Trending

Financial advisors get fired a lot, often at critical moments: 70% of families switch advisors when a spouse becomes disabled, and another 70% change when money passes to the next generation.

These are exactly when families most need guidance. So why fire advisors they've trusted for years?

It comes down to a fundamental disconnect.

The three-circle reality

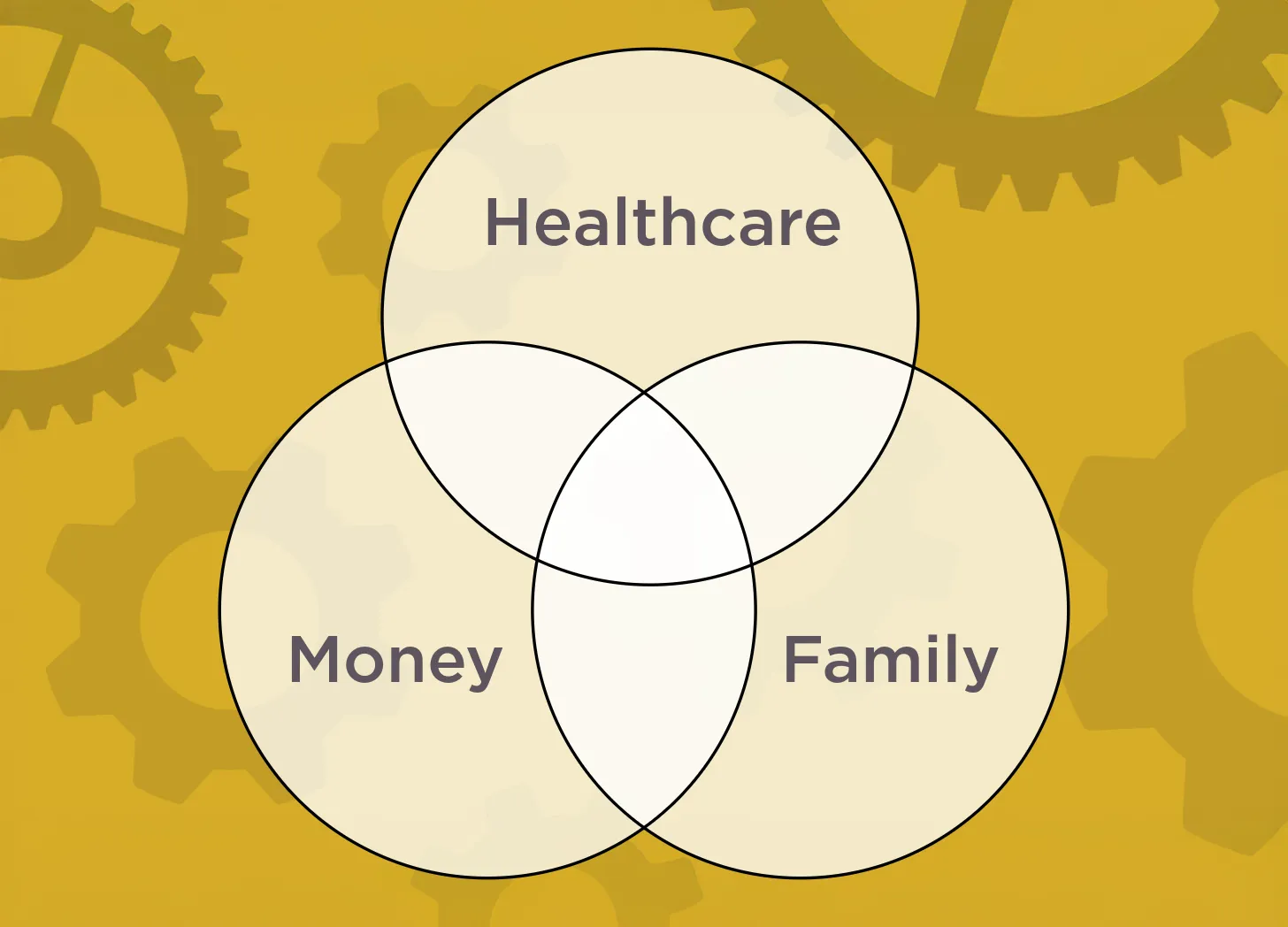

We can imagine the key elements of life decisions—Healthcare, Money, and Family Goals—as overlapping circles.

Most financial professionals are great when any two overlap. They excel at traditional retirement planning (Money + Family Goals) and can handle basic healthcare costs (Money + Healthcare). But they struggle when all three circles intersect—which is exactly where your biggest life decisions happen.

I learned this lesson with a client I'll call Mary. She had substantial savings and a husband with Alzheimer's. While she was figuring out how to keep him safe and whether they could stay in their home, I was busy creating sophisticated financial projections and tax strategies.

When I presented my detailed plan, Mary listened politely and said,

"Tom, I trust you with our money because I can see you believe in your plan. But I can't focus on any of that right now. My goal this morning was just remembering to eat lunch."

That's when I realized we were living in different worlds.

She was thinking about dignity, safety, and staying together. I was talking about portfolio optimization.

Reality check: how to prepare

Healthcare crises don't wait for your financial plan. Real decisions happen in hospital waiting rooms and around kitchen tables. By the time you call your financial advisor, you've already committed to moving Dad to memory care or keeping Mom at home with round-the-clock help.

So what can you do about this reality?

First, understand that healthcare priorities will hijack your financial priorities—whether you plan for it or not. The question isn't if, it's when.

Second, the best financial decisions happen when someone understands both the healthcare landscape and the financial implications. These worlds rarely talk to each other, but your family needs someone who speaks both languages.

Third, timing matters enormously. Having financial conversations after you've already decided to move Mom to assisted living is like buying insurance after the accident.

Questions to ask before you’re in crisis mode

Before you’re in a place where remembering to eat lunch is all you can focus on, ask your financial advisor:

-

Have you helped other families navigate healthcare transitions?

-

Do you understand how different types of senior care work and what they cost?

-

Can you model scenarios based on different care needs, not just market conditions?

-

Will you help us have difficult family conversations about future care?

If your advisor seems uncomfortable with these questions, that's valuable information. Most of us will need someone who can guide us through those overlapping circles of health, family, and money—not just manage your portfolio.

The families who navigate aging successfully don't necessarily have more money. They have better guidance at the moments when everything intersects.

Related: I Can’t Thrive at 55?