Trending

2021 HSA Contribution Limits

The IRS just announced that health savings account (HSA) contribution limits will increase in 2020, giving you and your employees the chance to save more than ever.

As a response to rising inflation, the contribution limits into savings vehicles like IRAs, 401(k)s, and HSAs can rise from year to year.

A quick HSA refresher

An HSA is a tax-advantaged account paired with an HSA-qualified health insurance policy. HSAs allow your employees to save tax-free money for qualified medical expenses. When used for qualified medical expenses, there is no tax on your HSA funds, and the funds in the account are exempt from capital gains and other investment related taxes. These savings create a triple-tax advantage for participants. Increased limits can help your employees accelerate the process of saving and investing.

To qualify for an HSA and the triple-tax savings, your employees need an HSA-qualified policy, which is a plan with a higher deductible. In order to qualify for 2020, the employee must have a health insurance policy with a deductible of at least $1,400 per year for individual coverage, and $2,800 per year for a family plan.

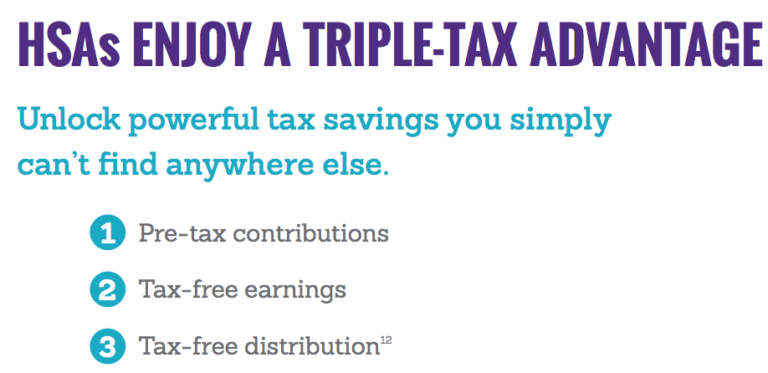

Your health savings account (HSA) packs more punch than ever.

Tax-free contributions apply to federal income taxes as well as FICA payroll taxes. When members make tax-free HSA contributions, they save on average 30% of their income. Importantly, 401(k) contributions are still subject to FICA taxes. FICA taxes are approximately 7.65% on each dollar, so contributions to an HSA go further than contributions to a 401(k).

In addition, HSA earnings (whether from interest or investments) are not taxed either. Members can contribute to their HSA up to the age of 65, after which time Medicare disallows HSA contributions because it’s not considered a high-deductible health plan.

Because of this triple-tax advantage, HSAs deliver maximum exibility in retirement. HSA members age 65 and older can use their HSA for any expense, not just qualified medical expenses. But if the money is not used for qualified medical expenses, then it’s taxed as ordinary income—just like a 401(k). However, unlike a 401(k), an HSA is not subject to minimum required distributions. And HSA distributions are never taxed if the money is used for qualified medical expenses.

The IRS announced higher HSA limits for the 2021 tax year, which means opportunity to save even more.

2021 maximum HSA contributions

$3,600 Individual

$7,200 Family

$1,000 Catch-up contributions (55 and older)

Before you look too far ahead, it’s a good idea to make sure you’ve maximized your 2019 contributions. Because of COVID-19, the IRS extended the tax filing deadline to July 15, 2020. HSA members with individual coverage can contribute up to $3,500, those with family coverage can contribute up to $7,000 and those 55 and older can contribute an extra $1,000.

Take a moment to confirm that you’re on pace for your 2020 targets, too. Given social distancing, most of us are spending a little less than usual. Consider moving that savings into your HSA. The more you contribute, the faster you can accelerate long-term health savings.

The IRS also announced 2021 HSA-qualified health plan limits.

2021 high-deductible health plan limits

Maximum out-of-pocket expenses

$7,000 Individual

$14,000 Family

Minimum deductible

$1,400 Individual

$2,800 Family

Conclusion

HSA contribution limits are a great reason for your employees who don’t currently have an HSA-qualified health plan to get started. Some of the greatest advantages of HSAs include being able to use funds to pay for qualified medical expenses, and rolling over any unused balance to next year or even all the way to retirement and beyond.

If you would like more information regarding HSAs for yourself or your company please contact us at [email protected]

Until Next Time…

Related: How to Understand Cash Balance Plans Without Being an Expert