Trending

At the moment, it’s understandably difficult to be enthusiastic about mid-cap stocks and the related funds. As of Aug. 8, the large-cap S&P 500 was beating the S&P MidCap 400 Index by a margin of better than 9-to-1 year-to-date.

Perhaps the best 2025 things that can be said of that mid-cap gauge are that it’s positive year-to-date and that puts it in better form than equivalent small-cap benchmarks, some of which are in the red since the start of the year. Still, it’s hard to convince large-cap-enthused clients and investors that the mid-cap juice is currently worth the squeeze.

For patient investors, there may be light at the end of the mid-cap tunnel because this segment of the equity market could, over time, prove responsive to President Trump’s “America First” agenda. That’s not an endorsement of a candidate, party or policy and the sentiment comes with the caveat that this administration’s economic and trade policies aren’t always smooth.

Still, mid-caps have the makings of a MAGA/America First, indicating the group could reward patient clients and investors seeking some diversification away from large- and mega-cap equities while not venturing outside the U.S.

Mid-Cap Sector Allocations Matter

Sector weights are among the reasons why broad mid-cap fund could be Trump plays. Take the case of the S&P MidCap 400’s roughly 24% allocation to industrial stocks, or more than double the weight to that sector found in the S&P 500.

“This sector weighting positions midcaps to benefit significantly from the anticipated infrastructure boom, as the US Congressional Budget Office noted in a report last year that infrastructure investment is expected to add up to US$800 billion to US$1 trillion in gross domestic product (GDP) growth by 2033, with significant contributions coming from transportation, energy and technology-related projects,” notes Dina Ting, head of global index portfolio management at Franklin Templeton.

Another sector-level advantage offered by many passive mid-cap funds is a notable overweight to financial services stocks relative to the S&P 500. That’s pertinent at a time when banks have the green light from the Federal Reserve to increase shareholder rewards.

Not to be overlooked is that while many basic mid-cap indexes and funds aren’t tech-heavy, the companies populating those funds are big-time artificial intelligence (AI) adopters. Due to their smaller size, mid-market corporations can be rapid deployers of AI, potentially giving them long-term legs up.

“According to a recent AI survey, generative AI adoption has surged to 91% among middle-market companies—up from 77% last year—indicating that AI capabilities have become standard operational tools that are expected to propel this segment of firms,” adds Ting.

Mid-Caps Are Inviting

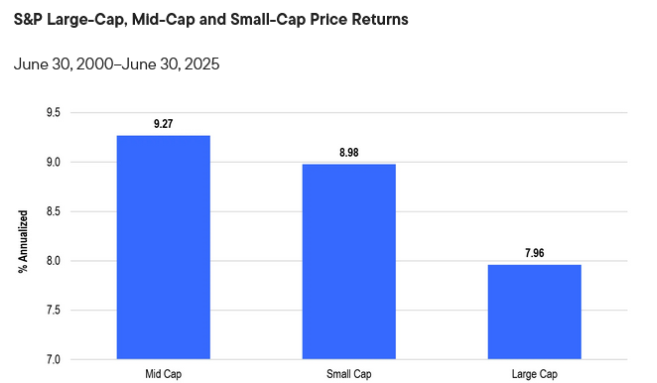

Beyond potentially favorable sector exposure, there are other reasons why mid-caps merit attention. Those include impressive long-term performance as highlighted in the Franklin Templeton chart below.

Mid-caps are also solid ideas for quelling concentration risk, which in this case references professional and retail investors’ favoritism of larger stocks is prompting them to gloss over mid-caps, possibly creating opportunity in the process. Perhaps best of all is the point that mid-caps aren’t demanding on valuation, confirming investors don’t have to pay-up to access this segment’s perks.

“Current market conditions have also created a notable valuation dispersion. Midcaps currently trade at nearly a 31% discount to large caps on a price-to-earnings (P/E) basis,” concludes Ting. “For investors with a longer-term horizon, we believe this valuation divergence may represent a compelling entry point into overlooked quality companies that have been overshadowed by the market’s focus on mega-cap names.”

Related: Here’s Why Cryptocurrency Has Plenty of Growth Ahead