Written by: Hal Cook: Senior Investment Analyst, Hargreaves Lansdown

During a challenging year for investors in 2022 Hargreaves Lansdown fund analysts take a look at how active UK and US fund managers performed against their passive peers.

- Performance: the proportion of active managers that outperformed was lower than usual

- Fund flows: passive funds continued to take market share, defined as being proportion of total assets invested

- Should we all just switch to passive funds?

In terms of performance of equity fund managers, most active managers underperformed their passive equivalents over 2022. This shouldn’t be a surprise: one year is a short time period, giving active managers limited scope to outperform – most have targets based on at least three to five years’ worth of performance.

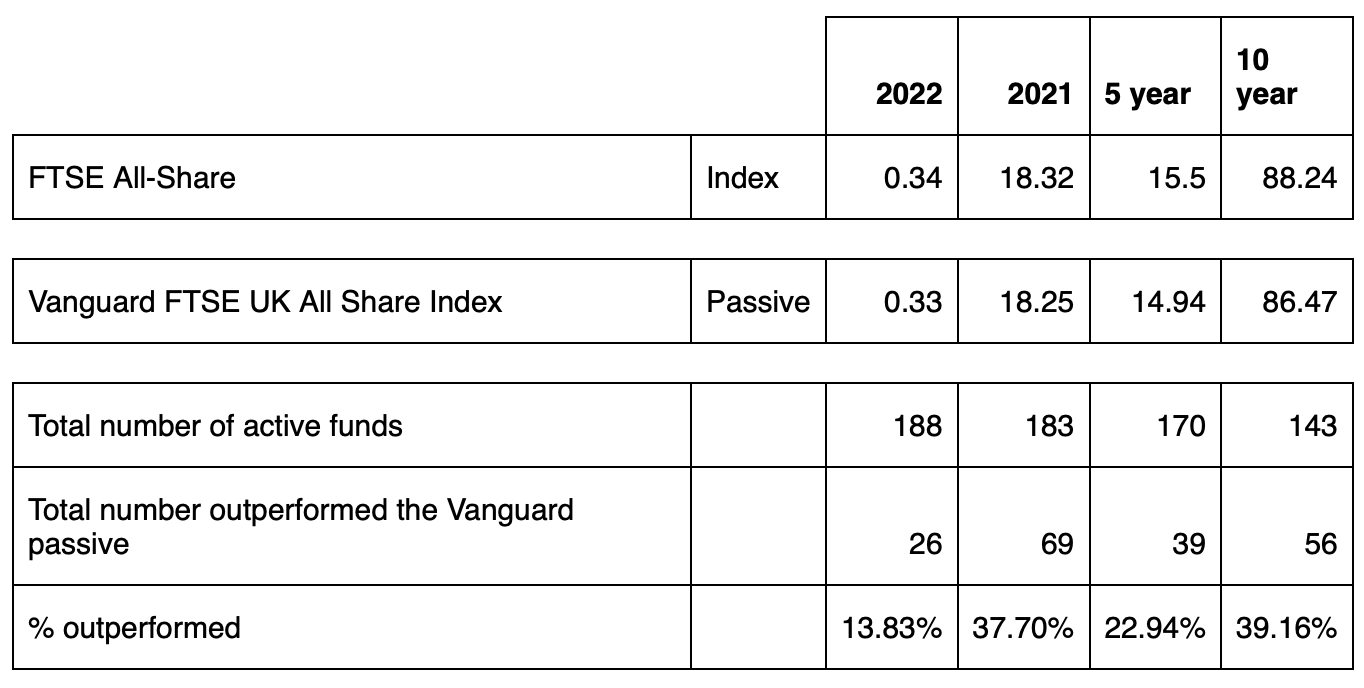

Historically UK equity managers have shown better ability to outperform passive equivalents than managers in most other regions. This was not true in 2022, with the Oil & Gas sector adding notable performance to the FTSE All Share, and in turn, passive funds, and small and mid-sized companies underperforming their larger counterparts. Typically, UK managers have a greater proportion invested in small and mid-sized companies when compared to their passive equivalents and historically this has been a tailwind for relative performance. The Oil & Gas sector exposure is more varied, but with the rise of responsible investing, it is now more common for UK equity managers to have lower exposure to this area of the market.

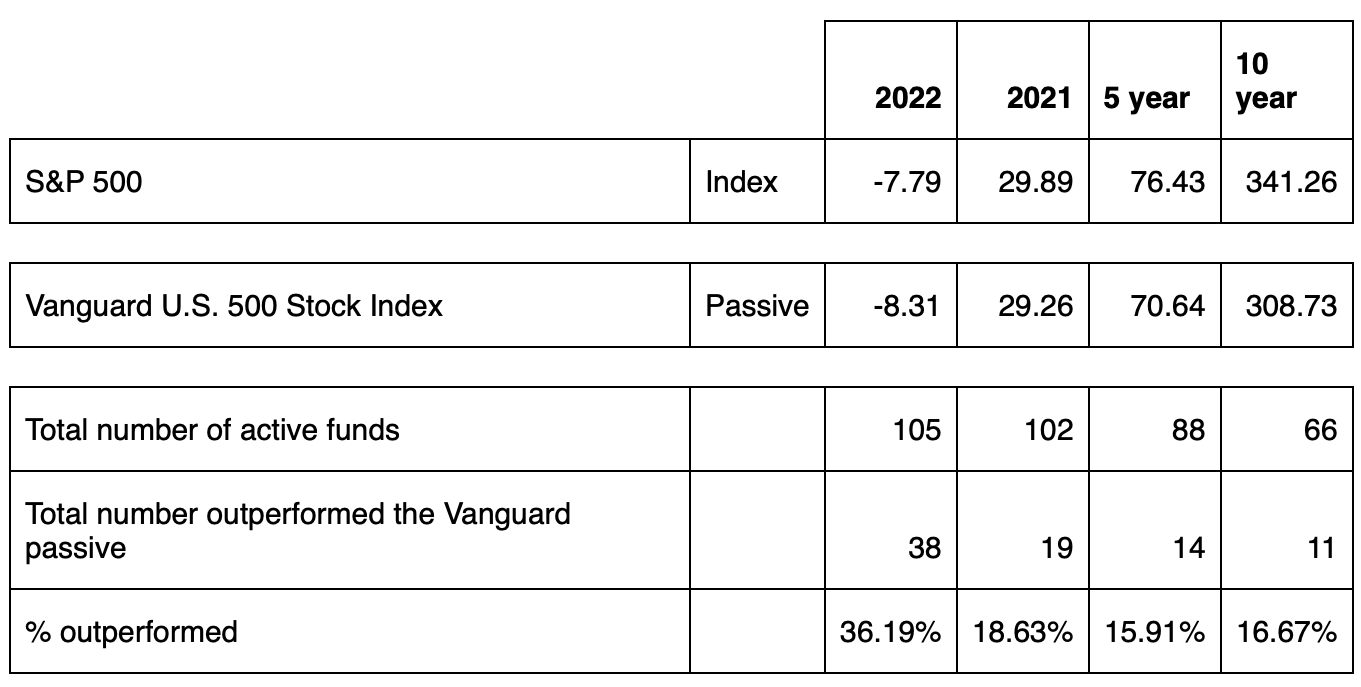

US equity managers saw the opposite effect: a greater proportion outperformed during 2022 than the historic average. It’s notoriously difficult to outperform passive funds in the US consistently over time, in part due to the amount of people analysing companies there along with the sheer volume of information available. A large part of the losses in the US came from the Technology sector which was deemed to be very highly valued by mid-2021, meaning a lot of active managers had less invested in these companies for fear of a downward correction in share prices. Long-term though, most active managers underperform passive funds in the region.

In terms of market share, passive funds continued the trend of increasing the size of their slice of the pie: in 2010 about 10% of assets invested in mutual funds were passive in nature, this has increased to around 25% by the end of 2022. Despite falling markets in 2022, passive funds continued to see net inflows, while active funds saw net outflows.

This is all a bit damning for active funds: they seem to struggle to outperform with any sort of consistency and are becoming less popular over time. So, shouldn’t we all just switch? I’m going to continue to answer that with a no. There are a couple of reasons why.

Firstly, the performance data here is averages: while the average manager didn’t outperform, there are some that did. And there are some that do manage to outperform consistently over time. Secondly, this data just tells you if something outperformed or underperformed the passive. It doesn’t tell you by how much. One year of large outperformance and four years of small underperformance can still result in outperformance over the long-term.

The UK – how does the data stack up?

The US – how does the data stack up?

Source: Lipper

Related: Low Returns and High Volatility? Time To Consider Covered Calls?