Trending

How one client illustrated the giant gap in managing long-term care—and changed my life in the process

Prologue

I have been in the business of long-term care financial planning for more than 30 years, which makes me old-ish. I can tell that I’m old-ish because I increasingly reminisce about things. For instance, the Knicks in the NBA Finals take me back to when they were in the Finals in 1994, playing the Houston Rockets, and having that Game Six interrupted by the O.J. Bronco chase—which was also the night of my bachelor party.

I also have been reminiscing about how I became involved in long-term care financial planning. My wife of 30+ years would cringe at any blustery framing of my “origin” story, but I want to share my path because the crises that pulled me into my profession remain a persistent source of pain and stress for many families. It’s become my life’s work to help those families navigate the challenges of health, financial planning, and the stress that comes with every long-term care situation. I hope by sharing this story, it illustrates what many families are up against and what they can do to mitigate the problems.

There are three key people in this story, and please indulge a bit of artistic liberty to write about it from their points of view instead of my first person. This is a fictional reconstruction based on real conversations and events.

JOHN

Tom’s long-term care manager at John Hancock Financial Services

Tom was 25 when he started working for John Hancock Financial Services. He was newly married, and I knew he had just moved in with his in-laws—which meant he needed this job badly. Hancock is always looking for motivated and disciplined new agents with a high pain threshold. Cold calling about long-term life insurance is rough, but not as rough as running out of money and living in your in-laws’ basement.

Tom West ‘95. I have no idea what I’m doing

It’s not a fun job. It’s a pay-your-dues job so you move on to the next position. But Tom started to get some engagement with the people he called, and he came to me with a question: What can we do for a couple where one healthy spouse is the caregiver for a sick spouse who needs long-term care?

Our boiler-room called these “one-legger” appointments. Tom for some reason was great with these, but the solution wasn’t exactly what the prospects were hoping for. Because at that time, our answer was for the healthy spouse to buy long-term care insurance for themselves. There is no insurance for someone with a diagnosed long-term care illness. And buy enough that the payout would care for the healthy spouse, because other resources were being gobbled up by the cost of care.

Tom did that—because it is good financial advice for the next long-term care problem for a one-legger couple. But Tom wasn’t happy leaving living rooms without solving the current problem, and he complained about not being able to help these households. Same broken record. Families asking: What are we supposed to do? But you can’t insure the uninsurable, and nobody wants these families as investment clients Rolling Crises x High Difficulty x Timehole = Not Profitable.

I told him to go look up the Alzheimer’s Association if he wanted more resources to help.

BETSY

Program director at the Alzheimer’s Association

I got an unsolicited request from this long-term care insurance guy named Tom who wanted to “learn more.” He was young and had that eagerness and sales-y confidence of shiny new financial guys.

Little did I know that over the next few years, Tom would become a huge resource for our support groups and even introduce me to his mom, who would later volunteer with us and become a friend. This day, however, was not the start of a great friendship. I was annoyed because I thought the last thing we needed at the Association was a guy hovering around families in a real struggle with cognitive challenges trying to sell people long-term care insurance.

“You want to help?” I told him. “You need to understand what these families are going through. Why don’t you co-host a social working group for families that we have at a local church. You’ll be able to interact with them and understand what they are experiencing. The next one is on ‘Grief During the Holidays.’

That’ll get rid of him, I figured, throwing him right in the deep end when he had no experience with Alzheimer’s. That was one of the roughest tests for even our most experienced social workers, an emotional cyclone of denial and acceptance, fear and love, and the true tests of friend and family bonds.

And wouldn’t you know? He came back. Shook, for sure. He joked with me later that the meeting gave him PTSD—as it should have. He saw firsthand what the families were experiencing as they tried to balance the health care of their loved one, find the finances they needed to pay for I-had-no-idea-how-very expensive care, and provide a quality of life for themselves and their loved ones.

To his credit, he came back, spearheaded a revamp of all of our programming about financing dementia costs, built our planned giving operation from scratch, and served on our board for the better part of a decade.

When I referred him to an overwhelmed caregiver named Mary and her husband, I had a feeling they would be in good hands.

MARY

Federal Government retiree and caregiver for her husband

I was skeptical when Betsy from the Alzheimer’s Association referred Tom, but at the time I couldn’t even open the mail and focus on all of the money things that seemed to be screaming for attention. I guess I was also desperate for help. I’d promised myself that I’d be the one taking care of my husband on his journey through dementia, that I wouldn’t be outsourcing to help, or God forbid, a nursing home, but honestly, I was threadbare and exhausted.

All I wanted was to protect my husband: protect his health, his well-being, and his dignity. I wanted to protect myself, too, to make sure I had what I needed to care for him. It was around the holidays when I first met Tom, and my main concern was my adult children coming home and thinking that I couldn’t handle what I signed up for (even if they were right). They were going to ask about money, and I didn’t even know where the account statements were. I think we were late filing taxes.

Tom wanted to be helpful, but I was sure he didn’t understand at his age what it was like to go through the grind of long-term care, regardless of his insurance acumen. I think he sensed that as well, so he told me he wanted to better understand the problem firsthand. He told me he could sort out the money stuff and help me organize the conversations with my kids. I didn’t really have a way to pay him directly then, but he assured me that he’d throw himself into learning more by getting into details, and this was an extension of him volunteering for the Alzheimer’s Association. So I took a chance and accepted his help.

JOHN

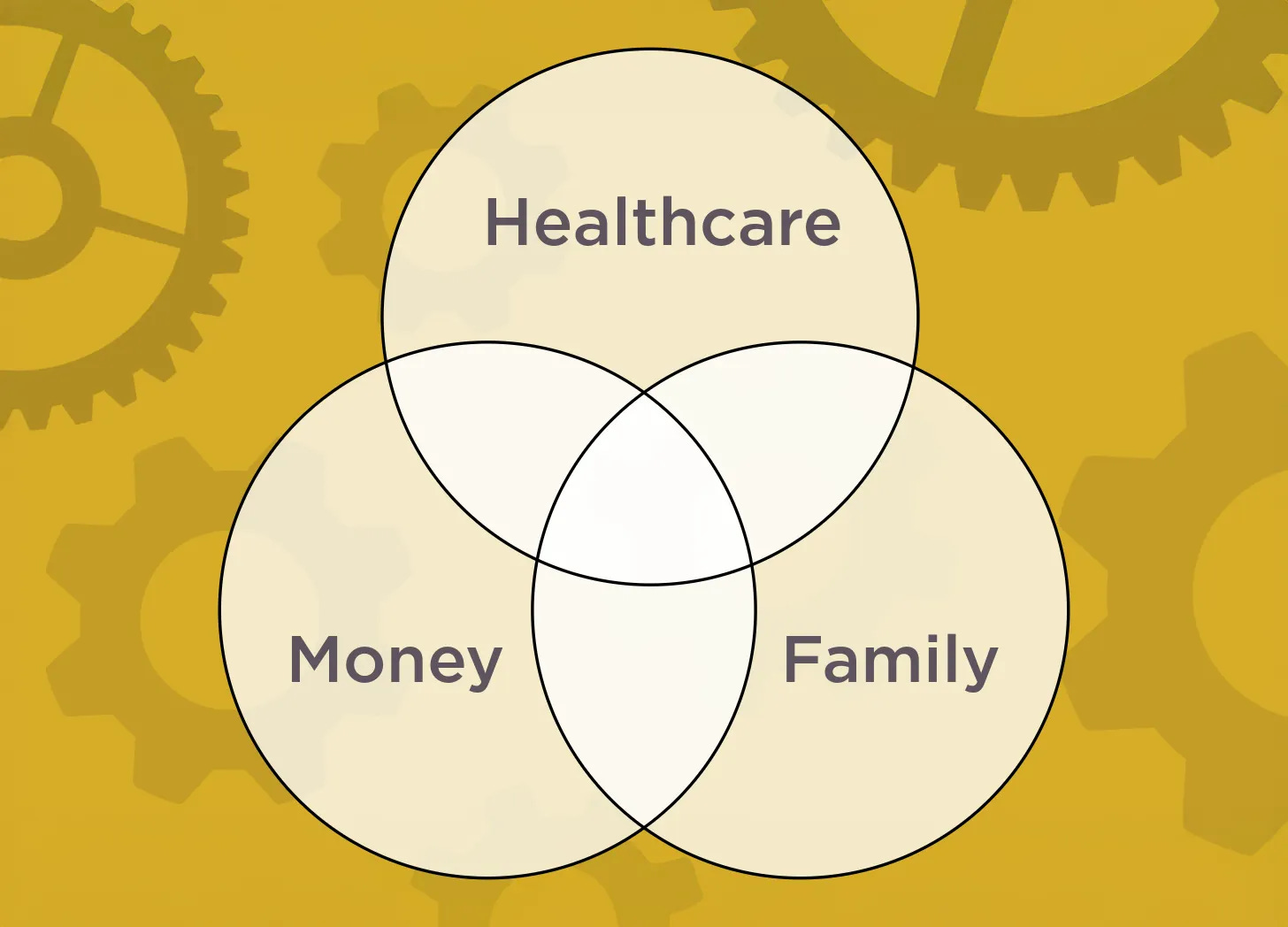

Tom came to me and asked what we could do for these families outside of financial planning and long-term care insurance. Unfortunately, the answer was not much. Unless we were selling long-term care insurance to an insurable prospect, there wasn’t really a way to make a business with what’s left. Investment brokerages don’t want clients where money is going out the door paying for care; family financial authority is in flux; and client relationships are unlikely to be long-term given the prospect’s older age. But Tom pushed still, and he and I wound up drawing this three-circle diagram:

-

Circle 1: Money, which of course we could help with. But again, more in terms of long-term care insurance vs financial planning specifically for people going through a care situation.

-

Circle 2: Family, which looked at family goals, financial planning, and legal needs, but also veered into psychological and emotional dynamics because of the heavy weight of these long-term care issues.

-

Circle 3: Healthcare, which as financial planners at the time, we simply did not deal with. But Tom made this good argument that long-term care planning really needed a health expert to help families manage complex health questions and decisions, and consequently get a revised hierarchy of priorities so we could recalibrate the ‘job of the money.’ He convinced me that without it, families were left with this enormous blind spot from a planning perspective.

That’s when he started pursuing these links between these three areas—the “spokes” between these circles.

MARY

Tom came back to me with organized financial statements in time for the family visits around the holidays. I was surprised that he had built out a financial plan that, my goodness, seemed very thorough and complicated. How we needed to anticipate costs for my husband when I might run out of gas as the primary caregiver, and to make sure I had the resources left over if I survived my husband. I remember he harped on tax planning and how medical expense deductions would alleviate what we’d owe in terms of income taxes.

I was a government professional and I had experience with complex figures like budgets, so I had no trouble following what he was proposing. But in terms of my mental energy, I just kind of checked out when he was talking details. I had no bandwidth to validate what Tom was saying, even though I knew that budgets, as it were, need to be reconciled. I just couldn’t muster up the focus to even review the stapled financial plan he left for me to review.

Caring for my husband—protecting him—took everything I had. So I took another chance with Tom. When I asked him for help, I think it surprised us both.

“Tom, if you can figure out how to manage our money and work this plan into our finances and help me with the kids, I’ll hire you right now. But be gentle with my attention. I can’t go deep into the weeds about this stuff—executive summary only. I trust you that the diligence is there, and be sure my kids are going to ask after that. But I’ll confess something to you when you were going through your very impressive but thoroughly baffling financial plan. The only thing I was thinking about when you were talking was that I forgot that my one goal that morning was remembering to eat lunch. I forgot to eat lunch. And you were still talking.

“That’s what it’s like.”

Tom put the plan back into his briefcase and said he understood. Honestly he looked a little disappointed that his hard work on the financial plan wasn’t going to be appreciated at that moment, but I needed to get back to my husband and this whole decision had worn me out.

I gave him one pointer that Betsy at the Alzheimer’s Association told me.

“Don’t forget that we aren’t the only ones who have walked this path. It’s just sometimes hard to find. And maybe we can make the path easier for those who follow.”

Epilogue

Every so often, we can experience a small moment in life that leads to a major pivot point. That’s what Mary’s “lunch” story was for me in my professional life. I wanted to help my clients like her navigate the financial, healthcare, and family aspects that are intertwined with long-term care planning. I knew then that I needed better tools, resources, and skills. Could I build a business out of this? A career? Was this a calling?

There’s still so much left to be done, and that’s why I want to share these stories of some of my clients here on Age Against the Machine and Advisorpedia (soon to become Power Advice). I’ll have much more to share in the coming weeks and months that I hope will help families going through these transitions, and the professionals that serve them.

Thank you for being part of this experiment one year in, the feedback has been uplifting and empowering.