Trending

Summary

-

The Fed’s decision to slash rates by 1.75 percentage points since late 2024, in the face of stalled inflation progress, signaled to markets that the 2% target had become a secondary priority, fueling consumer exhaustion and “bond vigilante” revolt.

-

Consumer inflation expectations appear to have reached a tipping point. With one-year expectations over 4%, consumers are shifting away from price sensitivity, creating the risk of a self-reinforcing inflationary cycle.

-

As Kevin Warsh takes the chairmanship, he inherits a Fed facing both a crisis in price stability and a legislative threat to its dual mandate.

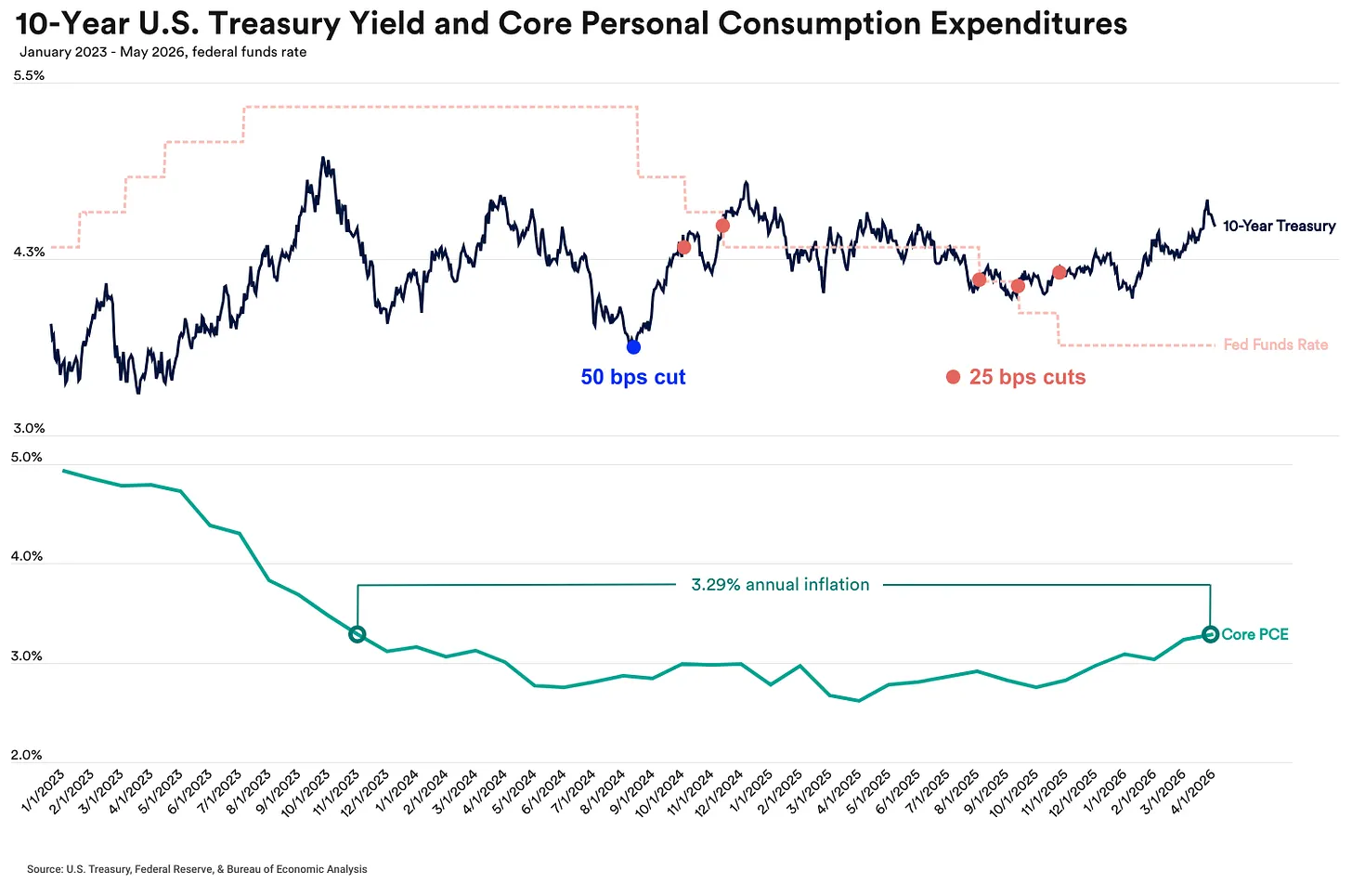

The Federal Reserve is flirting with a credibility crisis that threatens to bake higher prices into the American psyche semi-permanently. Starting in 2024, at the beginning of the current cutting cycle, the Federal Reserve overestimated their progress with beating back inflation. September 2024 marked a rare departure from past precedent, and the Fed unleashed an unexpected 50-basis-point cut to kick off a cutting cycle despite no clear economic crisis on the horizon.

That cut, in addition to the two that followed, sent the bond market running for cover. Starting immediately after the cut, and for the next four months, the 10-year treasury steadily rose, landing a full percentage point higher than before the cuts began. As progress stalled in mid-2025, the Federal Reserve blamed the stubborn inflation on temporary factors like tariff pass-throughs, while asking the public for patience.

Despite a lack of progress on inflation, rates were cut further at the end of 2025. In both cases, a non-recessionary, but mildly stagnating job market distracted from an inflation fight that is now at risk of spiraling out of control again.

It’s time to admit that patience has run out. Current long-term inflation expectations are a direct result of these permissive monetary conditions in the face of numerous economically negative White House actions such as the 2025 tariffs and the recent Iran conflict. Progress on core inflation has reversed again, and consumers are now adjusting for a world where 3% inflation may be the floor rather than the ceiling.

The Psychology of Inflation

The consumer is a powerful driving force within the U.S. economy, and consumer behavior hinges on expectations. When people believe prices will revert to the Fed’s 2% target, they remain price sensitive. However, when they believe supply shocks and rapid price hikes are a permanent feature of the landscape, they start to accept any current price and anticipate hikes which makes inflation worse.

Recent data suggests this mindset shift is already underway. Expectations for where inflation will be over the next one and five years is heading up, not down. Here are two examples:

-

The Michigan Spike: University of Michigan surveys from May show 1-year inflation expectations rose to 4.8% and 5-year expectations hit 3.9%. These are bound to rise further in June’s report.

-

The NY Fed Warning: The New York Fed’s median point predictions (a forecast of single-value expectations) for the 1-year and five-year inflation gauges sit at 4.34% and 3.41%, respectively, in May. April’s five-year report marked the highest reading since data collection began in January 2022.

The decision making during 2025 is an indictment of the Fed’s dual mandate. Core inflation reversed its downward trend, yet the FOMC chose to focus on a cooling labor market. The Fed delivered an additional 75 basis points of cuts into an economy already suffering from tariff price pressure. By prioritizing the employment half of their mandate, they effectively told the American consumer that the 2% inflation target was no longer a priority. The consumer heard them loud and clear and now inflation expectations are breaking.

The Fed has generally relied on a strategy of “looking through” (ignoring) temporary shocks and focusing on the long-term trend. This failed in 2021 when “transitory” inflation became a years-long crisis due in part to the numerous stimulus bills injecting too much liquidity into a supply-constrained economy. The Federal Reserve underestimated the strength and duration of the consumer demand that would be unleashed.

Prior to 2021, the long-term trend was low inflation and the Fed may have assumed that low-inflation environment would resume again naturally. After years of above target inflation, the long-term trend of today is no longer low inflation and therefore attempting to “look through” additional shocks, temporary or not, is willful ignorance of the damage inflation continues to do.

Unfortunately, the Warsh Fed must take action to stop the bleeding by signaling a readiness to return to a restrictive policy stance. Committing publicly to hike if necessary early in his tenure may limit the need to actually follow through with it later in 2026. The stock market might throw a fit, but doing otherwise will continue to normalize this level of inflation within the economy.

A Consumer Tipping Point

The consumer expectations figures should serve as a warning signal to policymakers to stop waiting for a return to the 2010s-era low-inflation environment. If the Fed does not show immediate resolve, the seemingly endless string of supply shocks and consumer fatigue will continue to drive price-setting.

When inflation expectations rise, it creates a self-fulfilling cycle. Households that expect persistently elevated inflation will stop delaying major purchases. They buy today to avoid the “certainty” of a higher price tag tomorrow. This surge in demand, met with constrained supply, keeps upward pressure on the very prices the Fed is trying to cool.

There is no shortage of money sloshing around the economy, and if it’s put into action to avoid the perceived inevitability of rapidly rising prices, then inflation will take on a life of its own.

Corrective Action

The New Warsh-led Fed is heading into a buzzsaw, and Warsh himself is going to find it incredibly difficult to live up to the dovish approach he espoused only months ago. The Federal Reserve’s credibility deficit is rivaling the national deficit. The underlying origin of the upward pressure on price, whether it is oil or tariffs, is secondary to the psychological fallout if the public begins to view 3+% inflation as the new normal. It’s been over five years since we’ve been at or below the 2% target inflation and Americans are tired.

Some members of Congress appear to be taking this situation seriously, introducing Bill H.R. 5396 which would amend the mandate of the Fed to only focus on stable prices, rather than the dual mandate of stable prices and full employment.

Stripping away half of the dual mandate risks leaving the Fed without the tools to prevent spiking unemployment which could come from future economic crises or technological disruptions. If this bill advances, it will require the Fed to defend both its ability and responsibility to balance these opposing goals.

Unless the FOMC moves aggressively to anchor expectations, it risks repeating the post-pandemic blunder of acting too late to stop a trend it mislabeled as temporary. A course correction is clearly necessary. The window to convince the American consumer that the 2% target is still achievable is closing, and the cost of failure will be a permanent loss of purchasing power.

Note: Median point predictions differ from the median expected inflation rate collected by the NY Fed. NY Fed Chart Guide.

-

Median point predictions ask respondents what the rate of inflation will be as a single-value forecast.

-

The median expected inflation rate asks respondents to select a percent chance inflation will fall between a variety of ranges.

Related: Searching for Yield? Vanguard's New High-Yield Bond ETF Deserves a Look