Trending

Written by: Stephanie Aliaga

Before Russia’s invasion of Ukraine and its impact on commodity markets, we thought inflation might finally see its peak in February. Supply chain gauges were showing signs of easing, with shipping delays poised to improve and companies showing progress on hiring. The Russian invasion then triggered a supply shock at a difficult time for inflation.

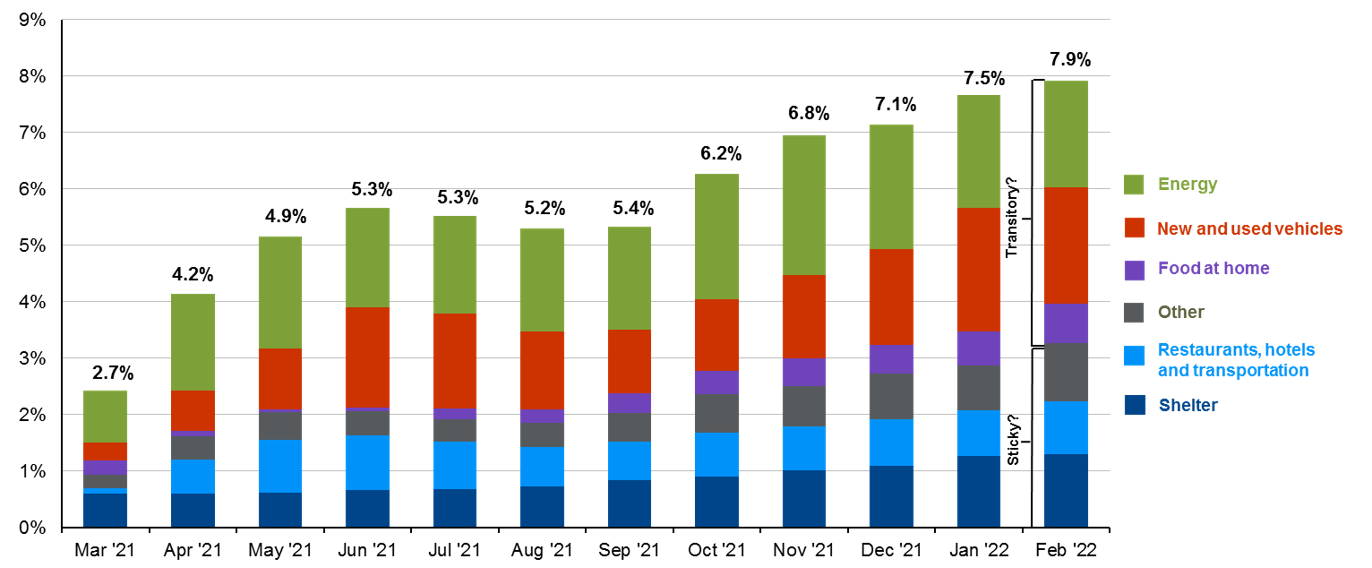

The February CPI report showed that even before the invasion, energy prices were pushing already-high inflation higher. Headline CPI climbed 0.8% m/m and 7.9% y/y while Core CPI (excluding food and energy) rose 0.5% m/m and 6.4% y/y. Gas prices drove inflation, skyrocketing 6.6% and contributed nearly a third of the monthly price gains. Other strong gains came from food, shelter and services sectors that were most impacted by Omicron. It’s worth remembering that food and energy prices are typically volatile, which is why the Fed excludes these measures in their preferred measure of inflation. That being said, much higher oil prices for a sustained period of time could have a significantly negative impact on the U.S. economy.

Higher energy prices could –

- Dig into consumer wallets. If oil prices stayed around $120 per barrel for the rest of the year, gasoline would likely average $4.20 compared to an annual average of $3.09 in 2020. We estimate that this would add over $1,000 to the expenses of the average household.

- Lead to higher inflation expectations through higher wage demands and altered consumer psychology.

- Spill over to the costs of broad goods and services by further raising a variety of input costs.

- Negatively impact consumer sentiment, which could impact consumer spending and lead businesses to pull back on hiring and expansion efforts.

With that said, the U.S. economy does have significant buffers for protection against this storm. Households are sitting on an estimated $2.5 trillion of excess savings accumulated throughout the pandemic and have seen very strong wage gains[1]. Further, pent-up demand in services sectors after two long years of the pandemic could provide an important growth offset to the impacts of higher energy prices.

Still, Russia’s stranglehold on global commodity markets likely means higher energy costs for longer, further strains on supply chains and complications for global economies with varying Russia exposures. All in, this will likely postpone the inflation peak to later this year. Looking further ahead, we do expect inflation to cool to a more sustainable level. The long-term forces that have suppressed inflation in recent decades—income inequality, the collapse of trade unions, and growth of information technology—have not simply gone away (as explained in “Inflation: A Somewhat Sticky Situation”).

In the meantime, the Fed is gearing up to combat these rising price pressures, and is set to raise interest rates by 0.25% next week. We anticipate the Fed will hike less aggressively than markets are currently pricing given the aforementioned growth concerns, but the persistence and breadth of hotter inflation may result in a more extended hiking cycle than was originally penciled in.

Ahead of March FOMC meeting, inflationary pressures are broad-based

Contribution to y/y % change in CPI, seasonally adjusted

Source: BLS, J.P. Morgan Asset Management. Headline values reflect the seasonally adjusted year-over-year % change in CPI. Values may not sum to headline CPI figures due to rounding and underlying calculations.Shelter includes owner's equivalent rent and rent of primary residence. Other primarily reflects household furnishings, apparel, and medical care services. Data are as of March 10, 2022.

Related: Has the Outlook for Monetary and Fiscal Policy Changed?