Trending

Written by: Steven D. Bleiberg | New York Life Investments

An odd thing has been happening lately – people who should know better are blaming a variety of economic ills on an unlikely villain: the desire of investors to earn good returns on capital. Not enough oil wells being drilled, even with oil prices so high? Blame those pesky investors:

As to why they weren’t drilling more, oil executives blamed Wall Street. Nearly 60% cited “investor pressure to maintain capital discipline” as the primary reason oil companies weren’t drilling more despite skyrocketing prices, according to the Dallas Fed survey.1

Insufficient housing construction causing rents to rise? It’s those annoying investors again:

From a broader perspective, developers have been notably gun-shy to make big investments since 2008 because shareholders haven’t rewarded them for doing so. Instead, equity owners have prioritized prudent balance sheets and cash payouts from housing companies that were decimated in the 2008 financial crisis. Or, as Conor Sen, a Bloomberg Opinion columnist, said succinctly in our Twitter Spaces discussion Friday, “It’s a really tough thing because we think homebuilding companies are in the business of making homes, but at a certain point, it just becomes an investor base saying, ‘All I care about is return. I don’t really care about the business you’re in.’”2

So, if you own stock in a company, is wanting the company to earn a good return on the capital it invests…a bad thing? To hear these news reports tell it, if it wasn’t for those unreasonable investors with their crazy demands about earning good returns, we would have plentiful cheap oil and houses galore! But nooooo, investors want companies to earn good returns. This is why we can’t have nice things!

Irony abounds here. Most of the time, critics say that investors focus too much on the short term – e.g., did a company beat the quarterly earnings expectation? – rather than on a sensible long-term question, such as, oh, you know, is the company earning a good return on its invested capital? Examples of this criticism are not hard to find, from both sides of the political spectrum. A 2015 Huffington Post article explained “How Wall Street’s Short-Term Fixation Is Destroying The Economy.”3 And in 2018, a Wall Street Journal op-ed by Jamie Dimon and Warren Buffett, no less, proclaimed that “Short-Termism Is Harming the Economy,” and urged public companies to get out of the business of providing guidance on quarterly earnings.4 Today, though, we are asked to believe that the problems in the oil and housing sectors (high prices, not enough supply) are the result of investors being too focused on the long term. We used to hear a lot about the Goldilocks economy – not too hot and not too cold; apparently critics are now looking for the Goldilocks investor – not too short-term, and not too long-term.

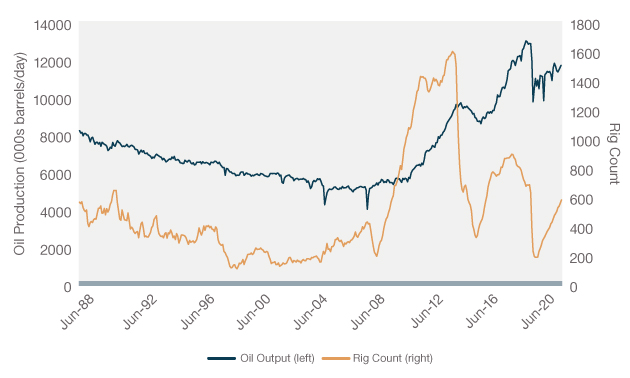

At Epoch, we think that wanting companies to earn good returns on their capital is in fact a good thing. (We’re really going out on a limb here.) So, what do we make of the issues in the oil and housing industries mentioned at the top of this piece? It helps to begin by putting things in perspective. Let’s start with oil. Figure 1 shows how the U.S. rig count (i.e., the number of oil rigs that are actively pumping oil) has moved over time, together with the price of oil (Figure 1).

Source: Bloomberg, as of June 2022.

You might have gotten the impression from listening to the news that oil drillers have not reacted at all to the rise in the price of oil over the last year. Yet the rig count has roughly tripled, from a low of 180 to its most recent level of 574. True, the increase in the rig count has not been proportionate to the rise in the price of oil the way that it was after the financial crisis of 2008, but keep in mind that this earlier period saw the spread of the new hydraulic fracturing technology (i.e., “fracking”), and that has made wells more productive (in terms of output) than they used to be. In Figure 2 we look at the rig count again, but also at the actual production of oil (in thousands of barrels per day) (Figure 2).

Source: Bloomberg, as of June 2022..

Oil production in the U.S. had peaked at around 10 million barrels per day back in 1970 and, by the early 2000s, had fallen to half of that level. But fracking drove a huge boom in oil output, even under the purportedly “anti-oil” (at least if it came from federal lands) Obama administration. By the beginning of 2020 the U.S. was producing almost 13 million barrels per day, until COVID came along and crushed the demand for energy. But output began to recover by the end of that year and today, the U.S. is producing 25% more oil per day than it was in 2014, with only about a third as many rigs operating. Yes, output could be higher if the oil companies operated more rigs (or added new ones), but that decision is influenced by a mix of factors, from government policy (which turned rhetorically hostile to fossil fuel production again after the Biden administration came in), to doubts about the economic outlook as the Fed raises interest rates to try to curb inflation, to yes, concerns that additional wells will not earn a good return on investment if the price of oil falls in response to increased production (or to an economic slowdown). That last factor is a perfectly legitimate one for companies to consider. To believe, however, that this factor, and this factor alone, is somehow restricting the supply of oil is to ignore both the importance of the other factors involved, as well as the actual data on how much oil is still being produced, which is only about 10% off its all-time high. Investors demanding good returns on investment have not created some huge oil production shortfall.

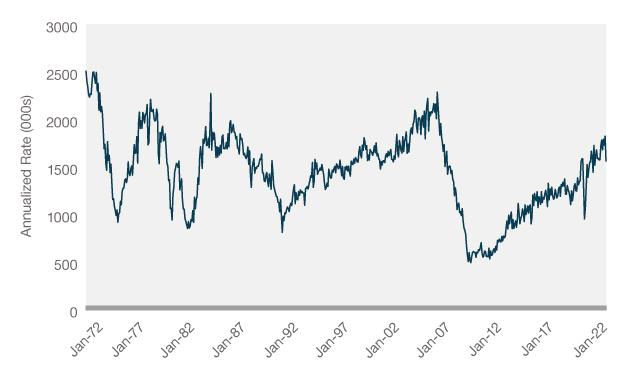

Now let’s turn to housing. Figure 3 shows the number of housing starts in the U.S. on a monthly basis going back fifty years (Figure 3).

Source: Bloomberg, as of January 2022.

Housing starts collapsed between 2006 and 2009, for well-known reasons – i.e., we were way too lax in lending money to people who really couldn’t afford it so they could buy houses in the years leading up to 2006. The result was that vast numbers of people defaulted on those loans, creating a huge overhang of houses for sale that took several years to work off, not to mention sparking a huge financial crisis as banks found themselves holding all sorts of suddenly much less valuable derivative securities tied to those now-defaulted mortgages. Since 2009, however, housing starts have marched steadily upward, thanks to generally rising incomes and low interest rates, which have made houses affordable to many new buyers. In recent months, housing starts have been at a higher level, apart from the peak years of 2003-2006, than at any time over the last thirty-five years. And as we just discussed, the numbers during that peak period were in essence artificially boosted by what turned out to be disastrously generous lending standards – hardly a benchmark we should hold out as our goal. (Today’s numbers would look lower compared to the past if we adjusted for population growth, admittedly.) So, as we saw with oil, there really isn’t strong evidence that return-conscious investors have been driving some sort of restrictions on housing supply. Why are rents rising in some places? You can blame a host of other factors for localized supply issues: zoning regulations and “not in my backyard” opposition to more housing, among others. But it seems silly to blame it on investors wanting to earn a good return.

Earning a return on invested capital that is higher than the cost of that capital is simply the way a company increases its value. It is no different than the way an individual increases his or her net worth. If you went out and borrowed money at a 5% interest rate and invested it in a project that earned 9%, you would grow your wealth; if the project only earned 3%, you would find your wealth reduced once you paid off the loan. That is not a sustainable outcome for companies any more than for individuals.

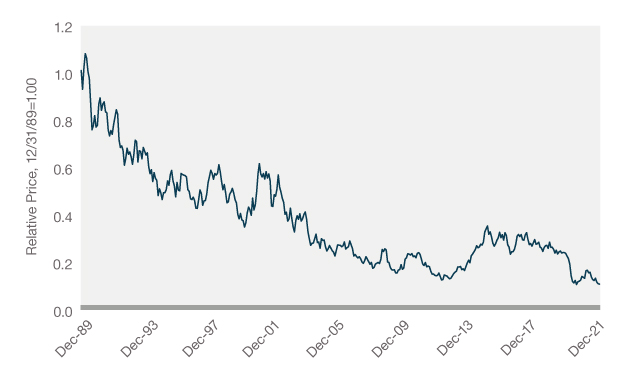

To see what happens when an industry fails to earn its cost of capital, consider the U.S. airline industry’s performance over the decades. For years, the industry struggled with the effects of too much capacity for a product – a seat on a flight – whose value depreciated to zero if the flight took off with the seat empty. This combination led to endless fare wars, which were great for consumers but terrible for the profitability of the airlines, many of whom made more than one trip through bankruptcy. Figure 4 shows how the S&P 500 Airline Index performed compared to the overall S&P 500 since the end of 1989 (Figure 4).

Source: Bloomberg, as of December 2021. Past performance is no guarantee of future results. It is not possible to invest directly in an index.

Over the 25 years through 5/31/22, the S&P 500 Airline index produced an annualized total return of just 1.2%, compared to 8.5% for the S&P 500. But even 3-month Treasury Bills*, the ultimate risk-free investment, earned 1.9% per year over that time. Investing in an industry that earned poor returns destroyed wealth for those investors.

Airline consolidation eventually solved the capacity issue, reducing the frequency of unprofitable discounting and enabling airlines to start charging additional fees (for luggage, meals, etc.) without worrying whether other airlines would follow suit. Profitability within the industry did improve over time, and the stocks enjoyed better relative returns (outperforming the S&P 500 for the decade ending in 2018, for example). Consumers, having been spoiled by the years of cheap airfares they previously enjoyed, could (and did!) complain in recent years that the airlines’ ability to earn better returns on capital had come at their expense. The truth is that when they were enjoying those cheap airfares in earlier years, they weren’t bearing the true cost of their flying – airline investors were. And it was not unreasonable for those investors to want the airline industry to change the way it operated, even if it meant higher fares for flyers. No industry can be expected to survive if it is not creating value for the investors in that industry. And that would be the worst outcome of all for consumers. Earning good returns on capital is not an obstacle to satisfying consumer demands; it’s what enables companies to continue to satisfy those demands.

Related: October Optimism Continues but Cost-of-Living Problems Still Linger