Trending

Written by: Tom Nakamura | AGF

Supportive fiscal policy is among the catalysts that could benefit currencies in emerging markets and select developed markets.

In currency markets, several key uncertainties—let’s call them “known unknowns”—lie ahead as we approach 2026. They range from the outcome of major court rulings and crucial appointments at the U.S. central bank to potential trade deals, the tariff end game (is there one?) and upcoming elections, particularly in the U.S. These events and trends will no doubt shape the near-term market outlook, but how they will do that—well, we just don’t know.

Instead, while we try to divine what will happen in currency markets next year, let’s focus on what we do know—the “known knowns”: past monetary and fiscal policy, future demographic trends, and the likelihood that current market anxieties will eventually subside. When we do focus on that, we see a rapidly shifting landscape.

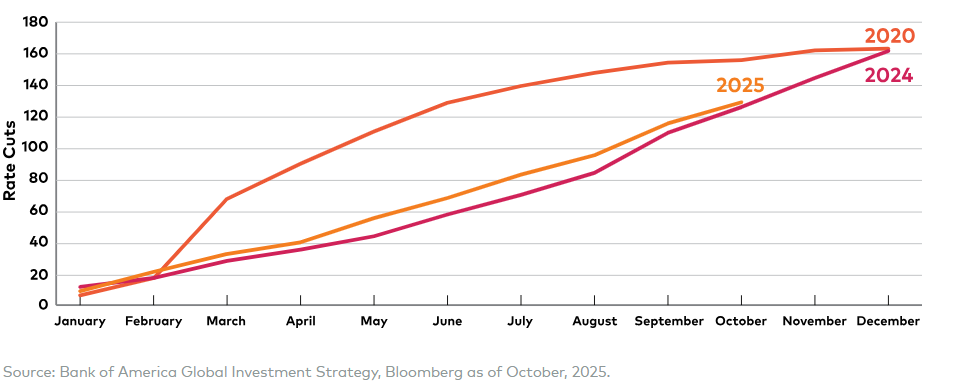

When we look back at 2025 it seems to have been defined by steady and substantial global monetary easing—much like 2024 was, too. Clearly, two years of rate cutting will support economies and benefit currencies sensitive to growth, especially in emerging and select developed markets. But the past is prologue, and 2026 is likely to see a shift in degree, if not kind, when it comes to monetary policy. We expect much shallower rate cuts around the world, as many central banks have signalled that they are close to, or in, rate ranges that broadly balance the risks of being too accommodative or too restrictive.

Cumulative Policy Rate Cuts by Year

The lone potential exception: the U.S. Federal Reserve (Fed). We think that growth in the U.S. is slowing enough to justify more rate cuts from the Fed. With an easier monetary policy path, the fiscal stimulus that Washington is likely to provide, and some moderation (we hope) of uncertainty around economic policy, the risks of a near-term recession are low. In contrast to the past two years, we think there is a strong likelihood that the Fed will be cutting more than most major central banks in the world. This would create a moderating effect on the U.S. dollar and in turn provide tailwinds for emerging market currencies and some developed market currencies.

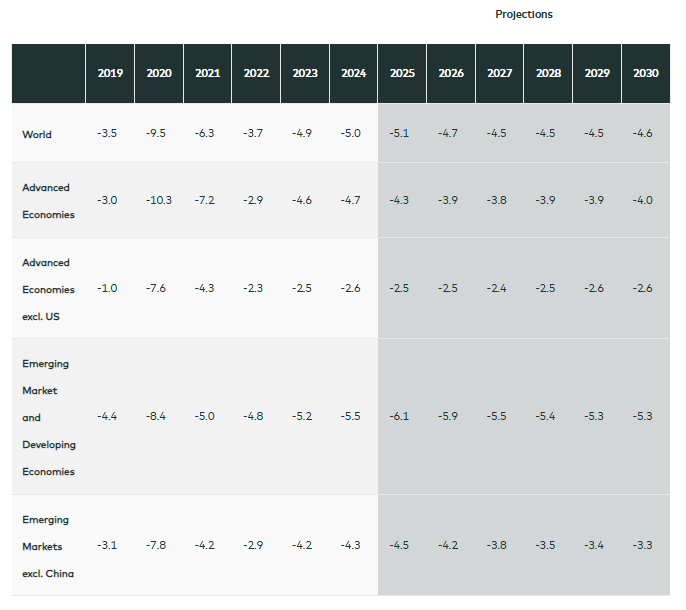

Fiscal policy remains supportive. In addition to planned stimulus in the U.S., we continue to see increased spending in several important economies, including Europe, China and Canada. We think that globally, the lagging impacts of fiscal policy continue to provide a solid backdrop for economic expansion. This, again, should benefit our favoured currencies in emerging markets and select developed markets.

Projected Fiscal Policy Continues to be Growth-Supportive

Table 1.1 General Government Fiscal Balance, 2019-30: Overall Balance

(Percent of GDP, unless noted otherwise)

Source: International Monetary Fund, Fiscal Monitor, April 2025.

This development is playing out against the backdrop of important demographic changes. In the world of economics, less is less and lower is lower. Population growth has slowed in developed and emerging economies alike, with many projected to experience outright declines in their working-age populations, based on research from the United Nations. Among developed nations, roughly two-thirds will experience such declines by 2050, posing challenges to GDP growth. We believe emerging economies are generally better positioned.

Lower potential growth could be a support for government bond markets, but only if monetary and fiscal policies are properly calibrated. As markets adjust to these structural shifts, we think there is a natural tailwind for bond markets that can get their policy mix right, and a strong tailwind for emerging economies that have strong demographic profiles.

While trade will remain an issue, there could be a long-lasting tailwind if the Canadian government is able to execute on plans to diversify trade relationships towards other economies to both the east and west.

Note that Canada ranks slightly ahead of the U.S. in terms of population growth and is expected to be one of the more strongly growing developed economies going forward. So, what do we make of our much-maligned Canadian dollar? 2025 proved a challenging year for the CAD, and with some good reason, as it was weighed down by strained U.S. relations and export dependency. Concerns over the joint review of the U.S.-Mexico-Canada trade agreement also dampened sentiment.

We think that a rebound is possible in 2026. Positioning, often a contrarian indicator, is very light. With Bank of Canada rate cuts likely complete, interest rate differentials will improve. Global growth, supported by the mix of monetary and fiscal policies discussed earlier, could help Canada’s export sector. Demographics, as we showed earlier, are a net positive, too.

While trade will remain an issue, there could be a long-lasting tailwind if the Canadian government is able to execute on plans to diversify trade relationships towards other economies to both the east and west. If that is coupled with sound investment in productive assets domestically, it could pay large dividends in the long run. We are not sure that the moment is now, but we think that some of the negativity on the Canadian dollar can lift and unlock a period of outperformance.

So, here is what (we think) we know: Supportive monetary and fiscal policies should drive near-term global growth, while demographic headwinds pose longer-term challenges. Emerging markets are generally better positioned than developed economies. Countries with higher growth prospects, including Canada if it diversifies trade and invests productively, stand to benefit. Of course, those “known unknowns” still must play out—and staying agile as they do will be key to success in currency markets next year.

Related: Why 2026 Could Be a Turning Point for Hope, Renewal, and a Better Society