Trending

Written by: Christopher Gannatti, CFA

Key Takeaways

-

NVIDIA’s 2026 GTC keynote signals a near-term inflection point as AI moves from generating content to executing real-world actions, powering autonomous vehicles, smart factories and robotics—creating immediate opportunities across the Physical AI ecosystem captured by the newly launched WisdomTree Physical AI, Humanoids, and Drones Fund (WDRN).

-

While macro uncertainty and high capital intensity remain headwinds for automation adoption, accelerating deployments in autonomous mobility, manufacturing and logistics suggest a durable shift toward embodied AI that could expand total addressable markets well beyond software.

-

With early leaders spanning drones, humanoid robotics and AI-enabled industrial systems, and portfolio exposure concentrated in these verticals, WDRN offers targeted access to sector-specific growth drivers as AI transitions from tokens to tangible economic output.

For the last few years, artificial intelligence has felt almost entirely digital. It writes emails, summarizes documents, generates images, helps code software and answers questions with increasing sophistication. But despite all that progress, it has largely remained confined to screens.

At NVIDIA’s 2026 GTC keynote, Jensen Huang introduced a shift that may prove more important than any incremental improvement in model performance. The conversation moved beyond chatbots, beyond reasoning systems, and into something more tangible: AI is beginning to act in the physical world.1 This could represent a transition into an entirely new phase.

If ChatGPT, released in late November 2022,2 was the moment AI became useful for generating information, 2026 may be remembered as the moment it became useful for generating physical action. We think that distinction matters more than it first appears.

From Thinking to Doing

The evolution of AI has followed a clear trajectory. First, models learned to perceive—recognizing images, transcribing speech and appearing to understand language. Then came generation, when AI could create entirely new content. More recently, reasoning models have enabled systems to break down problems, plan and refine outputs in a more structured way.

But the next phase could be fundamentally different. It’s not about what AI can understand or generate. Instead, it’s about what it can execute. Physical AI represents a shift from passive intelligence to active participation. These systems don’t just process inputs; they interact with environments, make decisions in context and translate those decisions into real-world outcomes.

This is the moment when AI stops being just a tool and starts becoming a collaborator, powering something that can operate alongside humans, not just respond to them.

The Bridge: From Tokens to Motions

At a technical level, the foundations of AI haven’t changed. Everything still runs on tokens. To step back, tokens are the basic units of data that models use to process and generate outputs. In some contexts, including the 2026 NVIDIA GTC keynote, tokens are referred to as ‘the units of intelligence.’ Over the past few years, entire business models have emerged around generating and monetizing these tokens.

What’s new is what those tokens represent. They are no longer just producing answers or content to be read on a screen, rather, they are producing decisions. Increasingly, those decisions are connected to systems that can act in the physical world.

The progression looks like this: Tokens become decisions, decisions become actions and actions translate into economic output. This can be viewed as the bridge between the digital and physical economies. Once AI can consistently move along that chain, its impact is no longer limited to software. It begins to reshape industries built on motion, coordination and execution. In a sense, we could be watching the next evolution that takes us beyond one of AI’s biggest initial use cases, the generation of software code.3

The First Real-World Deployments

At NVIDIA’s 2026 GTC keynote, this shift was on full display through its NVIDIA DRIVE platform, powered by the new AlpaMayo autonomous driving model, the company’s latest step toward reasoning-based vehicle intelligence. These systems don’t just navigate—they explain their decisions, articulating why they changed lanes, how they responded to obstacles and what they anticipate next. This is a meaningful step beyond automation—it is the emergence of systems that can reason in the physical world, not just react.

Importantly, this technology is not confined to the stage. NVIDIA’s DRIVE platform already underpins development programs across a wide range of global automakers, and its next-generation capabilities are being integrated into vehicles that are beginning to reach public roads. In the near term, most people are unlikely to “buy” an NVIDIA-powered autonomous vehicle outright, but they are increasingly likely to ride in one.

In cities like Phoenix, San Francisco and Los Angeles, fully autonomous vehicles from companies like Waymo are already operating without human drivers. Uber is actively partnering with autonomous vehicle developers to bring these fleets onto its network, meaning a rider could request a trip and be matched with a driverless car.4 Amazon’s Zoox is preparing purpose-built autonomous vehicles designed specifically for urban environments,5 while traditional automakers—from Mercedes to Hyundai and BYD—are working with NVIDIA to bring advanced driver-assistance and, eventually, fully autonomous capabilities into consumer vehicles.

Tesla, pursuing a different technological path, is simultaneously deploying increasingly capable AI-driven driving systems across millions of vehicles already on the road, using real-world data to continuously improve performance.6 While the architectures differ, the direction is the same: AI systems are moving from assisting drivers to gradually replacing them.

Factories Become Intelligent Systems

If autonomous vehicles are the most visible example of physical AI, manufacturing may ultimately be the most important. Global manufacturing represents tens of trillions of dollars in economic activity, yet much of it still operates on relatively rigid forms of automation—machines programmed to repeat the same task.

That model is already beginning to change.

At Hyundai’s new “Metaplant” in Georgia, the future of manufacturing is taking shape in real time. Hundreds of robots weld, assemble and move components across the factory floor, while fleets of automated guided vehicles coordinate the flow of materials between stations. The system is designed to scale to hundreds of thousands of vehicles per year—not through incremental labor increases but through tightly orchestrated machine coordination.7

What stands out is not just the level of automation, but the structure of the system itself. This is not a factory augmented by technology. It is a factory increasingly defined by it.

Beyond the Factory Floor

The implications of physical AI extend well beyond manufacturing and automotive applications. Drones are already transforming industries from logistics to infrastructure inspection—but increasingly, they are becoming visible in everyday experiences as well.

At the 2026 Winter Olympics, for example, fleets of high-speed drones raced alongside athletes in real time, capturing footage that traditional cameras simply couldn’t. These systems weren’t just flying cameras, rather, they were operating in complex, dynamic environments, tracking motion, adapting to terrain and maintaining stability at high speeds.

What makes this notable is not the novelty of the footage, but what it represents. The same underlying capabilities, things such as real-time perception, decision-making and coordination in physical space, are the building blocks of much larger systems.

The Next Chapter

If ChatGPT marked the moment when AI became capable of thinking, this may mark the moment it begins to work. And when AI starts working in the real world, doing things such as driving vehicles, managing factories and coordinating infrastructure, the investment landscape changes accordingly.

The opportunity is no longer confined to software companies or cloud platforms. It extends across the systems and industries that connect intelligence to physical outcomes. That makes the story both broader and more complex.

Which leads to the natural question: how do you invest in a transformation that spans so many sectors, technologies and timelines?

Introducing the WisdomTree Physical AI, Humanoids, and Drones Fund (WDRN)

The WisdomTree Physical AI, Humanoids, and Drones Fund (WDRN) provides investors with targeted exposure to this transformation by capturing companies across the Physical AI ecosystem, from enabling technologies to real-world deployment platforms. The ETF is designed to track, before fees and expenses, the total return performance of the WisdomTree Physical AI, Humanoids, and Drones Index.

Physical AI manifests across several key verticals. These verticals are central to how different company activities are incorporated into the strategy:

-

Humanoid robotics – Companies developing humanoid or exoskeleton robots that replicate human movement, interaction, or assistive functions. Includes designers of bipedal robots, service robots, and robotic components such as actuators, sensors, and embodied-AI systems enabling human-like capabilities.

-

Drones and autonomous systems – Autonomous mobility companies involved in unmanned and autonomous vehicles operating in air, land, or sea. Includes producers of drones, eVTOL aircraft, autonomous driving systems, and supporting hardware and software for self-navigating mobility.

-

Next-Gen Factories (Smart Manufacturing) – Companies advancing industrial automation and robotics within manufacturing. Covers providers of cobots, machine vision, control systems, and digital-factory software enabling autonomous, connected, and data-driven production environments.

-

Next-Gen Logistics & Supply Chain Robotics – Companies providing robotic and automation solutions that streamline warehousing and distribution, including automated storage systems, mobile and guided robots, and AI-driven logistics software.

-

Emerging Applications of Robotics - Companies applying robotics and AI to new or specialized sectors such as healthcare, agriculture, construction, and defense. Includes manufacturers of medical, rehabilitation, inspection, and field-service robots expanding robotics beyond factory and logistics use.

These categories collectively represent the transition from software-based intelligence to embodied intelligence.

In Figure 1, we see one result of this process, looking at the top 20 company exposures for the WisdomTree Physical AI, Humanoids, and Drones Index. We think that many investors will see some highly recognizable global companies, like Nvidia and Tesla. Similarly, they will also see an emphasis on drones and autonomous mobility, which may lead to learning about important physical AI companies that are not as globally familiar.

Figure 1: Top 20 Company Positions

Source: WisdomTree, Bloomberg. Weights as of 28 February 2026. Holdings are subject to change. Click here for current holdings. You cannot invest directly in an index. Past performance is not indicative of future results.

In Figure 2, we see the current positioning of the strategy across the five aforementioned verticals. The clear emphasis at present is on Humanoid Robotics and Drones / Autonomous Mobility. As the space evolves over time, the strategy is designed to flexibly evolve and other categories may gain greater exposure.

Figure 2: Exposure to the Five ‘Physical AI Verticals’

Source: WisdomTree, as of 28 February 2026. You cannot invest directly in an index. Past performance is not indicative of future results.

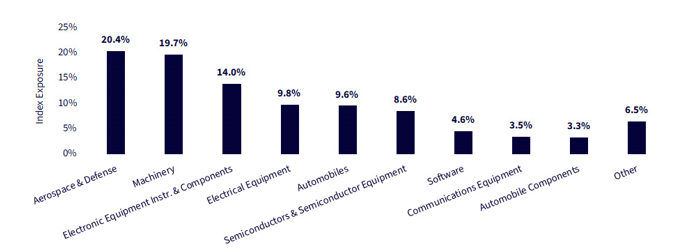

Finally, for those looking to ground a sense of the strategy’s exposure against a known equity categorization hierarchy, Figure 3 shows exposures across different Global Industry Classification Standard (GICS) Industry Groups. This helps investors go back and forth from Figure 2 to Figure 3 and gain a greater sense of the balance between diversification across specific company activities as well as concentration within the verticals that WisdomTree believes define the Physical AI theme.

Figure 3: Exposures Across the GICS Industry Groups

Source: WisdomTree, Bloomberg as of 28 February 2026. Exposures shown across different GICS Industry Groups to showcase breadth. You cannot invest directly in an index. Past performance is not indicative of future results.

It is exciting to introduce the physical AI theme into the U.S. ETF market, and it’s notable to look towards the next evolution of such themes as ‘robotics’ and ‘factory automation’ that have certainly come up before, but that are now undertaking their business activities and innovations in new ways, taking advantage of generative AI as well as AI agents and what those may bring to the physical world.

-

Source for the narrative arc of this piece, unless otherwise noted: Huang, J. (2026, March 16). Keynote by NVIDIA CEO Jensen Huang at GTC 2026 [Conference presentation]. NVIDIA GPU Technology Conference (GTC), San Jose, CA, United States.

-

Source: OpenAI. (2022, November 30). Introducing ChatGPT.

-

Source: Business Insider. (2026, March). AI coding is changing the role of software developers.

-

Source: Uber Technologies, Inc. (2026). Uber unveils Uber Autonomous Solutions to accelerate autonomous mobility & delivery worldwide.

-

Source: Car Design News. (2025). How autonomy reshapes vehicle design: The Zoox robotaxi.

-

Source: Tesla, Inc. (2024). Full Self-Driving (FSD) capability.

-

Source: Ulrich, L. (2025, November 5). The Hyundai Metaplant: A new era in EV manufacturing. IEEE Spectrum

See the WisdomTree Glossary for definitions of terms and indexes.

Related: Rising Through Discipline: Why DGRW and DDWM Are Earning Their Upgrades

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Companies engaged in Physical AI Activities are subject to unique regulatory, operational and technological risks, such as intense competition and potentially rapid product obsolescence. The regulation of such companies in the United States and other countries is diverse and rapidly evolving, which may inhibit or delay adoption. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Companies engaged in Physical AI Activities typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Humanoid robotics companies are sensitive to trends in industrial production, capital-expenditure cycles, supply-chain conditions, and adoption rates of automation technologies across varied sectors including business and industrial end-users.

Humanoid robotics companies may have long and capital-intensive development timelines, highly uncertain paths to profitability and large-scale deployment, and limited product lines, markets, financial resources or personnel. Drone companies may be dependent on the U.S. Government and its agencies for a significant portion of their revenues, and the commercial and military adoption of drone technologies remains subject to extensive and evolving governmental oversight, including aviation safety standards, airworthiness certification requirements, export controls, and national security reviews. A fund that has a portfolio that is concentrated in the securities of issuers in a particular industry or group of related industries, may be adversely affected by the performance of those securities, and more susceptible to adverse economic, market, political, or regulatory occurrences affecting that industry or group of related industries.

Investments in non-U.S. securities involve political, regulatory, and economic risks that may not be present in U.S. securities. For example, foreign securities may be subject to risk of loss due to foreign currency fluctuations, political or economic instability, or geographic events that adversely impact issuers of foreign securities. Investments in securities and instruments traded in developing or emerging markets, or that provide exposure to such securities or markets, can involve additional risks relating to political, economic, or regulatory conditions not associated with investments in U.S. securities and instruments or investments in more developed international markets.

The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Past performance is not indicative of future results.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S.

This WisdomTree article is provided as part of a paid sponsorship.