Trending

Written by: JB Golden | Advisor Asset Management

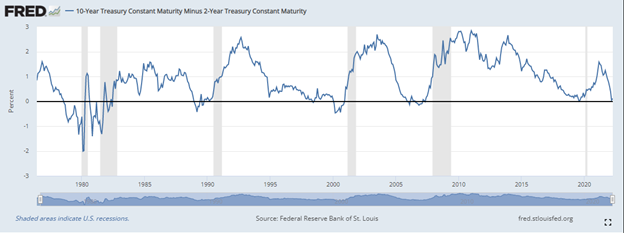

After a pronounced flattening lasting the entire first quarter (Q1) of the year, the yield curve — as measured by the spread between the 2-year and 10-year U.S. Treasury (“2s-10s spread”) — finally inverted as the second quarter of the year kicked off. The 2s-10s spread began the year at approximately 90bps (basis points), not far off the 100bps average over the last 40 years. However, with inflation at levels not seen in decades, souring consumer confidence, concerns over slowing growth and the war in Ukraine all weighed on markets in Q1 pushing the 2s-10s spread to inversion by the end of the quarter. The inversion was brief and shallow lasting from March 31 to April 5and touching a low of -8bps on April 1 before steepening to +20bps by April 7. While not necessarily unexpected given the flattening that preceded the inversion, it nevertheless got the market’s attention given the strength of the spread measured as a leading indicator of economic recession. The 2s-10s spread has a strong history of inversion ahead of recession and, as illustrated below, has inverted ahead of every recession since 1980.

It should not come as a surprise that the yield curve reflects concern over the strength of future economic growth. Q1 2022 has brought unknowns seemingly around every corner. When and/or will the highest inflation in decades roll over? What will be the ultimate outcome and future impact on financial markets given the situation in Ukraine? Can the consumer handle higher rates and slowing growth? Will the Federal Reserve be able to engineer a soft landing? The only certainty seems to be uncertainty and thrown into the mix we have now had a yield curve inversion raising concerns that we could be headed for a recession. As one might expect given such uncertainty, there are also a whole host of opinions on what the inversion signals and what the consequences might be for financial markets. Is this time different? Should we disregard the signal given the shallow and brief nature of the inversion? While recession may not come to pass it behooves investors to take the signal seriously.

There is certainly no lack of research on the importance of yield curve inversions as a leading indicator. Anecdotally, it seems likely it could be one of the most poured over concepts in the balance of financial markets. The St. Louis Federal Reserve alone has produced 70+ publications and 120+ working papers on the concept and there are some important inferences that can be drawn. First, it is important to understand that yield curve inversion is a leading indicator and, in fact, there can be quite a long lag time between inversion and recession. A yield curve inversion does not necessarily imply a recession is imminent nor does it imply anything about the depth or duration. The average lag time between inversion and recession is about 15 months.In addition, while it may seem counterintuitive, equities generally perform quite well post inversion. Equity markets tend to peak approximately one year after yield curves invert and the average performance of the S&P 500 from inversion to peak over the last seven inversions has been 15%; for comparison, the 10-year U.S. Treasury has averaged a meager 1% return. Finally, it isn’t shocking that we have seen a strong flattening and briefly inverted yield curve in Q1 when considering where we are at from a monetary policy standpoint. The Federal Reserve has been messaging aggressive tightening for some time culminating in the March meeting rate hike to likely have been the first of many. Alongside rate hikes, the Fed will likely begin to reduce the size of their $9 trillion balance sheet via quantitative tightening in short order with a framework announced in the Fed Minutes last week. Monetary policy shifts tend to impact the short end of the yield curve the most. The sharp move up in 2-year Treasury yields this year, which is one of the main causes of yield curve inversions, is certainly not abnormal. The yield curve has flattened during each of the last seven rate hike cycles with the 2-year moving up faster than the 10-year, however, what is unique this time around is the pace at which the curve has flattened, occurring much earlier than in previous tightening cycles. Also unique to this cycle is the higher levels of inflation, something the markets and the Fed have not had to deal with in a very long time. It could take significantly higher rates to get inflation under control.

It does not look like the Fed will be able to provide any further backstop for financial markets. This represents a bit of a regime change on the part of the Fed as market volatility has been a consideration for some time. The so-called “Powell Put” — the notion that the Federal Reserve would only let markets fall to a certain point before stepping in with stimulus — is likely now dead. The flattening and inversion of the yield curve is signaling to markets that the Fed wants to act fast and aggressively in tightening monetary policy and unwinding the balance sheet. The labor market is overheating with wages rising at almost twice the post-2008 average and close to two jobs for every one job seeker. In addition, inflation is rising at the fastest pace in almost 40 years. The Federal Reserve is not in a position to consider market volatility. The old mantra “Don’t Fight the Fed” might be more aptly put in today’s market as “Don’t Get Steamrolled by The Fed.” Those areas of the market that have been supported for the last decade by easy monetary policy and quantitative easing could be in for a rough ride. Look no further than longer-duration fixed income holdings to see the volatility at work. The 10+ year band of the U.S. Aggregate is down over 14% year to date. One could also point to high-growth equities with no cash flows as an area that might be in the Fed’s crosshairs as higher rates and tighter monetary policy are likely to weigh on valuations. Consistent and sustainable income-producing investments, whether it be in the form of dividends or interest income should be considered, in our opinion. Longer-duration equities, which tend to be those with little to no cash flows, and longer-duration fixed income could continue to see volatility until the Federal Reserve reigns in inflation. A focus on defensive duration alongside a heavier emphasis on income could be warranted in our view. At the end of the day the yield curve may not be signaling recession, but it does seem to be indicating an inflection point regarding monetary policy and the potential end of the quantitative easing era. If there is one actionable takeaway from the flattening curve and brief inversion it is get out of the way of the Federal Reserve.