Trending

Imagine if someone asked you how hot it was in America last month. How would you respond to such a vague question? As everyone knows, temperatures vary greatly depending on a number of factors, from region to elevation, from time of year to even time of day.

Is the person inquiring about the temperature in Flagstaff, Arizona, in the early morning of Wednesday, May 3—or in Fargo, North Dakota, in the late evening of Sunday, May 28? Are they looking for an answer in Fahrenheit or Celsius?

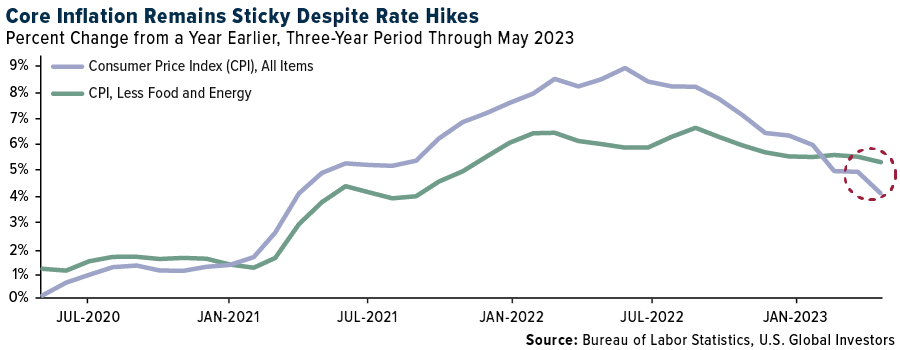

Most people would agree that the “temperature in America last month” question is absurd, but this is more or less what we get with regard to inflation. Once a month, the Bureau of Labor Statistics (BLS) releases its headline consumer price index (CPI), which is supposed to give us some idea of how much or how little consumer prices changed compared to last month and last year.

This week’s CPI, for example, shows that prices in May continued to increase year-over-year, but at a much slower pace of 4%, down from nearly 9% in June of last year.

This makes it seem as if the Federal Reserve’s efforts to bring down inflation by hiking rates are working, but if we strip out volatile food and energy prices, the picture isn’t as rosy. The so-called core CPI—which measures everything except food and energy—shows that prices on average barely budged from May 2022 to May 2023.

I should add that the BLS has continued to revise its methodology over the years. If we still used the 1980s methodology, annual inflation would be closer to 12% than 4%.

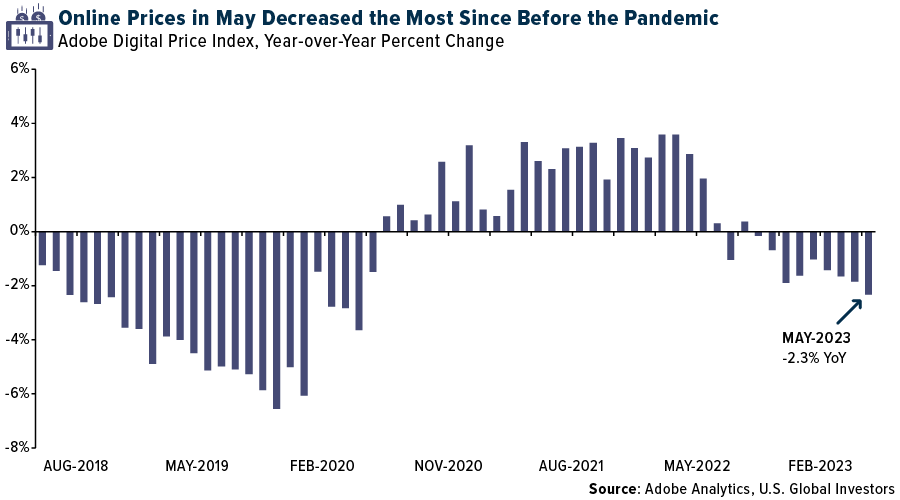

Online Prices Saw Largest Monthly Decline Since Start Of Pandemic

Again, just like temperatures, prices can vary significantly state-to-state and even city-to-city. According to the American Automobile Association (AAA), the current average price for a gallon of gasoline is $3.00 in Mississippi, making it the cheapest in the country. In California, by contrast, a trip to the pump will cost you $4.87 per gallon on average, or nearly $2 more.

Similarly, prices can be higher or lower depending on whether you purchase something from a brick-and-mortar store or an online retailer. For years, the joke was that big-box retailers like Best Buy had become a showroom for Amazon. Have your eye on an expensive surround sound system? Best to experience it in person before buying it for cheaper online.

That said, the CPI only measures “offline” prices. BLS workers literally visit or call physical stores to get the price of select items.

For changes in online prices, we can turn to Adobe—the maker of the portable document format, or pdf, and Photoshop. Contrary to what you might think, Adobe is uniquely qualified to report on inflation trends, as its marketing and web analytics arm tracks an alleged 1 trillion visits to online retailers and over 100 million products across 18 different categories, from electronics to jewelry.

According to the company, online prices fell 2.3% in May compared to the same month last year. To clarify, prices didn’t just slow down, they got cheaper, and at the fastest pace since the start of the pandemic. Among the product categories that decreased the most were computers (-16.45%), electronics (-12.04%), appliances (-7.86%) and sporting goods (-7.39%). Categories that increased in price over the 12 months were personal care products, tools and home improvement, medical equipment, nonprescription drugs, clothes, groceries and pet products.

Will Fed Action Trigger Another Crisis?

My point in sharing this with you is to make it clear that measuring changes in consumer prices is a messy, imprecise undertaking, one that can result in conflicting data, as the difference between offline and online prices shows.

And yet these data are used by both the public and private sectors to guide important policy decisions, including cost-of-living adjustments, Social Security payments and more.

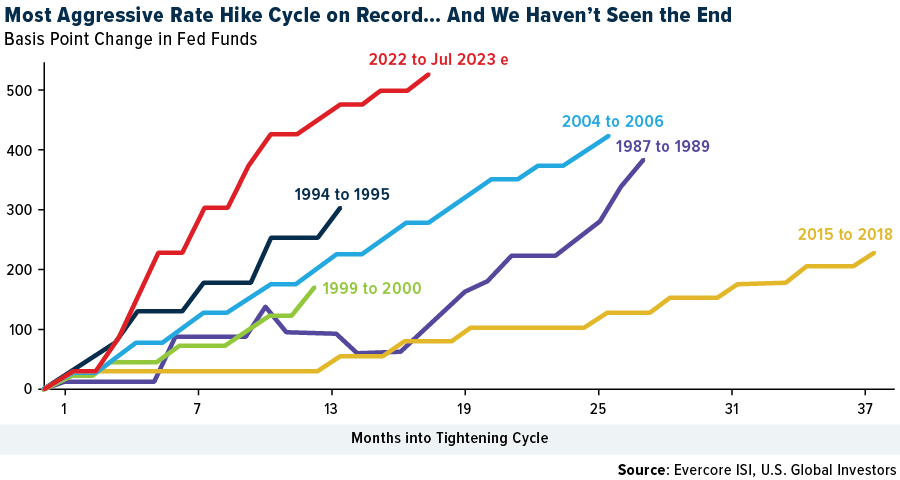

In perhaps the most well-known example, the Fed uses BLS data to inform monetary policy. This week, the central bank elected to leave rates the same but indicated it may need to raise them at least two more times this year, despite the fact that this tightening cycle is already the most aggressive since at least the 1987-1989 cycle.

As Evercore ISI’s Ed Hyman put it this week, if we take the Fed’s balance sheet normalization into consideration, today’s effective rate is really around 6%. The regional banking crisis may be behind us, Hyman says, but the risk of “another financial shock/crisis in another area” rises as rates remain on an upward trajectory.

Preparing Your Portfolio For A High-Inflation, High-Interest Rate Environment

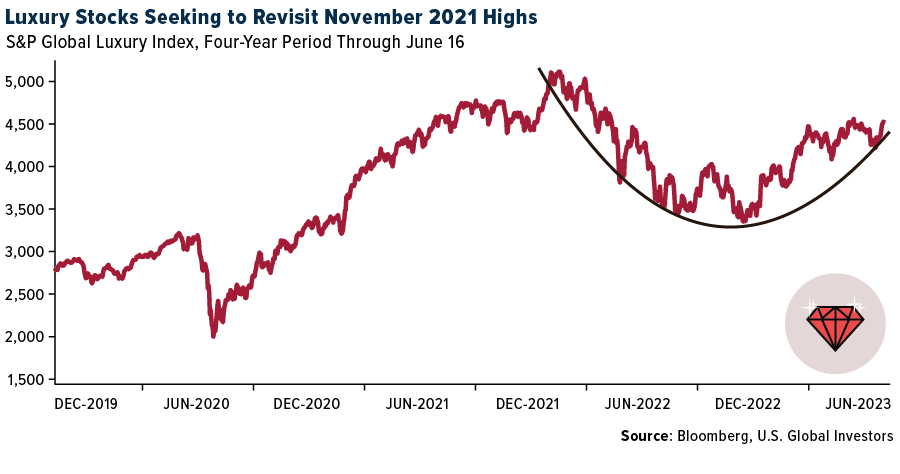

It may be impossible to say that any asset class or investment is immune to the kind of volatile swings in inflation and interest rates we’re seeing today, but luxury stocks are a strong contender, I believe.

Because luxury brands tend to have decades of name recognition behind them, and because they limit supply, they’ve historically had incredible pricing power, able to raise prices without severely impacting demand from mostly affluent consumers.

Many luxury items have themselves been smart investments, with Hermès’ famous Birkin bag often outperforming the S&P 500 and gold. Between 2011 and 2021, the price of pre-owned Rolex watches beat advances in the stock market, gold and real estate.

The S&P Global Luxury Index, up a little over 20% year-to-date, is still below its all-time high set in November 2021, making now an attractive buying opportunity, according to Bank of America (BofA).

Companies in the luxury industry are “likely” to continue beating earnings expectations as profits remain strong on buoyant sales, BofA analyst Ashley Wallace said in a note this week.

“Historically, pullbacks in the sector have been buying opportunities and this time will likely be no different,” Wallace wrote, adding that demand in China has continued to exceed expectations despite an underwhelming economic reopening.

BofA’s top luxury picks include LVMH, Europe’s largest company after surpassing $500 billion in market cap this year; Cartier-owner Richemont; and Hermès.

If you missed my slideshow on the 10 most popular luxury brands online, click here!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.25%. The S&P 500 Stock Index rose 2.76%, while the Nasdaq Composite climbed 3.25%. The Russell 2000 small capitalization index gained 0.36% this week.

- The Hang Seng Composite gained 3.23% this week; while Taiwan was up 2.38% and the KOSPI fell 0.58%.

- The 10-year Treasury bond yield rose 2 basis points to 3.764%.

Airlines And Shipping

Strengths

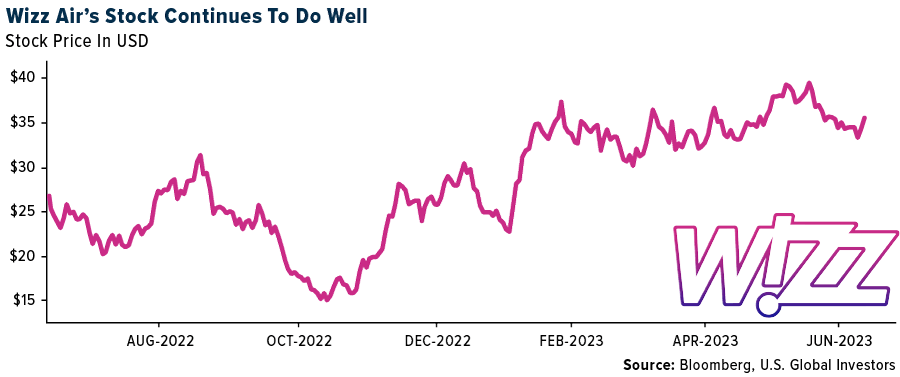

- The best performing airline stock for the week was Skywest, up 13.6%. Wizz Air introduced its fiscal year 2024 estimate net income guidance of €350-450 million, which was 34% above consensus estimates. This implies a €1billion increase in net income from fiscal year 2023 levels. Wizz remains confident of an improvement in utilization and productivity, resulting in CASK ex fuel declining year-over-year.

- JPMorgan sees evidence of capacity discipline year-to-date, including: 1) slow steaming; 2) a pickup in scrapping, which should accelerate in the second half of the year due to the new emissions standards; 3) slippage in new vessel deliveries year-to-date, serving to balance the sluggish demand and oversupply concerns. There are also fresh risks arising from labor disruption at U.S. West Coast ports since June 2 and drought conditions.

- Air Traffic Liability “ATL” as a percentage of total liquidity has declined from an average of 70% in the first quarter of 2019 to 61% in the first quarter of this year. Only GOL, Azul, and, to a much lesser extent, JetBlue have seen this metric deteriorate meaningfully. ATL as a percentage of TTM revenue has increased from 16% in 2019 to 22% in 2023, likely due to the post-pandemic recovery in demand. Interestingly, the Big 4 U.S. airlines and JetBlue have historically been comfortable maintaining a lower liquidity position relative to ATL.

Weaknesses

- The worst performing airline stock for the week was Copa, down 0.3%. Spirit Airlines cut capacity by 11% and 9% in September and October, respectively. This is the second meaningful cut to the airline’s schedules in the past three weeks. Spirit’s third quarter capacity is now tracking 6% below consensus. JetBlue reduced its capacity 370 basis points (bps) and 140bps in September and October, with cuts seen across the network, including cuts in Europe.

- Clarkson’s Broking revenue should be fairly closely linked to the Clarksea Index, albeit likely with a proportionately lower weighting to containerships. The index is now at $22,212 per day, down 46% year-over-year on a spot basis after reaching a recent high of $44,357 per day, in May 2022. The decline in the Clarksea Index in recent weeks has been driven by both lower Tanker and Dry Bulk earnings, which may be partly seasonal.

- Australia’s competition regulator put the airline industry firmly in the spotlight this week, calling for an ombudsman and for the government to break up the skies and provide relief for travelers at a time of record high airfares. It came as Qantas Airways caused a stir when it said international flight capacity wouldn’t match surging demand until 2028. Airlines are dusting off their planes and bringing them out of desert storage facilities, such as this one in Alice Springs, as travel starts up again globally. Travelers, meanwhile, are paying about 50% more for international flights than before the pandemic.

Opportunities

- Travel budget expectations continue to noticeably improve in 2023, with improvement expected to continue into 2024. Travel managers expect their budgets to be up 11% versus 2022 in the first half of the year and up 9% versus 2022 in the second half of the year, on average.

- According to UBS, April / May data points suggest a sequential improvement in freight volume trends versus the first quarter. This is partially explained by lower comps but also by an underlying improvement of trends versus 2019 levels. Volume declines in ocean have decelerated to low-single digit year-over-year, with East – West routes down 4% year-over-year in April versus down 9% on average September-February, and May air volume declines are down high single-digits year-over-year.

- Corporate volumes have continued to trend around 75-80% recovered, led by SMBs rather than larger corporations. In fact, several airlines have noted SMBs have been over 100% recovered versus 2019 levels. Even if corporate volumes do not fully recover this year, they will be 100% recovered on a revenue basis. There could be continued normalization of corporate travel returning to and exceeding pre-pandemic levels in 2023.

Threats

- The ACCC has released its 12th and final Airlines Competition in Australia report for June 2023. It notes that domestic airfares declined 14% in real terms from February 2023 to May 2023. Despite these falls, fares remain 13% higher than pre-Covid in real terms and 32% higher in nominal terms. The fall in pricing can be somewhat attributed to a return of capacity to the system and the reduction seen in fuel prices. In May 2023 international arrival and departures recovered to 81% and 79% of pre-pandemic levels, respectively.

- Morgan Stanley expects effective supply growth to be 6.0% year-over-year in 2023 and 9.0% in 2024 for total containership capacity, and to be 8.2% year-over-year in 2023 and 11.4% year-over-year in 2024 for vessels above 8000 TEUs. That’s well beyond the 2.5% demand CAGR over 2011-2022 – and, as they note, visibility on demand resumption is low.

- European flight activity declined by two points to -8% of 2019 levels in the week. Ryanair flights were impacted by French air traffic control strikes. Heathrow airport will face disruption because of pay strike action by the Unite union for 31 days spread across the summer. Daily website visits for EU airlines improved by three points to -2% versus 2019 levels on a seven-day trailing basis in the week.

Luxury Goods And International Markets

Strengths

- Berenberg’s Research Team upgraded Estee Lauder to a buy from a hold on the expectation that China will continue to recover and the country’s demand for cosmetic goods will improve. China generates about 40% of Estee Lauder’s sales.

- A mansion is for sale in Dubai for 750 million dirhams ($204 million), making it the most expensive house on the market in the city. The Dubai property market has been gaining momentum for years. The city was able to reopen quickly, benefiting from cities like Hong Kong, which stayed under Covid restrictions much longer. In addition, Dubai’s property sector was supported by the inflow of wealthy Russians after Russia invaded Ukraine.

- Faraday Future Intelligence (an EV car maker) was the best performing S&P Global Luxury stock in the past five days, gaining 36.5%. Shares continued to climb after the company announced the production of the long-awaited FF 91 2.0, with a price tag of $309,000, which will be limited to 300 units available globally.

Weaknesses

- China reported weaker economic data for the month of May. Industrial output grew 3.5% year-over-year, slowing from April’s 5.6%. Retail sales rose 12.7%, slowing from 18.4% growth in April, and below the expectation of 13.6%. Fixed investment grew 4.0% year-over-year, less than market expectations of 4.4%. Unemployment remained at a 16-month low of 5.2%, but youth unemployment climbed to 20.8% from 20.4% in April. Property investment declined 7.2% in the first five months of the year, worse than the 6.2% decline in the January-April period.

- The ZEW Indicator of Economic Sentiment for the Eurozone dropped to -10.0 in June from a reading of -9.4 in May. “Experts do not anticipate an improvement in the economic situation during the second half of the year,” ZEW president Achim Wambach said, warning of persistent headwinds as export-focused sectors struggle with a weak global economy.

- Star Entertainment, an Australian casino operator, was the worst performing S&P Global Luxury stock in the past five days, losing 6.3%. The opening of the multibillion-dollar Queen’s Wharf development has been delayed for the fourth time in 18 months. Star has projected that the Brisbane River development will attract 1.39 million visitors per year.

Opportunities

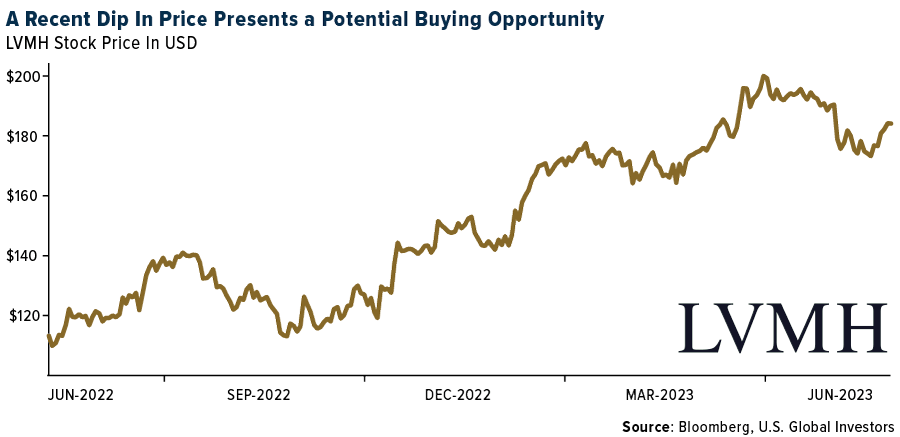

- The luxury sector was under pressure in the month of May, with most equities correcting. Shares of LVMH, a super luxury player, declined almost 9%, presenting a potential buying opportunity. Bank of America’s luxury research team believes that this sector will continue to beat earning expectations and sees its profit estimates being upgraded. The broker’s top picks are LVMH, Richemont, and Hermes.

- Inditex SA demonstrates strength through its successful strategy of expanding larger Zara stores, resulting in a 43% jump in operating income and a record first-quarter gross margin. By focusing on bigger locations and implementing new technology such as a more efficient security system, Inditex has achieved increased productivity and faster checkout times, as seen in the 20% rise in Zara’s entry prices and a remarkable 30% stock gain. Moreover, the company’s disciplined cost management has allowed for a substantial cash pile of over €10 billion, supporting dividend growth and a €1.6 billion investment plan, including 30 store openings and renovations in the U.S. by 2025.

- This week, China cut its seven-day repo rate by 10 basis points from 2% to 1.9% and the medium landing facility rate was cut by 10 basis points as well, from 2.75% to 2.65%. The country reported weaker economic data for May which may prompt the Chinese government to provide additional stimulus.

Threats

- Mercedes-Benz faces the threat of potential credit risks associated with its leasing practices. Despite Mercedes-Benz Mobility’s improved leasing use below the global peer average, the company’s credit rating continues to be penalized due to the level of leasing at its finance unit. With a significant number of operating leases expected, a drop of 8% above the company’s used-vehicle price value could potentially wipe out 2023 profitability, as observed in similar past instances. The reliance on operating leases, which constitute approximately 19% of Mobility’s asset base and 1.9x equity, poses a potential threat to asset quality and residual risk fluctuation.

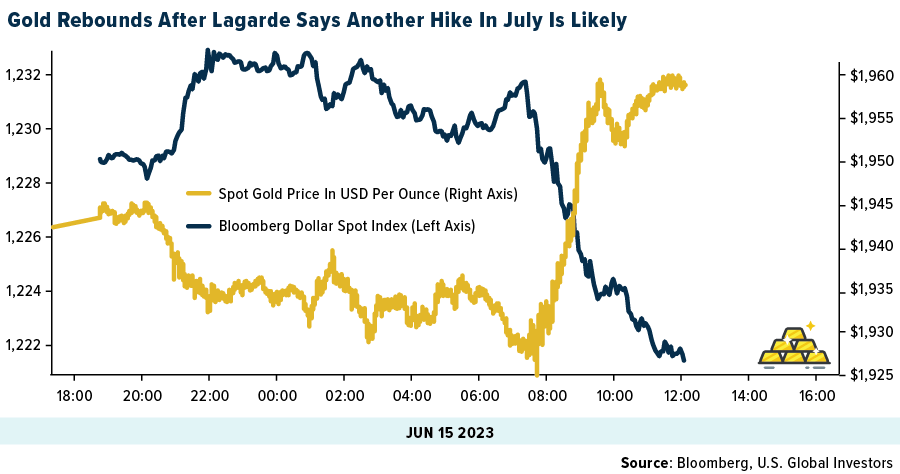

- While the Federal Reserve left rates unchanged in the U.S. this week, the European Central Bank (ECB) hiked rates on Thursday by 25 basis points. Head of the bank, Christine Lagarde, said that another increase should be expected in July as prices remain well above the bank’s target of 2%.

- Next Friday, the preliminary S&P Global U.S. Manufacturing PMI for June will be reported, and most Bloomberg economists expect the index to remain below 50, in contractionary territory. The index fell from 50.2 in April to 48.4 in May, as manufacturing activity declined in the United States as new orders plummeted on higher interest rates.

Energy And Natural Resources

Strengths

- The top-performing commodity this week was natural gas, which rose by 16.19%. U.S. natural gas futures spiked, driven by expectations of increased demand for power-generation fuel due to forecasts of hotter weather. Predictions of a heatwave in Texas, combined with an upsurge in cooling demand, offer favorable circumstances for a rise in natural gas prices. In addition, oil prices strengthened, with West Texas Intermediate (WTI) trading above $70 a barrel. Factors such as a weaker dollar, anticipated additional stimulus in China and a modest weekly gain boosted positive sentiment in the oil market.

- The oil market’s robustness was further supported by news that the U.S. intends to purchase approximately 12 million barrels of oil this year to replenish its depleted emergency reserve. Falling crude prices offer the government an affordable opportunity to refill the Strategic Petroleum Reserve (SPR). This action not only contributes to energy security but also helps stabilize oil prices, benefiting the domestic oil industry.

- A key strength in Glencore’s strategy is its ability to offload the operational risks of mining to a third party. The sale of Glencore’s stake in the Cobar copper mine in Australia for $875 million in cash and share consideration has enabled it to streamline its portfolio and concentrate on its core strength: commodity market trading. The infusion of cash and the ongoing off-take agreement for the copper concentrate enhance Glencore’s financial stability and future revenue streams.

Weaknesses

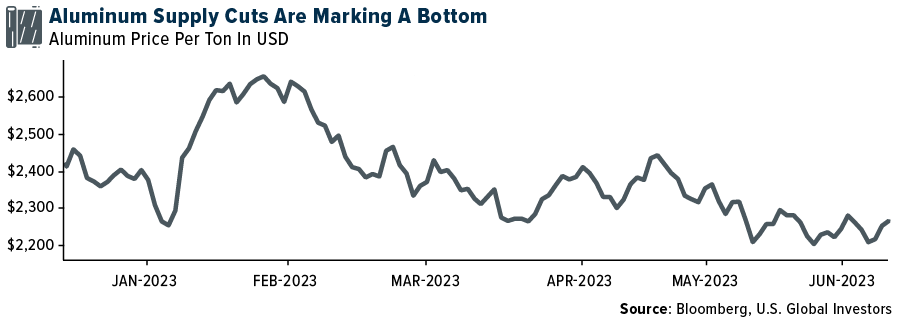

- Coffee was the worst-performing commodity this week, declining by 3.16% due to minimal news. The global aluminum market remains in a deficit, primarily due to supply constraints. With hydro power generation in China shrinking year over year, this poses a problem for approximately 20% of the country’s smelters. In Europe, while the energy crisis’s immediacy has lessened, many operators remain marginal, such as Aldel, which recently decided to permanently close its 120kt smelter in the Netherlands.

- Goldman Sachs’ warning about enduring issues in the Chinese real estate sector and its potential to act as a multiyear drag on the economy suggests vulnerabilities for investments in iron ore, which declined nearly 5% on the news. Reduced demand for steel-making ingredients due to weaknesses in the property sector could result in lower iron ore prices, affecting the profitability of iron ore production companies and impacting investor returns and market sentiment.

- The resignation of Codelco’s CEO, amid the company’s lowest copper output in a quarter-century and rising costs, points to problems in the copper sector. Delays in mining operations, setbacks in development projects, and falling production and profitability could pose risks to investors in copper companies, potentially causing a drop in stock prices and undermining investor confidence.

Opportunities

- Rio Tinto’s investment of $1.1 billion to expand its aluminum smelter in Quebec, Canada, using low-carbon technology, opens up an investment opportunity. The adoption of such technology aligns with the growing focus on sustainability and environmental responsibility. This investment underscores Rio Tinto’s commitment to the aluminum business, which could contribute to its long-term growth and profitability.

- As per a recent Barron’s story titled “Copper Is the Future. Freeport-McMoRan Is the Stock to Buy,” the expected long-term role of copper in the global energy mix, driven by the adoption of electric vehicles and alternative energy sources, presents an investment opportunity. Freeport-McMoRan, a copper miner, is well-positioned to take advantage of rising copper prices due to its strong fundamentals, which include a solid balance sheet and the capacity to return capital to shareholders. The potential for a sustained copper cycle and the company’s ability to capitalize on higher copper prices may lead to enhanced investor returns.

- Unusually extensive wildfires in Canada, which have been affecting logistics and forestry operations, present certain investment opportunities. The effect on pulp production has been limited so far, though risks persist, especially considering Canada’s already tight wood availability. Despite these conditions, there has been minimal impact on the overall pulp supply/demand balance. As a market update, producers have successfully implemented a $30-40/ton hardwood price increase in China.

Threats

-

Record-breaking ocean warmth in April and May, combined with the highest global temperatures for early June ever recorded, underscore the escalating risks of climate change. Rising temperatures may lead to extreme weather events such as heatwaves, droughts, and wildfires, which can disrupt agricultural activities and affect commodity and energy prices. The potential effects of climate change, coupled with the return of the El Niño phenomenon, introduce uncertainties and risks for various sectors, including agriculture and energy.

- The International Energy Agency’s forecast of slowing oil demand growth and the potential peak of demand within this decade pose a threat to the oil industry. Factors like high oil prices and the transition to electric vehicles contribute to this slowdown. The shift toward clean energy and the increasing focus on reducing greenhouse gas emissions may have long-term implications for the oil market, possibly leading to diminished demand and challenges for oil producers.

- The proposed carbon limits for coal-fired utilities and the requirement to implement carbon capture technology pose a threat to the coal industry. Critics argue that this technology is unproven and expensive, which could result in increased energy costs, affecting energy affordability and reliability. The tension between emission reduction and the feasibility of implementing costly control technology could create challenges for coal plants and the broader industry.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Stacks, rising 13.25%.

- Rapper and entrepreneur Snoop Dogg has launched a new non-fungible token (NFT) collectible series that will evolve in utility as he goes on tour this summer. The NFT will grant holders access to behind-the-scenes content exclusive merch, art, and experiences, writes Bloomberg.

- Bitcoin’s share of the total crypto market is the highest in about 20 months, a sign of the cautious mood in digital assets and dominance of Bitcoin again, according to Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Polygon, down 4.07%.

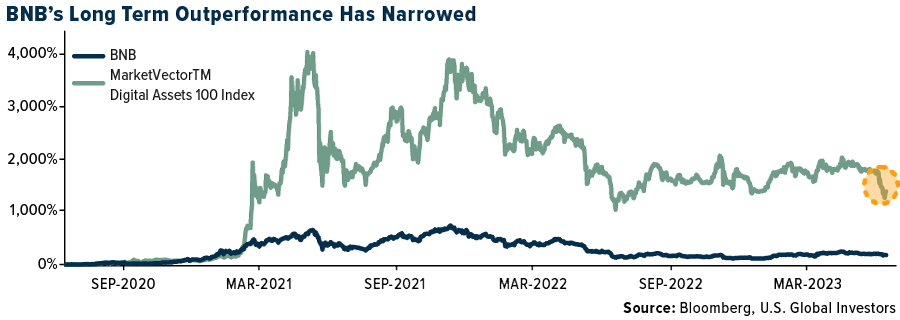

- The native token of Binance has snapped a slide that stoked nervousness among digital-asset investors. BNB has gained about 8.5% over the past two days, whereas an index of the largest 100 coins is little changed, (but that gap is starting to narrow), writes Bloomberg.

- Israel-based social-trading platform eToro says it won’t allow U.S. customers to open new positions in a number of crypto tokens, including Algorand, Decentraland, Dash, and Polygon effective July 12, writes Bloomberg.

Opportunities

- Santo Spirits, the tequila company co-founded by Grammy award-winning musician Sammy Hagar and famed television chef Guy Fieri, is the latest brand to jump into Web3 to create a customer loyalty program built around NFTs, writes Bloomberg.

- Hong Kong regulators are planning a second meeting in less than two months to push banks to offer services to virtual-asset firms as the city seeks to become an international crypto hub. The top financial regulators have called a meeting on Monday to bring together banks, crypto platforms, and other industry participants, writes Bloomberg.

- Coinbase’s retail traders may be turning to Robinhood, according to one analyst. Mizuho securities analyst Dan Dolev argues that data from April indicates the firm may be losing market share in retail crypto transaction volume to Robinhood, writes Bloomberg.

Threats

- Delio, a South Korean digital-asset platform, said it has suspended customer deposits and withdrawals, becoming the second site offering high yield to investors to do so this week, according to Bloomberg.

- Criminal hacker groups have a new favorite to bilk innocent companies out of cryptocurrency. So-called ransomware gangs are deploying fewer strains of ransomware in favor of data theft, but still demand payment, writes Bloomberg.

- Crypto trading platform Abra was accused of securities fraud by a Texas regulator that filed an emergency cease and desist order against the company and CEO Bill Barhydt. The Texas state securities board alleged that Abra misled investors through sales of its Abra Earn and Abra Boost crypto interest accounts, writes Bloomberg.

Gold Market

Gold futures closed the week at $1,971.50, down $5.70 per ounce, or 0.29%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.31%. The S&P/TSX Venture Index came in up 0.28%. The U.S. Trade-Weighted Dollar fell 1.24%.

Strengths

- The best performing precious metal for the week was palladium, up 8.91%, on little specific news and snapping a three-week losing streak. Gold strengthened with the weakening of the U.S. dollar and lower Treasury yields following comments from the European Central Bank (ECB) president about a likely interest-rate hike in July. The prospect of more rate hikes and positive economic data from the U.S. may temper gold’s performance, but the weakening dollar provides support.

- Positive drill results reported by Wesdome Gold Mines show the confirmation of the geometry and high grades of the 300 East Zone, indicating the potential for increased gold production. Additionally, the positive bias ascribed by National Bank of Canada further supports the investment potential, with visibility for resource accretion and high-grade production.

- Argonaut Gold’s successful gold pour marks a significant development milestone at its Magino mine in Ontario, and the company is now focused on completing commissioning and ramping up production. MAG Silver Corp.’s successful start of commercial production at its Juanicipio mine signifies a major milestone for the company and demonstrates its ability to generate revenue from the mine.

Weaknesses

- The worst performing precious metal for the week was platinum, down 2.53%, on little specific news. Gold and silver prices were declining to drifting lower with the upcoming Fed meeting at mid-week. The Fed paused on rates but signaled that potential future interest rate hikes were in the cards. Higher interest rates can negatively impact the demand for precious metals as they become relatively less attractive compared to interest-bearing assets.

- Johannesburg, Africa’s richest city, if faced with dysfunction in governance, rolling blackouts, and inadequate infrastructure maintenance, which contribute to a deteriorating quality of life and hinder economic development. The situation raises concerns about the city’s ability to attract investment and sustain its position as a major economic hub.

- The federal government cites Agnico Eagle Mines’ repeated failures to protect migrating caribou at the Meadowbank gold mine in Nunavut. The company needs to meet its obligations and implement caribou protection measures, or it risks potential penalties and reputational damage. This raises concerns about the company’s environmental stewardship and compliance with regulations.

Opportunities

- News broke that a takeover of First Quantum Minerals by Barrick Gold had been discussed by the two companies. Barrick’s interest in expanding in copper aligns with First Quantum’s significant copper assets. A successful acquisition would transform Barrick into a significant copper miner, a metal that is in high demand for its use in decarbonizing the global economy. This presents an opportunity for investors to capitalize on the potential growth and synergies resulting from the acquisition should the situation advance to further discussions.

- Royal Gold’s acquisition of royalty interests in the producing Serrote and Santa Rita mines in Brazil adds cash flow immediately to its portfolio. This acquisition provides Royal Gold with exposure to gold, platinum, palladium, copper, and nickel production from these mines. With the expected funding from available cash resources and a draw on its credit facility, Royal Gold can leverage the potential upside of these metals and diversify its royalty portfolio. This presents an opportunity for investors to gain exposure to multiple metals through a single investment.

- According to JPMorgan, the market is currently trending toward unprecedented territory for platinum in terms of load shedding and load curtailment in South Africa, with some producers warning that more severe power cuts could put between 5% and 15% of PGM supply in the country at risk. A one percentage point change in South African refined supply is equivalent to around 40,000 ounces of platinum and 22,000 ounces of palladium. Hence, even a relatively modest 3% contraction year-over-year in South African platinum supply this year would strip around 235,000 ounces from their balance and result in a global deficit approaching 900,000 ounces.

Threats

- The threat of the renewed rise in the value of Bitcoin has the potential to challenge the dominance of gold as a store of value. Bitcoin’s superior growth and increasing acceptance as an investment instrument have disrupted the traditional narrative that gold is a reliable haven asset. The emergence of Bitcoin as a viable alternative and hedge against uncertain market conditions could divert investor interest away from the yellow metal, posing a threat to its long-standing reputation and demand.

- The ongoing strike at Newmont’s Penasquito mine in Mexico, driven by a dispute over profit-sharing and alleged contract breaches, has the potential to disrupt production and affect Newmont’s earnings. The availability of funds to extend the strike and the support of associated members pose challenges to resolving the labor dispute, potentially prolonging the production suspension, and impacting Newmont’s financial performance.

- The surge in domestic gold prices in India is expected to lead to an increase in gold jewelry recycling. The record amount of used gold jewelry being sold for recycling could lead to reduced gold imports in India, putting downward pressure on international gold prices. The weakening rupee and the potential impact of a poor monsoon season further contribute to the increased selling of used gold, posing a threat to the demand and price of gold in the global market.

Related: Citigroup Says To Buy Copper Now Before the Rally to $15,000