Trending

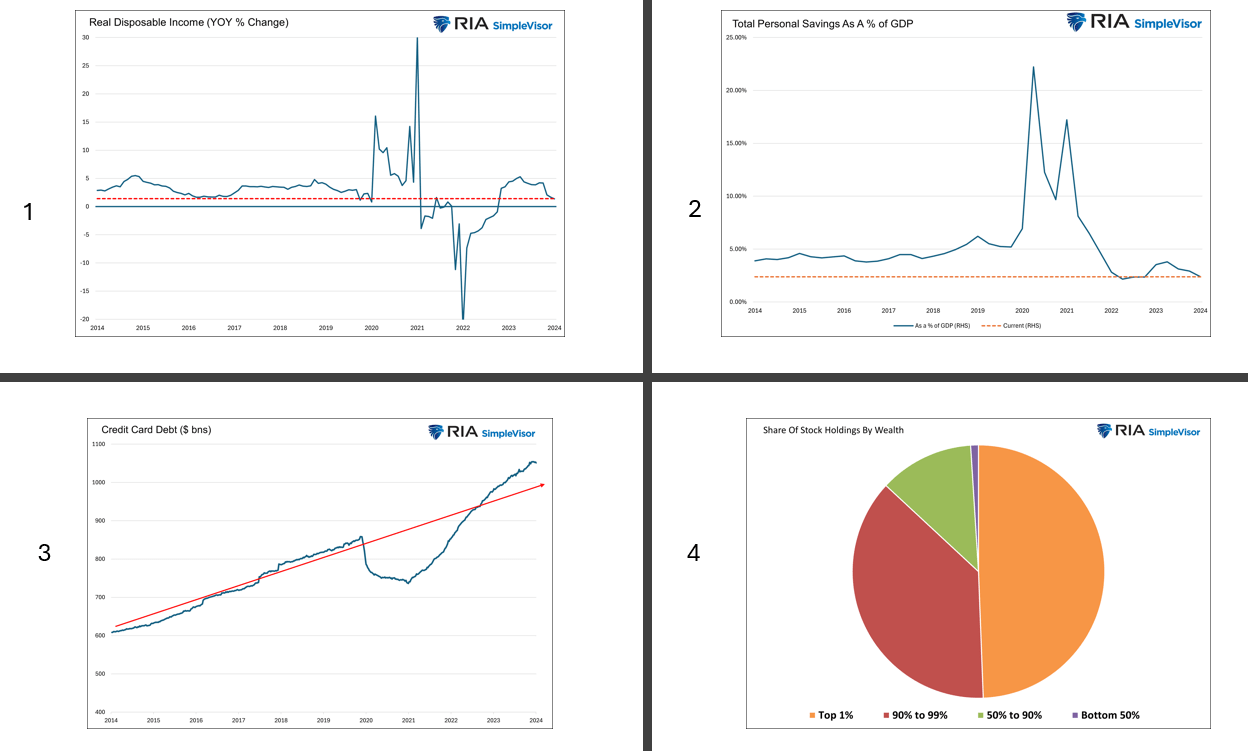

With just a few graphs, we can visualize how economic headwinds are about to get stiffer. Additionally, the graphs help us understand why President Biden has such low economic polling numbers, even among Democrats, despite such a strong economy. There are four predominant means by which consumers can spend. Income is typically the largest and most consistent. Savings and other forms of wealth provide money for spending as well. Lastly, a large majority of consumers borrow to fund their consumption.

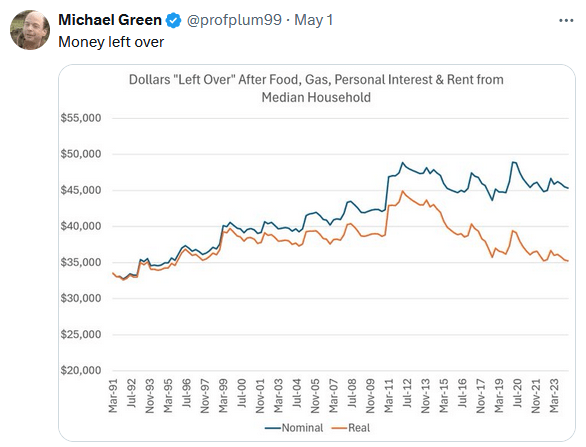

- Real disposable income is now below the lowest levels of the pre-pandemic era. Further highlighting this economic headwind from income is the Tweet of the day with a more inclusive version of real disposable income.

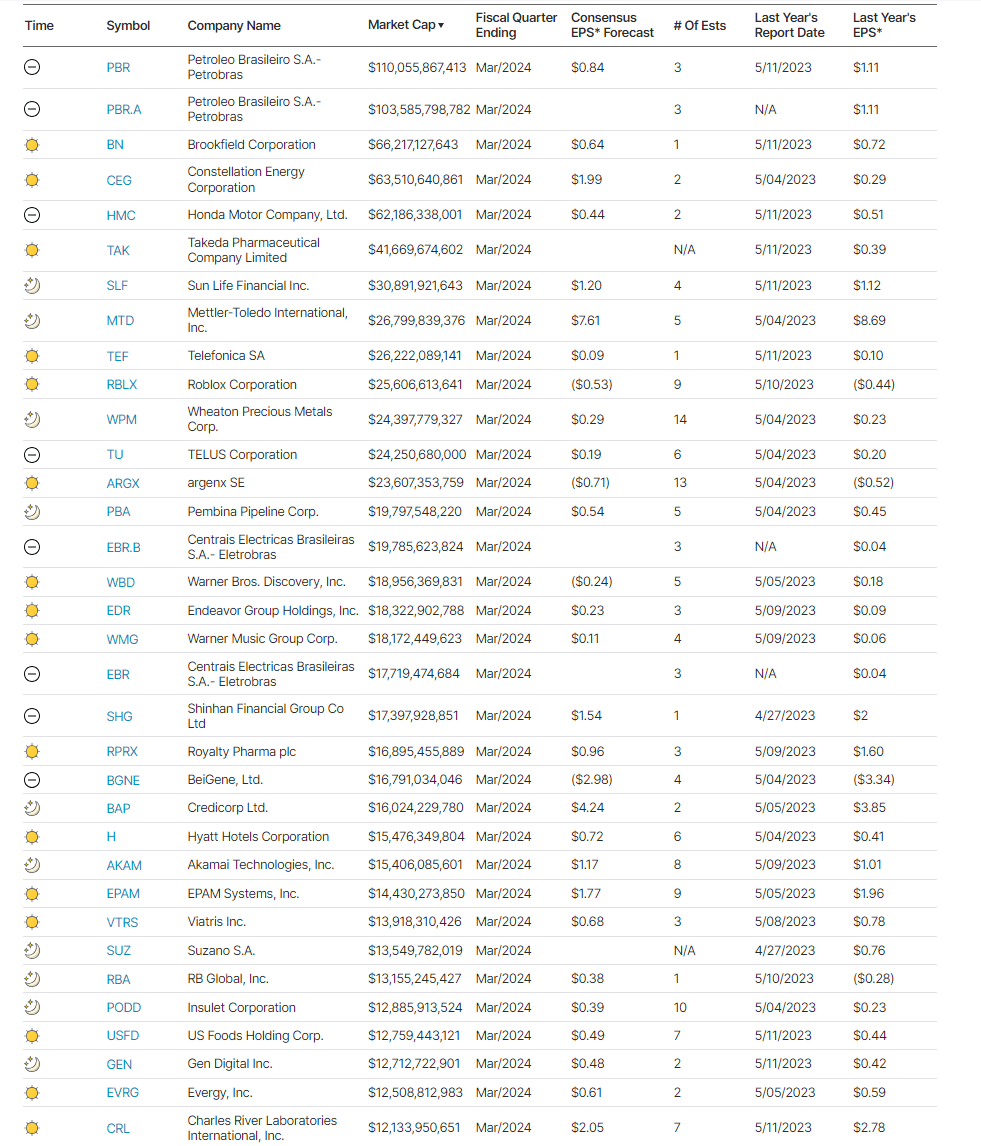

- Extreme fiscal stimulus massively boosted savings, but as shown, the total savings as a percentage of GDP is at 10-year lows. Tuesday’s Commentary further supports this, showing that the pandemic-related excess savings have been depleted.

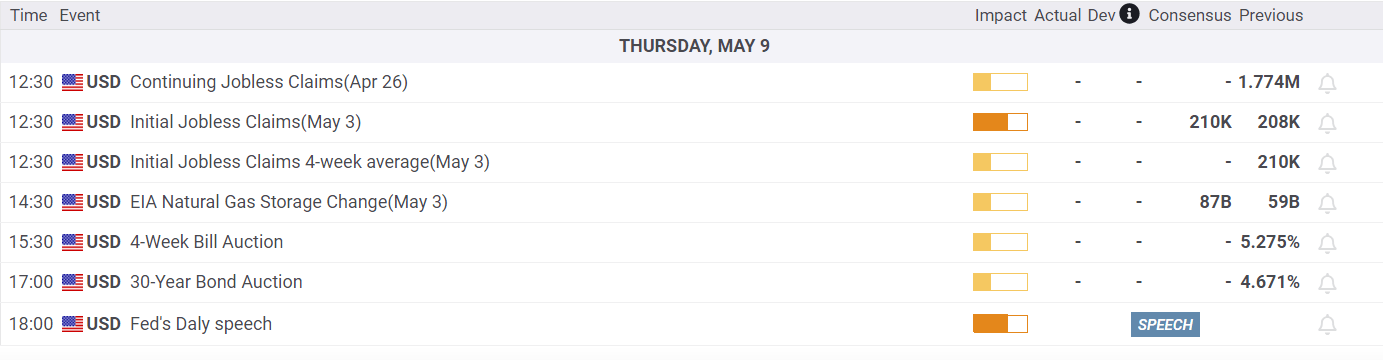

- With limited income and savings, consumers often rely on credit card debt. As a testament to the growing economic headwinds facing consumers, credit card debt outstanding is now growing above pre-pandemic trends.

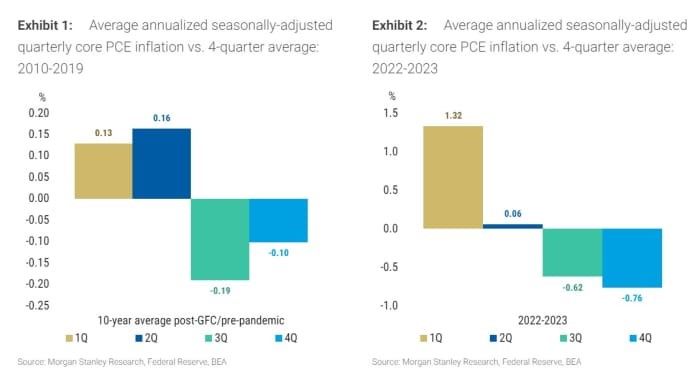

- While asset prices have done very well and enriched quite a few people, the pie chart shows that a significant majority of stocks are held by a small percentage of the population. The benefits are not widespread.

The graphs highlight that consumers, which had been able to spend at above-average rates, are now becoming constrained. Two-thirds of economic activity depends on consumption. The trends below represent a formidable economic headwind.

What To Watch

Earnings

Economy

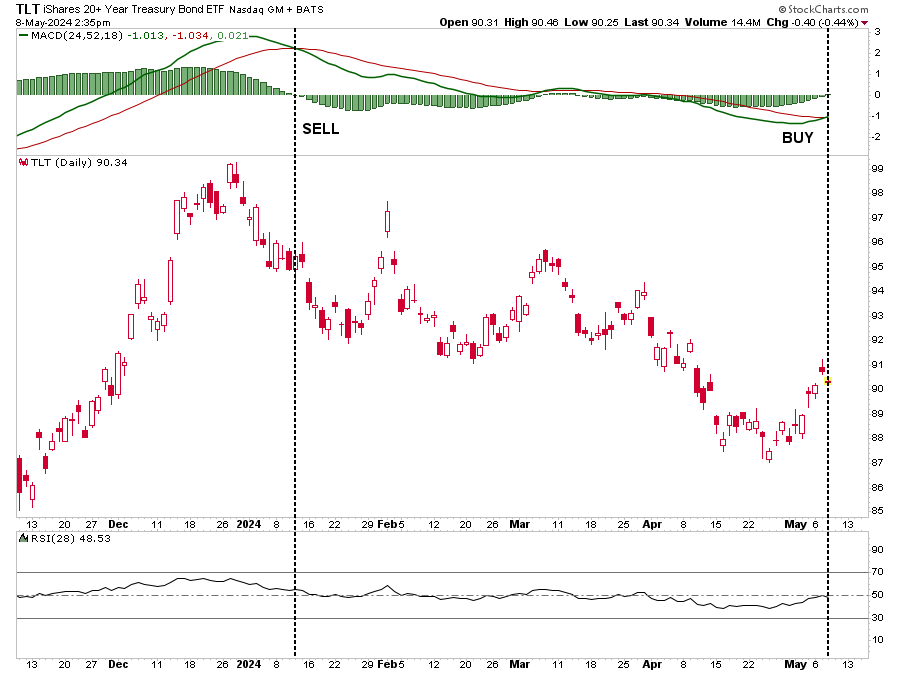

Market Trading Update

Yesterday, we noted that the breakout above the 50-DMA signaled that the recent correction is complete, particularly given the MACD “buy signal” now triggered. However, another buy signal is also in place that may signal another opportunity.

As we will discuss in this weekend’s Bull/Bear Report (Subscribe for free email delivery), Morgan Stanley recently commented on “residual seasonality.” To wit:

“Residual seasonality isn’t a new thing, but what was a small observed factor from 2010 to 2019 has emerged as a giant one now. To quantify the impact, Morgan Stanley employs a technique comparing the average annualized numbers for a quarter to the four-quarter average. For the preceding two years, core PCE prices — the inflation numbers that mean the most to the Fed — have seen a giant 1.32 percentage point boost to first-quarter numbers that erode as the year progresses.

This residual seasonality has also been seen elsewhere, in the employment cost index series and unit labor cost data in the productivity numbers. When so many price metrics display residual seasonality and a similar strengthening pattern, investors would be forgiven for gaining confidence that the pattern will continue in the coming year.

Translated into hard numbers, Morgan Stanley expects the three-month annualized rate of core PCE inflation to fall to 1.81% for the Dec. 2024 data released in January 2025 and the six-month annualized to fall to 1.96%.” – MarketWatch

If that is the case, weaker economic data will start influencing the Fed to cut rates, which supports lower yields. The bond market may already be sniffing out that outcome, as bonds have also triggered a MACD buy signal.

While we will likely see some additional near-term pressure on bonds over the next couple of months, we may be approaching the end of the bond market correction that began in 2020.

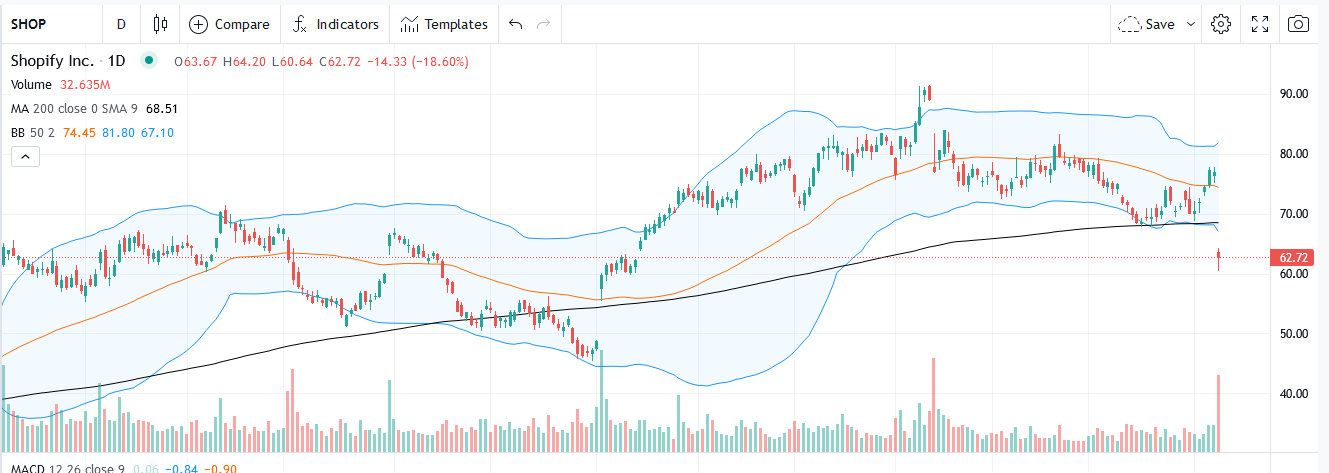

Earnings Season Punishments Were Worse Than Normal

With many companies having reported earnings, there was a definitive theme worth discussing. The theme is highlighted by Shopify and Uber, which fell 20% and 10%, respectively, on Wednesday based on their earnings announcements. To the naked eye, the punishment doled out for weak earnings this past quarter was worse than is typical. BofA confirms this as follows:

Companies that have beat on both sales and EPS outperformed the S&P 500 by 1.1% the next day, slightly lower than the historical average of 1.5%. Conversely, companies that missed got penalized much more than usual, underperforming the S&P 500 by 5.1% versus the historical average of 2.4%.

Druckenmiller Pares Back On AI

Famed investor Stanley Drunkenmiller is selling some of his holdings in the AI space. He is still very optimistic about AI’s potential but thinks that stock prices for companies directly related to AI are a little overdone. Per CNBC:

“So AI might be a little overhyped now, but underhyped long term,” he said. “AI could rhyme with the Internet. As we go through all this capital spending, we need to do the payoff while it’s incrementally coming in by the day. The big payoff might be four to five years from now.”

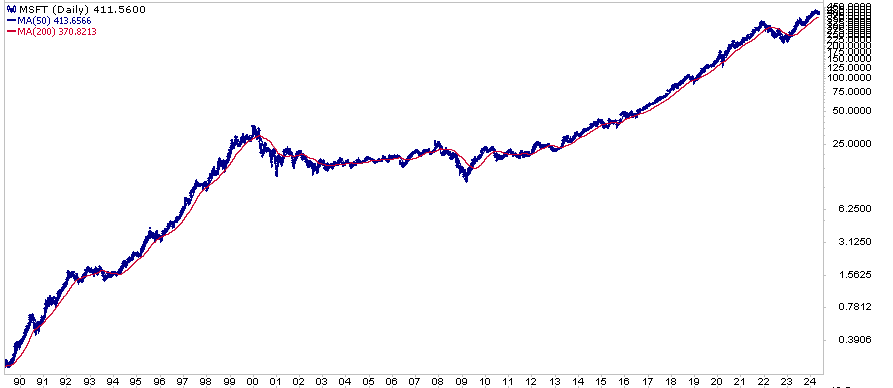

On Squawk Box, he said his fund cut Nvidia and “a lot of other positions in late March.” Drunkenmiller readily admits he is not a buy-and-hold investor like Warren Buffett. Based on the interview, Drunkenmiller thinks AI stocks are great long-term plays but understands that profit-taking can be very rewarding when stocks get too far ahead of themselves. Microsoft, for instance, rose 9400% from 1990 to 1999. While it turned out the company would be a huge beneficiary of the internet, its stock, at the time, rose too far, too fast. The stock would not revisit the 1999 highs until 2014. Since then, it has done extremely well. However, “taking a break” from a hot stock, as Drunkenmiller says, can be smart in the short to medium term.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: Applying Buffett's Logic: Identifying the Next Apple