Trending

Written by: EquityMultiple

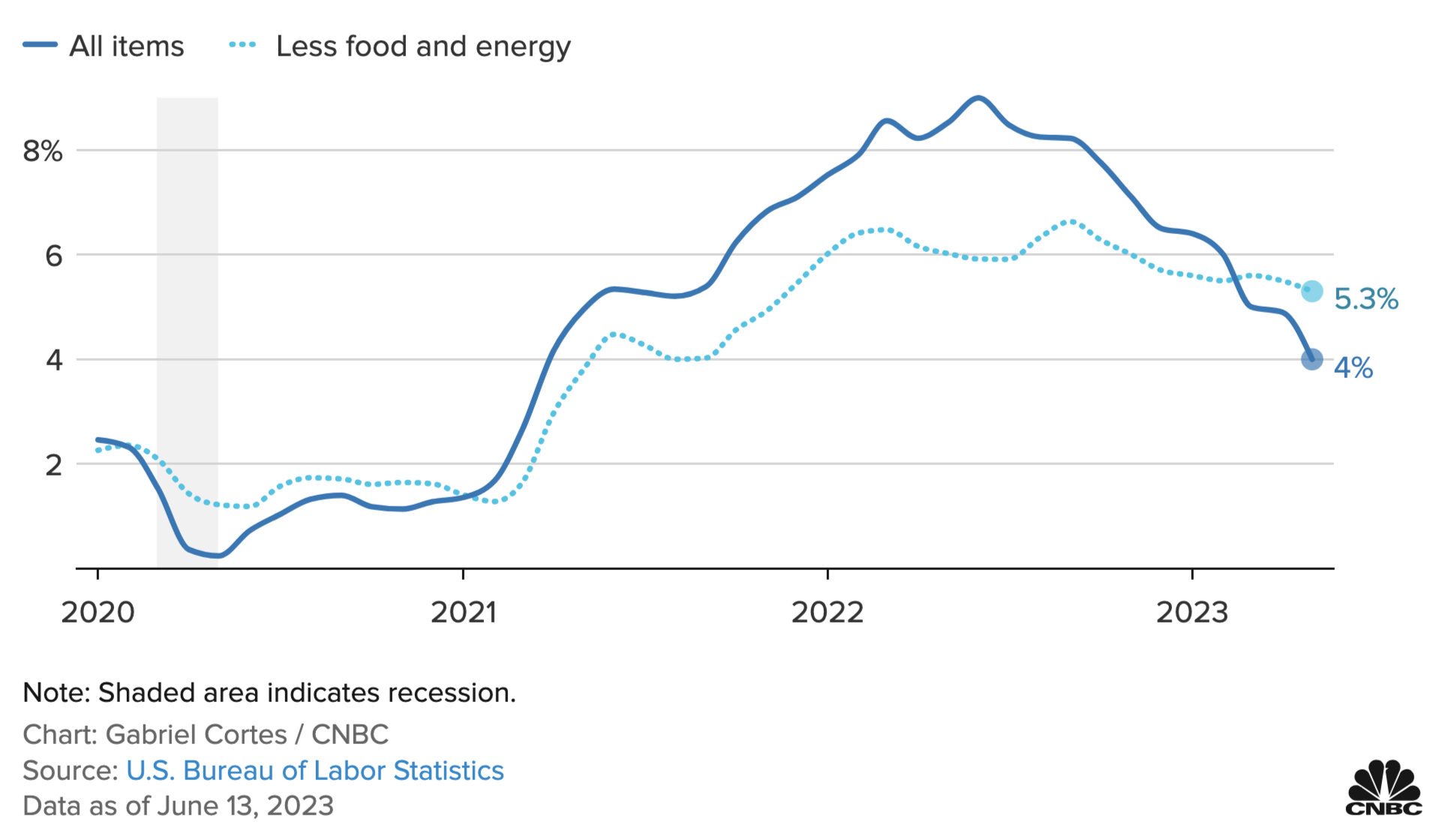

The latest inflation report from the Department of Labor showed that CPI rose only 4% from a year ago, about half the rise from when inflation peaked. This is a positive sign that inflation is starting to trend down and begin to taper back to the Fed’s 2% target. The Fed announced at their latest meeting that they would pause rate hikes for now.

U.S. Consumer Price Index: Year-over-year percent change through May 2023

Commercial real estate is affected by inflation and rate hikes in many ways. On one hand, CRE often serves as an inflation hedge such that rents tend to keep pace with inflation and property values rise with rents. On the other hand, higher interest rates tend to correspond with higher cap rates and borrowing costs, which can affect property values and cash flow, respectively. As monetary policy moderates, we can expect to see more liquidity in the real estate capital markets, which presents opportunities for investors.

EquityMultiple sees attractive risk-adjusted returns in both multifamily preferred equity and distressed acquisitions.

Here are five market trends to monitor this week in the context of your real estate portfolio:

1. More volatility?

Are public equities headed for halcyon days again? Not necessarily. The S&P 500’s gains this year are top-heavy, and could be more sentiment-driven than usual. To boot, the spread between the S&P 500’s earnings yield and “risk-free” yield is narrowing. With bond yields potentially being forced down as well, you may be well advised to look upon the traditional 60/40 portfolio construct with ongoing skepticism. Alternatives like (like private-market real estate) can offer a timely diversification driver.

2. All Eyes on Real Estate Debt

CBRE’s chief economist predicts more pain in the regional banking sector, predicting that 311 of 4,800 banks will go bust, while still painting a “rosy picture” for CRE. This confluence of factors, broadly, is why we’re bullish on real estate debt. As CenterSquare puts it: “Due to market inefficiencies, we believe that core-plus [real estate] debt is a mispriced asset class that has the potential to outperform core equity and broader fixed income returns, with lower risk.” The firm’s analysis concludes that real estate debt has the potential to outperform equity.

3. Productivity Boom?

After the GFC, we had a “jobless recovery.” Pessimistic economists (is there any other kind?) now worry that we may see the opposite: a “job-full recession,” owing to stagnating labor productivity. Generative AI has real potential to rapidly turn the tides, spur labor productivity growth, and reverse (or even stave off) a true recession. Even the enthusiasm for AI could potentially be a near-term boon for real estate markets, even beleaguered gateway metro office markets. The irreplaceable buzz of big city innovation, and agglomerative economies of scale, could help hasten the recovery of occupancy rates and valuations.

4. Don’t Chase the Hype

With the S&P 500 on the starting line of the next bull run, it is worth looking at what expectations propelled the last one. In recent weeks, the SEC has taken aim at crypto-asset exchanges alleging that the firms were operating unregistered exchanges. Crypto is exciting, but each hype cycle often follows a similar trend. A new AI summer begins with promising advances and technology stocks are rising to nauseating highs again. New tech is propelled by optimism and, each time, the reality tends to be much more tame. Investors are left with the bag. Tangible assets like real estate exist in the real world. Regardless of what the new hot tech is or the new enterprises we develop, we all need a place to live and conduct business.

5. When One Door Closes…

With large office real estate developers and managers suffering a downturn, investors are pausing to assess what is happening in the market. Several office markets are seeing large drops in value. The new normal of hybrid work has been resilient to corporate pressures and employees continue to cement into lower cost, suburban areas. What happens to be a loss of value in commercial office looks to be supporting a boom in suburban retail and new construction in the Sun Belt. Although prudence is required to not fall into a new hype cycle in these markets, it appears that the secular trend kickstarted by the Covid-19 pandemic continues. Workforce housing could be an interesting investment here and with the current hot market, investments higher in the capital stack (like preferred equity) can provide a higher priority return.

Related: Cracking the Inflation Code