Trending

Written by: Stephanie Aliaga

Investors have become all too familiar with the concept of “transitory” inflation over the last two years, after a seemingly temporary inflation surge stuck around much longer than expected. At the February Federal Open Market Committee (FOMC) press conference, Chairman Powell brought back the infamous term but this time to describe disinflation, or the falling inflation rate, that has helped boost market sentiment and stock prices in recent weeks.

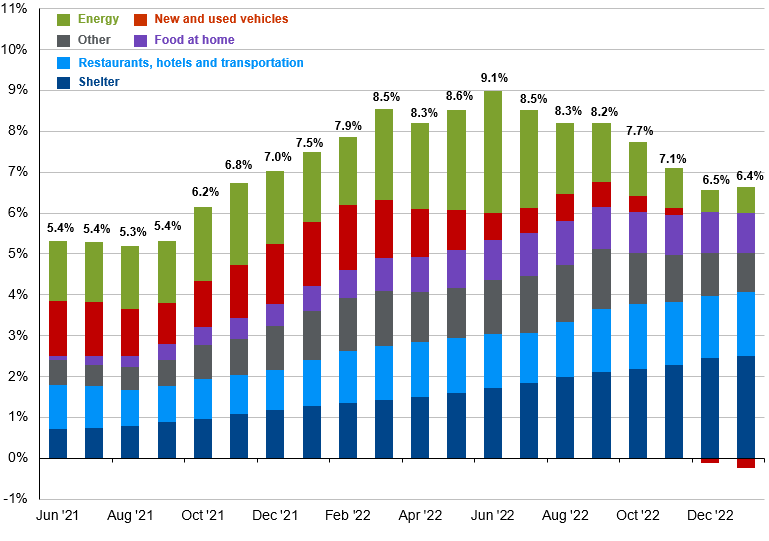

After a string of monthly declines, the January CPI report showed a bounce in headline inflation of 0.5% m/m and 0.4% m/m excluding food and energy. Markets had largely expected the uptick, but the underlying components showed a more mixed inflation picture compared to the broad-based declines seen in prior months. Still, we believe disinflation is in its early innings across the major components of CPI, as outlined below, and should gradually bring inflation back down to 2-3% over the course of 2023 and 2024.

- Energy: Energy inflation has declined from a peak of 41.3% y/y last June to 8.4% y/y in January as most of the impacts from Russia’s war in Ukraine have now passed. Barring another shock, this should come down further and pass-through to food inflation, which still has a long way to get back to normal.

- Core goods: Improved supply chains and the shift from goods consumption to services has brought core goods inflation considerably lower. Used car prices have been a major contributor to the slowdown, and bloated dealers’ margins in the context of softening consumer demand and higher inventories point to a need for further price declines, but the path will likely be bumpy.

- Rent: Shelter inflation makes up a large chunk of CPI and in the January release, accounted for nearly half of headline inflation gain. While the lag is significant, owner’s equivalent rent (OER) should soon begin to reflect the rollover in Zillow market rents. Once OER begins to reflect this data, it’s downshift will have a huge impact on core inflation—particularly following the BLS’s annual revisions that give OER a larger index weighting than last year.

- Core services ex-housing: The Federal Reserve’s focus measure on inflation remains elevated but is showing early signs of moderation. Real-time data on services prices point to further declines: airline fares should fall given lower jet fuel prices, hotel room rates have leveled off and the ISM services survey on prices has gradually declined over the last year.

Overall, we expect disinflation will be durable and significant, but it won’t be a smooth ride either given China’s reopening, the recent uptick in Manheim used car prices and elevated wage growth. Still, a slowing economy with improved supply chains and moderating wage growth cannot sustain a +6% annual inflation rate, underscoring a disinflationary wave with plenty of room to run.

Meanwhile, the Fed remains laser-focused on its intent to bring inflation down to its 2% target as soon as possible, raising the risk that they ultimately force a hard landing. Fed tightening expectations have risen in recent weeks, with the peak terminal rate now at 5.28% and just one rate cut priced in by the end of the year. Yet despite the climb in Fed expectations and elevated recession risks, stocks continue to perform remarkably well year-to-date. In this environment, investors should be wary of complacency and defensive positioning seems appropriate, with an emphasis on international diversification and a greater allocation to high-quality fixed income assets, as we await further clarity on the timing of a Fed pivot and the impact of monetary tightening on growth and inflation.

The major contributors to recent disinflation have room to run

Contribution to y/y % change in CPI, non seasonally adjusted

Source: Bureau of Labor Statistics, J.P. Morgan Asset Management. Contributions mirror the BLS methodology on Table 7 of the CPI report. Values may not sum to headline CPI figures due to rounding and underlying calculations. “Shelter” includes owner’s equivalent rent and rent of primary residence. “Other” primarily reflects household furnishings, apparel, education and communication services, medical care services and other personal services. Data are as of February 14, 2023.

Related: Is International Equity Outperformance Sustainable This Time?