Written by: Kunal Shah | iCapital Network

Private equity looks attractive today given the current discount to public markets and strong historical performance of recession-year vintages

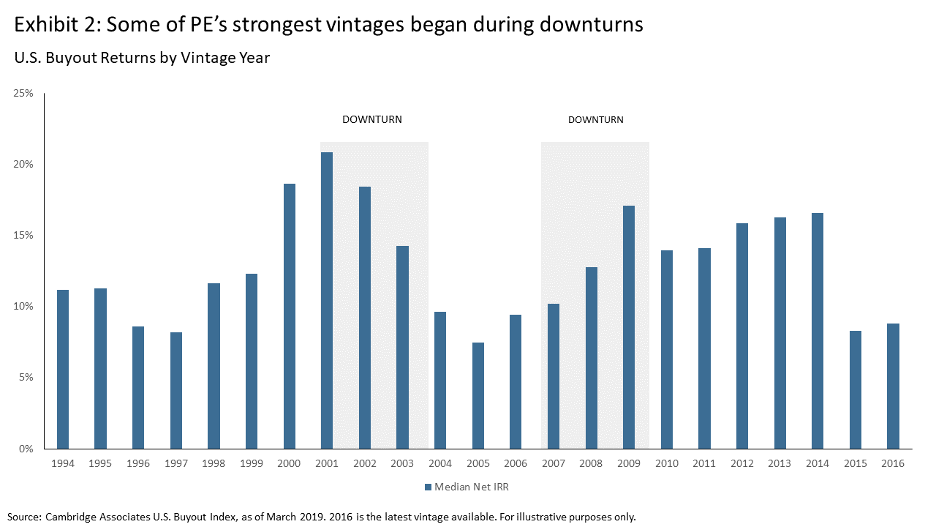

As public company valuations have continued to rise amid a pandemic-driven recession, private market valuations have trended downward. The current disparity between private and public markets, along with the strong historical performance of recession-year private equity vintages (Exhibit 2), may make this an ideal time to put capital to work in the private markets.

Since the pandemic-induced selloff in March, public equity indices have rebounded to all-time highs, continuing the longest bull run in history. While this has certainly been a short-term boon for equity investors, questions remain about the sustainability of current valuations, especially in light of the apparent disconnect between stock prices and underlying economic fundamentals.

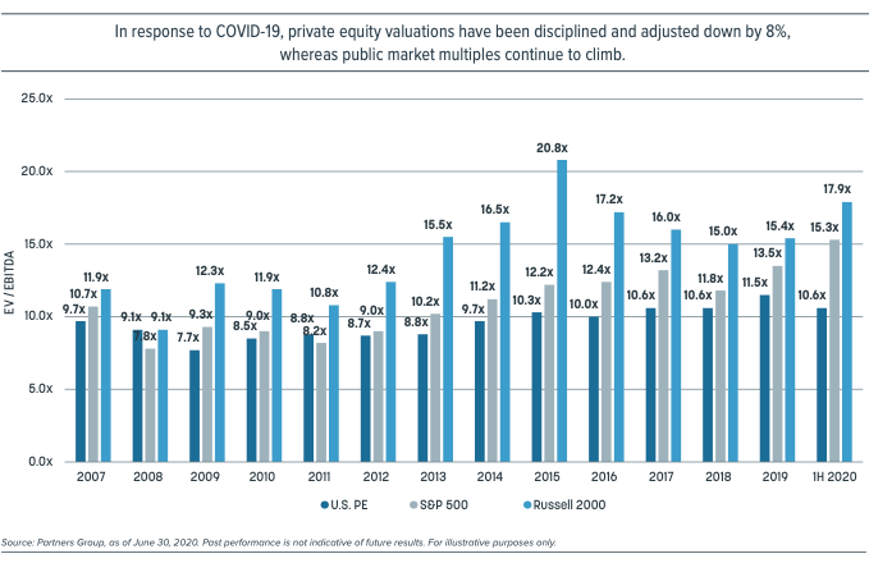

In the meantime, private market valuations—which often have as much as a 75% correlation with the movements of public markets—have told a different story over this period. As the pandemic unfolded during the first and second quarters, private equity managers were able to buy companies at an 8% discount compared with 2019. As of June 30, PE valuations represented significant discounts to the public markets.

Factors Driving Public Market Valuations

To understand why private markets may be an attractive alternative to public equities, it helps to first understand why public equity valuations are currently so high. The major contributing factor is ultra-accommodative monetary policies pushed forward by central banks since the start of the pandemic. The balance sheet of the Federal Reserve has ballooned to over $7 trillion, more than three times its size during the peak of the Great Financial Crisis, and other central banks have followed a similar trajectory. In addition, fiscal stimulus programs—including over $2 trillion in the U.S. to date—have reached unprecedented levels.

The dramatic increase in money supply, as well as the boost from fiscal stimulus programs, has created an environment that has allowed stock prices to climb higher absent the typical positive economic indicators that accompany a stock rally. As such, public markets appear to be ignoring current economic and earnings weakness. In place of fundamental analysis, public investors appear to be pricing in considerable optimism for future corporate earnings.

Another factor fueling this positive investor sentiment may be an increase in retail investors in the stock market today. A number of retail brokerage firms have recently started to allow fractional investments in stocks, while commission-free platforms like Robinhood have allowed for an influx of individuals to invest in the stock market, often without sufficient consideration for business fundamentals. Research[1] suggests that the stay-at-home orders during the coronavirus outbreak led to a significant increase in trading activity among individual investors, particularly younger people.[2] This additional activity may be nudging share prices higher.

Private Equity Valuations Are Rooted in Fundamental Analysis

Certain key dynamics in play in public equity markets today are not evident in the private markets. While public markets offer real-time pricing that can be fueled by sentiment, for example, experienced private equity managers make investments only after completing a rigorous fundamental analysis to determine a company’s value. The general uncertainty facing many companies today is factored into the purchase price and the structure of the privately negotiated transaction.

During periods of dislocation, we typically see a “flight to quality” by investors. This is true in private markets; relative to more benign environments, experienced private equity managers today are arguably choosing to invest in higher-quality, more resilient businesses able to withstand a recession. Thus, the reduction in purchase price multiples in the 1H 2020 is quite remarkable.

Because private equity managers report on the valuations of their portfolio companies infrequently (once a quarter), it can be challenging to take the pulse of the private markets intra-quarter and there is considerable uncertainty about whether private markets will rebound in the second half of the year. To be certain, the disconnect between public equity valuations and underlying fundamentals is unlikely to persist over the long term.

In our view, private equity’s lower valuations, coupled with its growth outlook, present an opportunity for the asset class to potentially deliver strong performance relative to public equity markets. We’ve written in the past about the strong historical performance of private equity during recessions. A recent report from UBS supports this perspective, noting that private funds that form in “crisis years” historically outperform. The report looked at funds from 1994-2017 and found that reported internal rates of return (IRR) averaged 18.6% during crisis periods compared to a return of 9.7% for the MSCI All Country World Index.[3]

Moreover, PE has generated 490 basis points of outperformance above the S&P 500 Index over the last 20 years. In our opinion, the more recent disconnect between stock prices and fundamentals will not persist. In fact, anecdotal feedback from private market fund managers suggests that valuations for many private companies are gradually shifting back up closer to pre-COVID levels, which, as noted above, are still generally well below public market valuations. As advisors prepare for more uncertainly in the public markets and adjust their expectations, we believe this may be an ideal time to consider entering the private markets.

Related: Driving Performance via Sector Specialists

[1] Ortmann, Regina; Pelster, Matthias; Wengerek, Sascha Tobias; “COVID-19 and Investor Behavior”