Trending

Stock bulls aren‘t wavering, and the upswing continues without a pause. Is the move (still) in balance with the relevant markets as one catches up to the other, or is a digestion of prior sharp gains nearby? It didn‘t come earlier this week, and in today‘s article, I‘ll lay down the rising probabilities of seeing at least a short-term pause in the stellar pace of gains since Monday.

Gold pause gave way to selling pressure yesterday, spurred to a degree by the post-Monday‘s trading action. As both metals declined by around 2.5%, this move probably appears overdone to more than a few. Me included, as I called it a kneejerk reaction before yesterday‘s close. In today‘s analysis, I‘ll demonstrate why precious metals investors shouldn‘t be afraid of a trend change – none is happening.

Let‘s dive into the charts (all courtesy of www.stockcharts.com).

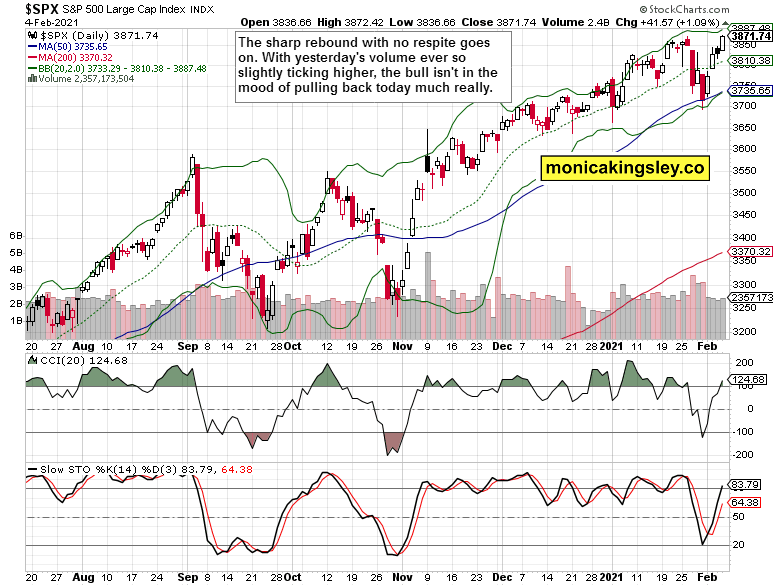

S&P 500 Outlook

Stocks continue higher without stopping, and the daily volume rose a little. The bulls are strong, and took prices almost to the upper Bollinger Bands border amid positive moves in CCI and Stochastics. The daily of daily increases looks set to slow down as minimum though – starting today.

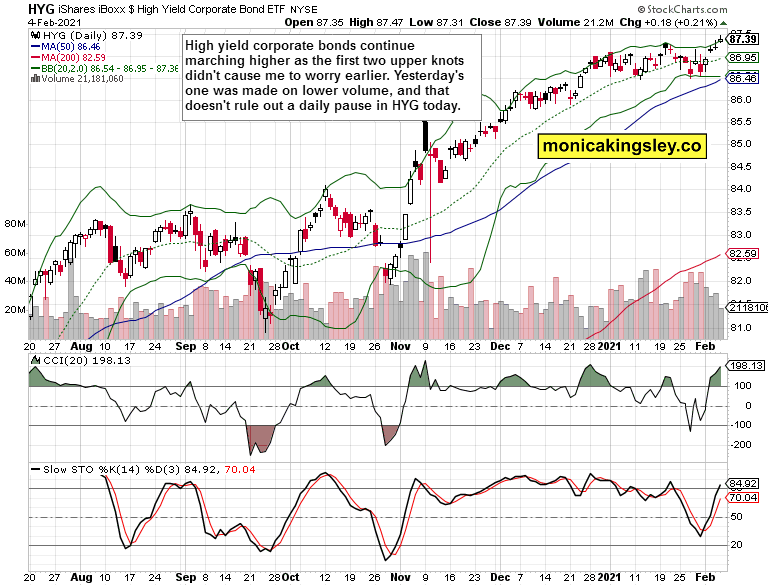

Credit Markets

High yield corporate bonds (HYG ETF) are still pushing higher. While I ignored Tuesday‘s and Wednesday‘s upper knot, yesterday‘s one is arguably a more respectable one, and that‘s because of the drying volume. It wouldn‘t be unimaginable to experience HYG to pause shortly, which would support my prior assessment about SPX.

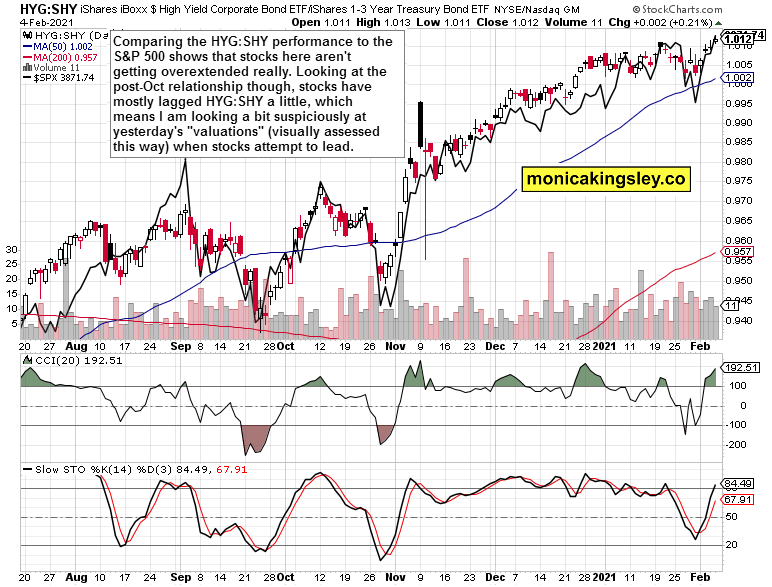

High yield corporate bonds to short-term Treasuries (HYG:SHY) ratio with S&P 500 overlaid (black line) shows that the two are tracking each other tightly in recent days. Actually, stocks are reaching for the leadership position, which given their performance since the start of November is very short-term suspect (stocks have lagged a little relative to the credit markets, and now they‘re trying to lead). That‘s yet another reason why to be cautious about (at least today‘s) trading – and for all the coming days, you know now where to find my daily analyses.

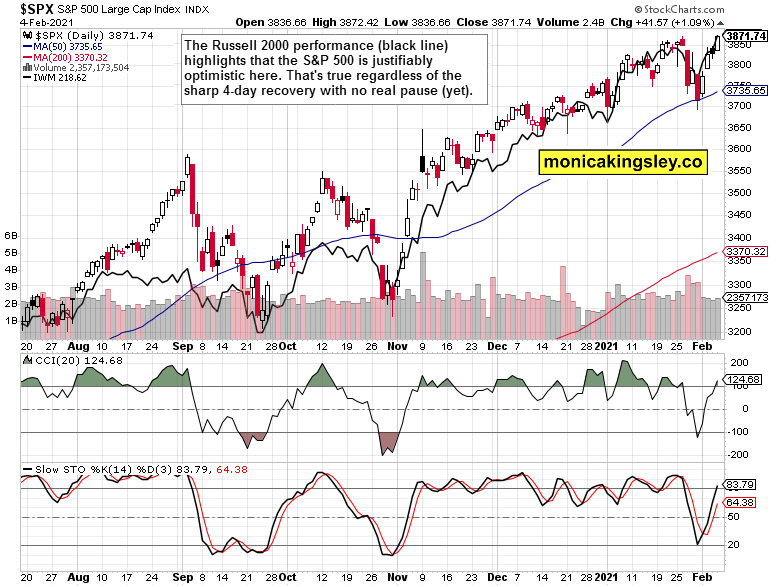

Russell 2000 and S&P 500

Smallcaps aren‘t weakening vs. the 500-strong index in the least, which means that the stock bull market continues unabated. It also disproves the recent significant correction ahead calls on the internet that aren‘t hard to come by. Here we are after Friday‘s bloodbath that I called as out of whack with the internals, here we are at new index highs, this soon.

In yesterday‘s analysis, I presented the value to growth ratio‘s message of the rotation from tech into value as value having to try once again. Technology (XLK ETF) had a strong week, so let‘s inspect its performance vs. the smallcaps – see the above chart. It shows that the Russell 2000 (IWM ETF) has carved a nice, almost rounded bottom, and is primed for higher values ahead, which also supports the notion of no stock market top ahead.

Gold in the Spotlight

The yellow metal is attempting to stage a recovery – a modest one thus far as it has been rejected at $1810 earlier. How disappointing is that? We‘ll see at the closing bell (my assumption is that the bulls will prevail today comfortably), but the implications of the moves thus far doesn‘t change my thesis of a break higher from the 5-month long consolidation in the least. It‘s that the technical (not to mention fundamental) factors propelling it higher, are still in place.

The caption says it all – we‘re in the closing stages of the prolonged consolidation, and prices will rebound next, as so many preceding sizable red candles had trouble attracting follow through selling, and yesterday‘s candle is in a technically even more difficult position to achieve that. The moving averages aren‘t seriously declining, and I look for the death cross (50-day moving average puncturing the 200-day one) to fail relatively shortly.

The Force index in gold agrees that we aren‘t seeing a really serious push to the downside here. Look at the start of 2021, how deep it went back then – we‘ll carve out a nice bullish divergence as I look for gold to get serious about turning up. Yes, the Force index won‘t decline as low as in early January.

Silver didn‘t yield all that much ground as the short squeeze got squeezed. The chart is still bullish, and I stand by the calls mentioned in the caption here – a great future ahead for the white metal in 1H 2021 and beyond.

Ratios and Miners

The gold to silver ratio also continues favoring the white metal, whose this week‘s retreat (post-Monday) didn‘t affect the downward trending values in the least.

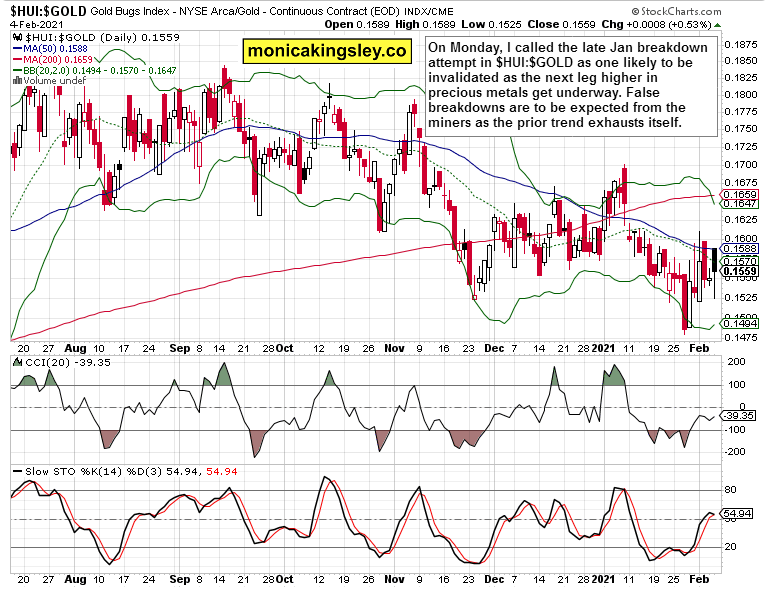

The miners to gold ratio continues supporting my call of breakdown invalidation leading to a new precious metals upleg. I made the calls along these lines both on Tuesday and prior Monday, when I featured my 2021 prognotications on stocks, gold, dollar and Bitcoin – please do check them if you hadn‘t done so already.

Senior gold miners (GDX ETF) are taking a back seat to juniors (GDXJ ETF), andthat‘s a hallmark of bullish spirits returning – first below the surface, then very apparently. While we have to wait for the latter, its preconditions are here.

Summary

The stock market keeps powering higher, and despite the rather clear skies ahead, a bit of short-term caution given the speed of the recovery and its internals presented, is in place even as the stock bull run shows zero signs of having topped.

It‘s time for the gold and silver bulls to reappear after yesterday‘s outsized setback. Crucially, it hasn‘t flipped the short- and medium-term outlook bearish as the factors powering the precious metals bull run, are in place.

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for both Stock Trading Signals and Gold Trading Signals.

Related: Gold Selling Is a Bit Extreme Compared to Dollar and Stocks

The views and opinions expressed in this article are those of the contributor, and do not represent the views of IRIS Media Works and Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.