Written by: Karen Watkin, CFA and Edward Williams

After a dismal 2022 for capital markets, the strong turnaround so far in 2023 is heartening for multi-asset investors. The MSCI World Index rose 15% year to date through June 30, shrugging off a banking sector crisis and a tense US debt-ceiling standoff along the way.

We’ve seen a sharp reversal of fortune for many of the worst-hit asset classes from 2022, with growth-orientated technology stocks being especially strong, thanks to fervent interest in the potential of artificial intelligence (Display).

Role Reversal: 2022’s Laggards Have Been 2023’s Leaders

Past performance does not guarantee future results.

Year-to-date returns through June 30, 2023. Developed (MSCI World), EM (MSCI EM), growth (MSCI World Growth), quality (MSCI World Quality), value (MSCI World Value), min. vol. (MSCI World Minimum Vol), high dividend (MSCI World High Dividend), EM debt (Bloomberg EM USD Aggregate), REITs (FTSE EPRA NAREIT Developed), commodity producers (MSCI ACWI Commodity Producers), high yield (Bloomberg Global High Yield Hedged), investment-grade Bonds (Bloomberg Global Aggregate Corporate Hedged), global treasuries (Bloomberg Global Treasury Hedged). Returns in USD.

Source: Bloomberg, FTSE, MSCI and AllianceBernstein (AB)

The more agreeable landscape has been a welcome sight for investors, including those focused on income. Much higher bond yields have created one of the most attractive and expansive income-generating markets in years, even among the highest-quality issuers—a relatively rare occurrence.

With this backdrop in mind, we think multi-asset investors should consider three broad income themes as the year plays out.

One: Higher Yields Bring Back the Power of Bonds

The outlook for bonds is much more positive now than it was last year. Yields remain attractive, and in our view, falling inflationary pressures and a global rate-hike cycle that’s nearing its end help to reduce downside risks from here.

Bonds are also starting to reassert their effectiveness as diversifiers for equities. This became very apparent during the banking crisis, when government bonds rallied while risk assets came under pressure. Bonds and stocks had suffered negative returns in tandem during 2022, giving investors few places to hide. This year, though, negative correlations are back for government bonds, providing more balance against risk assets to accompany improved income potential.

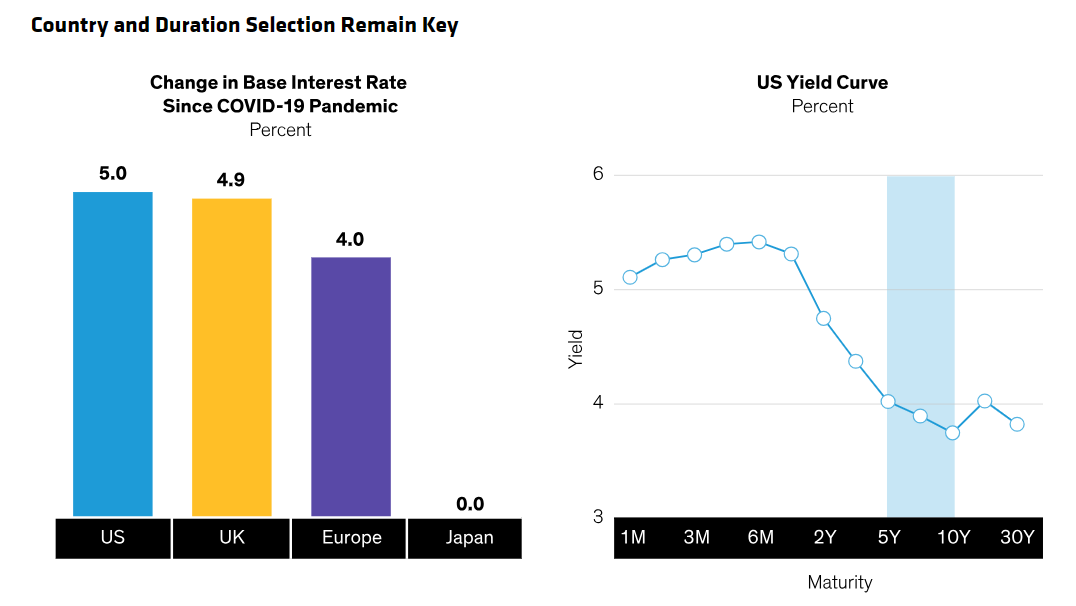

While sovereign bonds are more compelling, careful selection is important, because the interest-rate backdrop—and hence bond performance—can vary by region. For instance, aggressive hiking across the US, the UK and Europe means that central banks in these regions have much more policy flexibility than countries like Japan, should the growth outlook take a turn for the worse (Display, left).

Given the late stage of the policy cycle, we think it’s now prudent to consider increasing duration, or sensitivity to interest rates, and government bonds are particularly effective levers. Many investors leaned into ultrashort bonds as yields rose sharply in 2022, but market pricing of potential rate cuts is likely to reverse, at least in part, which could soon lead bonds at the front of the yield curve to underperform.

Maturity selection is key in sovereign bonds, too. We think the yield curve’s five- to 10-year maturity range is a preferable segment (Display, right). In our view, bond maturities beyond 10 years would add value only in a hard-recession scenario, which seems less likely at this point.

Past performance does not guarantee future results.

Change in yields measured from January 1, 2021.

As of June 26, 2023

Source: Bloomberg and AB

Two: Quality Is King Among High-Yield Bonds

High-yield corporate bonds, or credit, have a solid tradition within multi-asset income strategies as a source for yield, upside potential and portfolio diversification. And high yield has seldom looked more compelling, with the ICE BofA High Yield Index carrying a yield of about 8% at midyear.

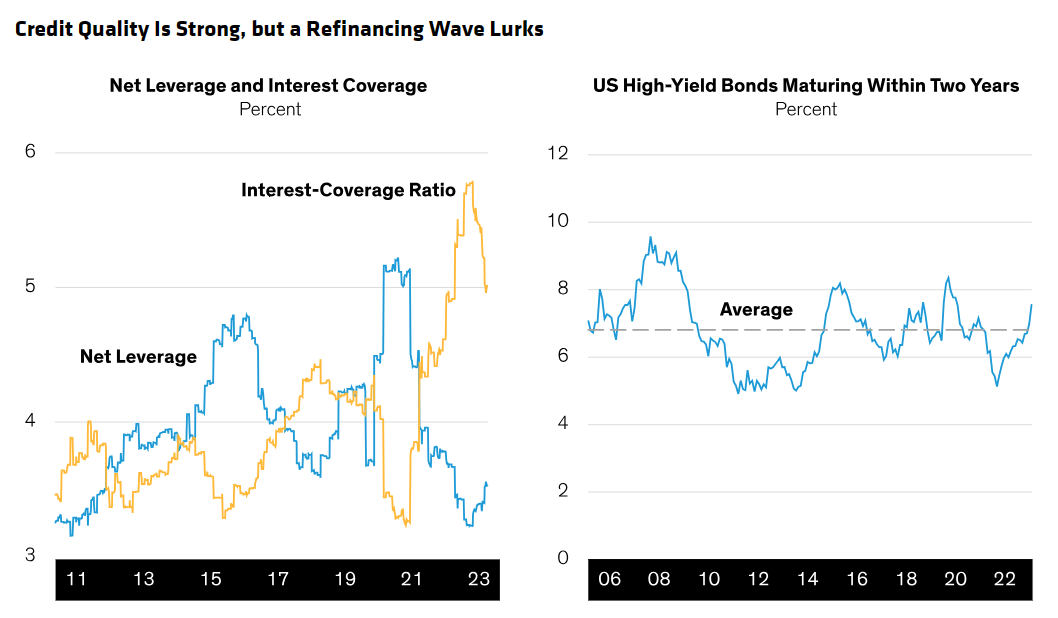

Investors tend to shy away from credit late in the business cycle, because it’s usually first to feel the pressure of downturns. But the fundamental backdrop is relatively strong this time. For instance, pandemic uncertainty led many firms to manage balance sheets and liquidity conservatively even as profitability struggled. Now, lower leverage and higher coverage ratios, along with better margins, earnings and cash flow, point to high yield being well equipped for a slowdown (Display, left).

But not all credit is created equal, so investors should be discerning. We typically lean toward the higher-rated end of the high-yield credit spectrum, such as BB-rated issuers, which have been less vulnerable during economic slowdowns. Selection is also important since an increasing proportion of the high-yield universe is due to mature in the next two years, which could become challenging if refinancing conditions remain unfavorable. However, we don’t think it’s an outsize risk in the near term (Display, right).

Past performance does not guarantee future results.

Right Hand Side average line calculated from June 30, 2006, through June 30, 2023.

As of June 30, 2023

Source: BofA Global Research and AB

Three: Invest for Wider Equity Market Opportunities

Although the equity market has been strong year to date, the dispersion among styles and sectors has been wide, with much of the return driven by a handful of mega-cap technology names. Many of the largest tech stocks pay little to no dividends, so it’s been a particularly challenging environment for income investors. Such market dynamics reinforce the need to have balance and diversification across equity exposure, in our view.

Diversification is particularly important for income investors, who could take unintended sector risks by focusing purely on high-dividend stocks. High-dividend payers are often overweight more defensive parts of the market, and crucially, can be significantly underrepresented among tech names.

Wider exposure across sectors and styles improves the odds that some part of an equity strategy will benefit, or help defend, as cycles shift. Last year, for instance, value stocks led growth stocks by more than 20%, but today growth has nearly the same advantage over value.

As we move through the year, and while recovery broadens alongside improving earnings, we expect the environment to benefit more than just a handful of sectors. The watchword should be to diversify—across investment styles, industries and regions—but focus on attractively priced, profitable companies with cash flows that seem to withstand economic downturns.

Big Picture: Likely a Better Finish than Start for 2023

The outlook for the global economy and capital markets has improved since the beginning of 2023. There’s still uncertainty and likely sluggish growth ahead, but we think resilient employment data coupled with signs of weakening inflation has increased the probability of a soft landing.

Falling inflation has historically supported risk assets. The income picture looks bright, too. Yields have surged to levels not seen in years and may stay there until central banks start cutting rates.

In the meantime, income opportunities are plentiful, but investors should avoid stretching for higher yields and adding too much risk so late in the cycle. We believe that the best approach is to remain selective, flexible and focused on quality, which should work hand-in-glove within our three broader themes through 2023.