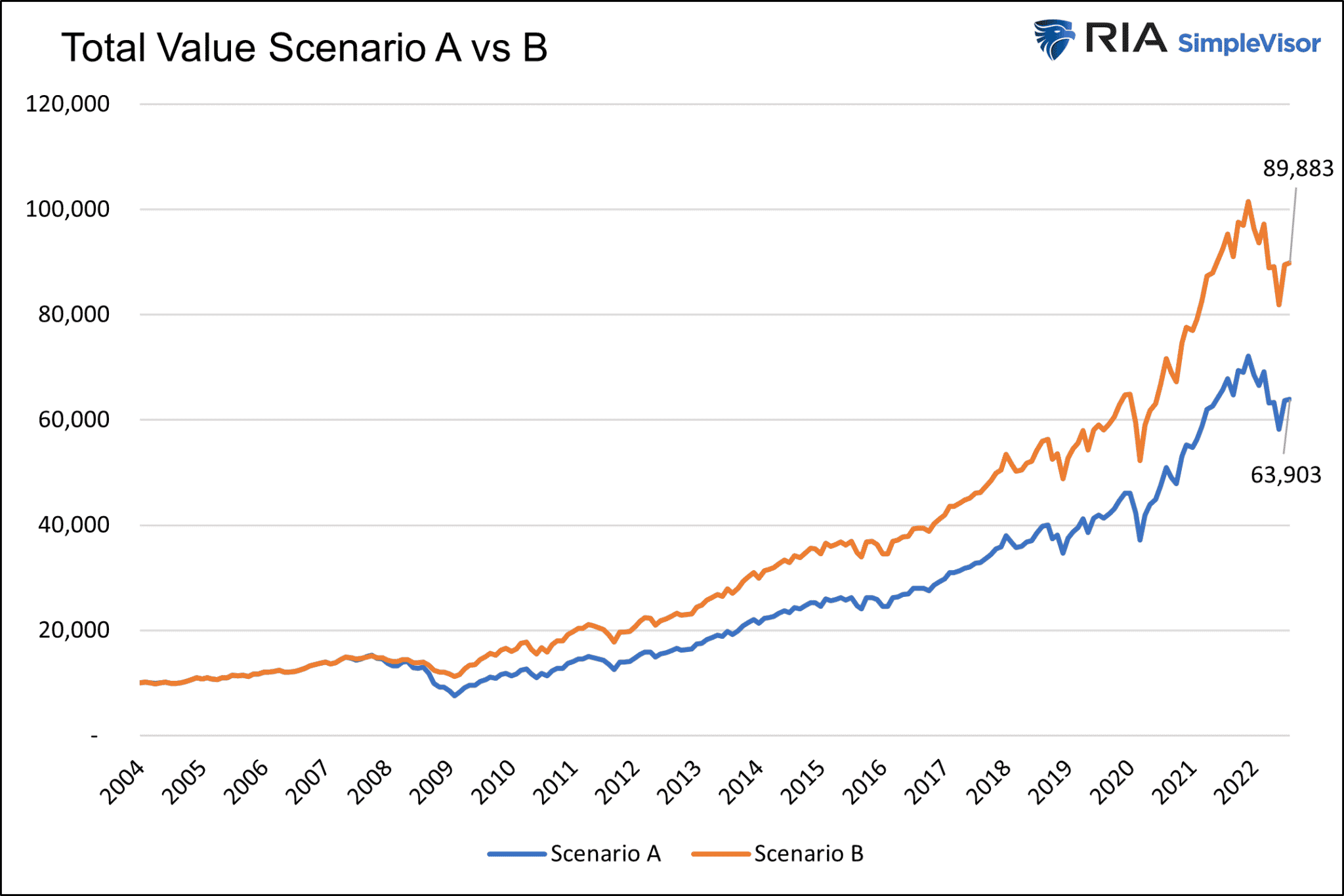

We share two simple scenarios to explain why actively managing risk exposure and limiting drawdowns in a bear market is so important. In both scenarios, we initially invested $10,000 in 2004. Scenario A is a buy-and-hold passive portfolio. It is fully allocated to the S&P 500 at all times. The Scenario B portfolio is fully allocated to the S&P 500 at all times except during the bear market of 2008. During that period, scenario B’s portfolio has a 50% allocation to the S&P 500, with the remainder in cash earning 0%. We reinvest dividends in both scenarios.

The first graph below shows that by simply cutting equity exposure in half for less than two years, scenario B’s value is currently 41% more than scenario A.

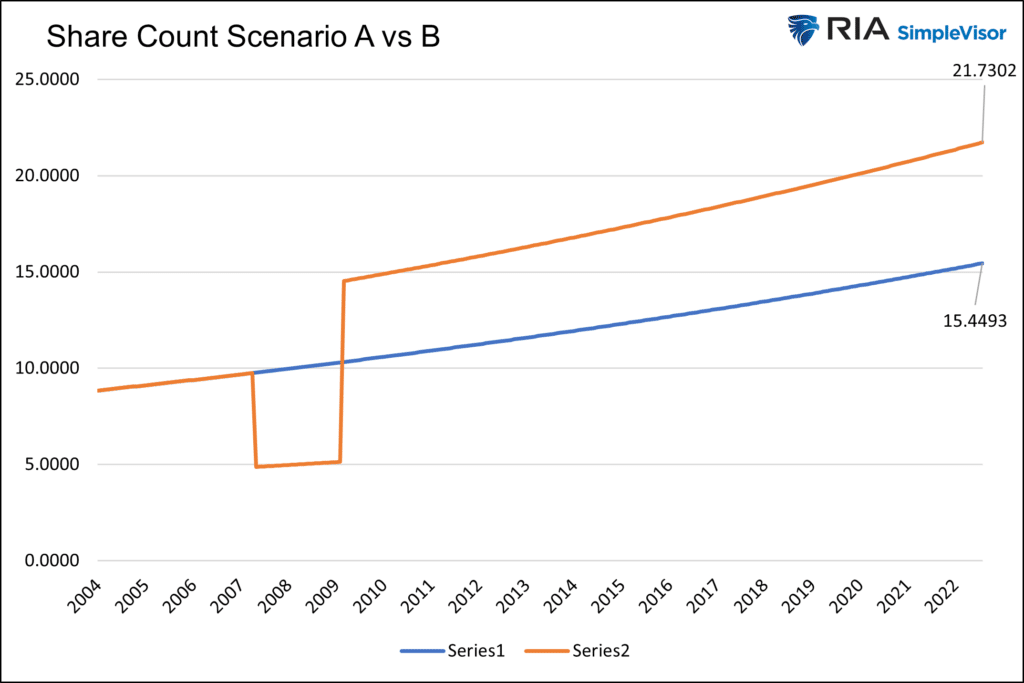

The following graph shows that both scenarios started with the same number of shares. But after redeploying cash in 2009, scenario B now has 50% more shares to earn dividends and profits.

A bear market wealth management strategy is simple with 20/20 hindsight. In reality, we know that getting in and out of markets at the exact top or bottom is impossible. The point of the example is to show that any reduction of exposure that diminishes your losses. Accordingly, it leaves you more wealth to invest when the bull market returns.

To boil this down, all we did was cut our exposure in half for two years over 18 years. As a result, our wealth was 41% greater than it would have been. Had we reduced our exposure more and acted similarly in 2020 and 2022, the relative returns would have been even better.

Summary

The benefit of compounding is maximized when a portfolio can feed on itself. Ben Franklin summarized compounding as follows:

The money that money earns, earns money

Any reduced exposure to stocks in a bear market leaves more money to buy stocks when prices are lower. The advice is so simple yet so hard for many investors to follow.

The mutual fund complexes and banks and brokers want commoditized markets. What better way than passive strategies to create a one size fits all approach? While buy and hold and other passive strategies may help their bottom lines, they are not always best for your bottom line.

We end with an oldie but goodie from Lance Roberts:

“It is ALWAYS okay to miss out on an opportunity, as opportunities come along as often as a taxicab in New York City. However, it is IMPOSSIBLE to make up losses as you can never regain the time lost getting back to even”.

Related: Deglobalization and Central Banking