Trending

Written by: Gabriela Santos

Since October 31, international equities have outperformed the U.S. by 12% points (in U.S. dollars). How sustainable is international outperformance this time? Absolute and relative valuations are still favorable, the U.S. dollar is still too strong, and positive surprises on international economic growth suggest upgrades to earnings expectations (versus downgrades in the U.S.). However, the key argument for a new cycle of international outperformance is the structural change to the macroeconomic picture, which can favor exactly the type of companies found overseas. Whereas deep portfolio underweights to international markets could be ignored a few months ago, they no longer can today.

The previous ten years were characterized by low inflation and zero or negative interest rates. Going forward, some recent inflationary forces will fade, but some have structurally become more inflationary (deglobalization, energy transition, and rise of populism). The next decade is likely to be characterized by more “normal” inflation. As a result, not all recent central bank rate hikes will be unwound - the era of free money is over.

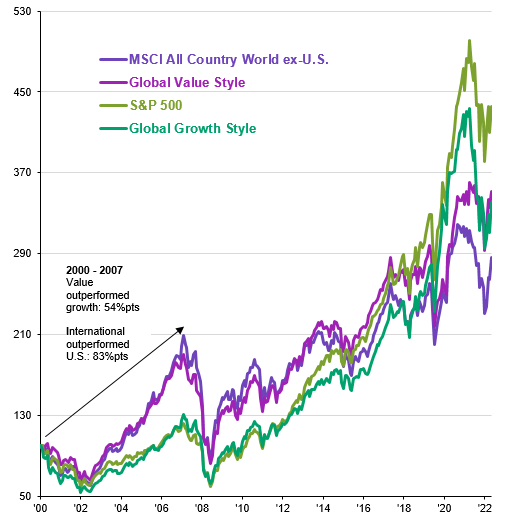

This backdrop benefits the value style more than growth, as it includes a greater percentage of sectors like industrials, financials, energy, and materials. Last year, value outperformed growth by 22%pts, the best since 2000. International markets have a much greater tilt toward value sectors versus the U.S.: 47% vs. 27% of market capitalization. We have seen this change in leadership before: following the bursting of the “dot com bubble” and before interest rates were slashed post-“financial crisis” (2000-2007), value outperformed growth by 54%pts and international outperformed the U.S. by 83%pts.

Areas of opportunity internationally include:

- Industrials: The previous decade saw a lack of capital spending, illustrated in the lack of resilience in global supply chains during COVID, the over-reliance of Europe to Russian oil and gas, and the renewed bargaining power of labor. A global “catch-up” in structural underinvestment should benefit globally leading capital goods companies listed in Japan and Europe that have dominant market positions in their respective niches: Atlas Copco in vacuum pumps and compressors, Keyence in machine vision, Fanuc in robo-machines, Schneider Electric in industrial automation systems.

- Financials: An area that was previously deemed uninvestable is European and Japanese financials due to previously negative interest rates. Japanese banks particularly were seen as uninvestable on the back of underperformance for decades, but this is rapidly changing. Japanese multinationals such as Mitsubishi UFG or regional banks are especially sensitive to a rising rate environment. They remain relatively cheap versus their regional peers, trading at a 40-50% discount to tangible book value. European banks, which have had a head start to the change in monetary policy, such as BNP Paribas, remain attractive.

International equity allocation reached a low of only 18% of a portfolio’s equity in November*. Sentiment is changing quickly: as of the end of January, this allocation is already up to 22%. With that said, this still represents a 13%pt underweight to international versus “neutral” - an important call to action for investors to not be caught offsides with the next decade’s leadership.

Value style leadership has been associated with international outperformance

Sep. 2000 = 100, total return, USD

Source: MSCI, J.P. Morgan Asset Management. Data are as of February 8, 2023.