Trending

Registered investment advisors (RIAs) and experienced fixed income investors are aware of callable bonds, or debt instruments that often feature higher interest rates because borrowers have the flexibility to pay off those liabilities early.

Building upon that concept, there are callable yield notes. Although many market participants aren’t familiar with that asset class, it represents 70% of all structured notes in the mammoth $200 billion domestic fixed income derivatives. If that sounds like the territory of professional market participants, that’s because it was. “Was” being the operative word because callable yield notes are now broadly available to advisors and income-hungry retail investors thanks to the Calamos Autocallable Income ETF (CAIE).

The first ETF of its kind, the Calamost autocallable ETF debuted last June and is an undisputed success as highlighted by its nearly $641 million in assets under management as of Jan. 28. That’s impressive work for any new ETF, let alone one addressing an asset class with which many investors aren’t familiar.

CAIE’s fast start also stands as proof positive of some other factors. Namely, advisors want to source income for clients and they want to accomplish that objective without relying entirely on bonds and dividend stocks. The Calamos ETF checks that box and does so to the tune of a distribution rate of 14.36%.

Understanding CAIE Plumbing

Clearly, CAIE delivers the income goods, but advisors should still take the time to understand the ETF’s inner workings.

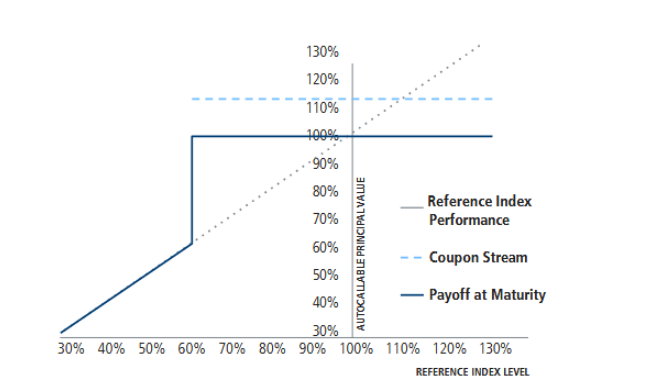

“An autocallable is a market-linked instrument that pays regular coupons and returns principal at maturity (or if called early), as long as a reference index, like the S&P 500, doesn’t fall below specific thresholds (e.g., -40%)—think of it like a bond whose income and principal depend on the stock market not falling too far,” according to Calamos.

The chart below paints a picture of how autocallables work.

(Image: Calamos Investments)

So what’s happening and what can advisors expect with CAIE? In essence, end users are engaging in a trade-off. They’re embracing CAIE’s potential for higher monthly income for slightly higher risk in the form of a deep bear market possibly interrupting the coupon payments delivered by some or all of the autocallables held by the fund.

Yes, it can be said that CAIE, as is the case nearly every other ETF on the market, is a reminder that there are no free lunches in investing, but bear markets aren’t frequent and with the autocallables featured in this ETF, counterparty risk is benign, broadly speaking.

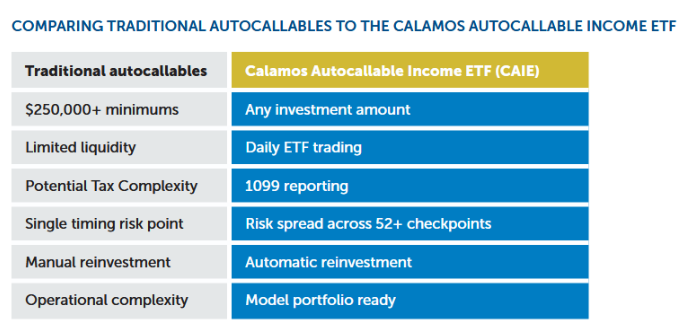

CAIE Democratizing Autocallable Investing

As noted earlier, CAIE is rapidly gaining traction because it’s bringing a formerly opaque asset class into the limelight while increasing access to it. That’s commendable for any new ETF, but few accomplish those aims and the point about democratizing autocallable access is not to be diminished.

(Image: Calamos Investments)

Plus, advisors considering CAIE get the transparency they’ve come to love with other ETFs – another positive point that shouldn’t be overlooked.

“Through the Calamos Autocallable Dashboard, investors can see exactly how many autocallables CAIE is exposed to and where they stand relative to coupon payments, market value, premium/discount to par, and expiration. This provides real-time visibility into the portfolio's performance,” according to the issuer.

Those aren’t the end of CAIE’s advantages. The ETF functions as a complement or alternative to traditional equity income exposures while acting as a yield diversifier in portfolios that may be too bond-dependent. All that with the potential for some tax efficiencies relative to bonds and other structured note products.