Trending

The market’s biggest stories this week were all about what was falling.

Technology stocks tumbled, and several of the market’s biggest winners faced additional selling pressure. But beneath the headlines, the broader market continued to strengthen. If you’re only watching the S&P 500 or the Nasdaq, then you might have missed that the equal-weight S&P 500 hit a new all-time high. Rather than signaling a breakdown, the week’s action suggested that leadership is once again expanding beyond a narrow group of technology companies.

The newest bullish catalyst is a sharp decline in oil prices, which could be creating a powerful tailwind for both the economy and financial markets.

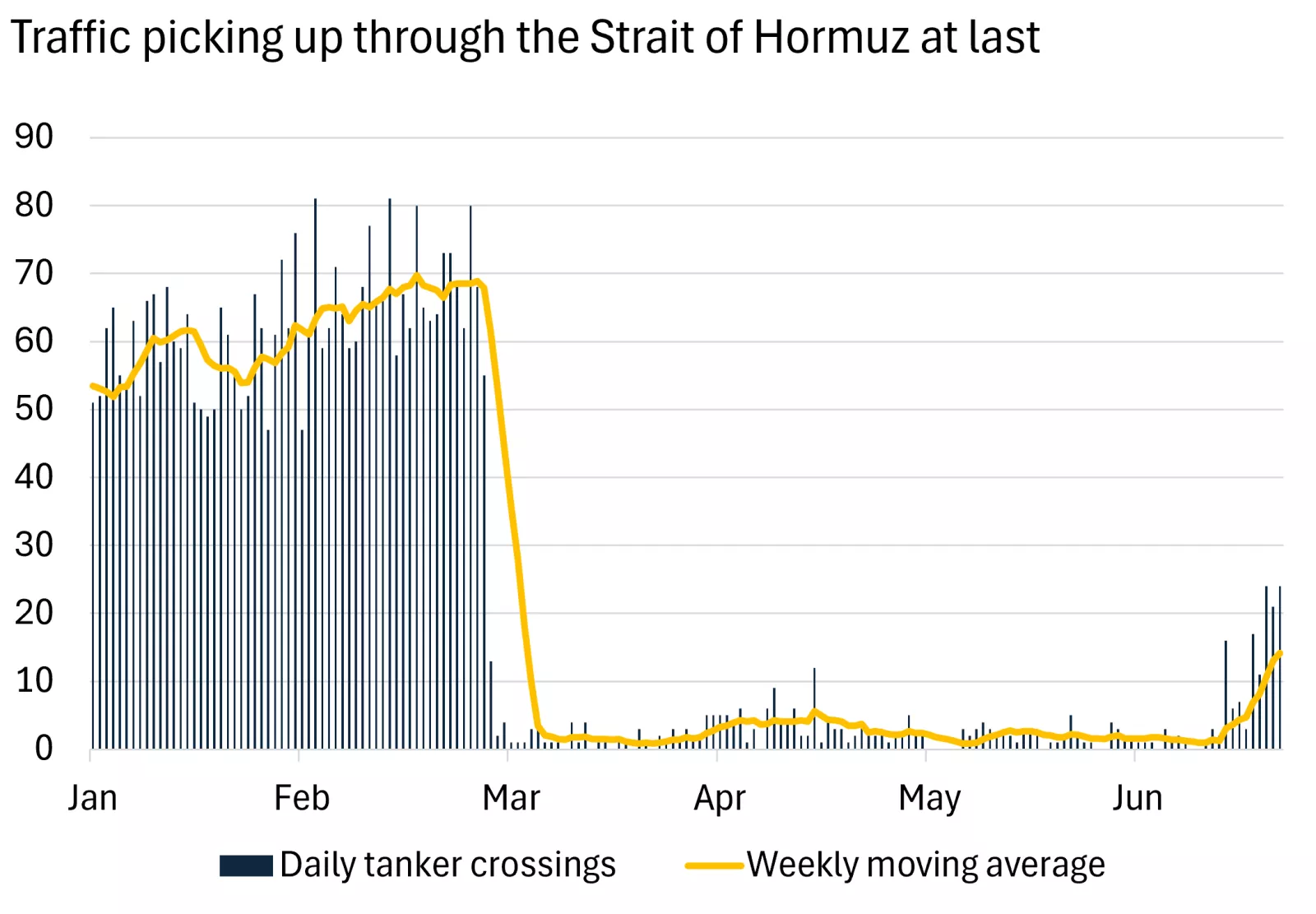

As the U.S.-Iran peace agreement continues to hold and energy transportation through the Strait of Hormuz recovers, investors are beginning to focus on a future with lower inflation. Consumers have been spending through the pain (the American way!), and falling inflation will ease the burden on both household budgets and lower the stress level of brand-new central bank chairmen everywhere.

Technology stumbles

Recent weakness in technology stocks has understandably captured attention and resurfaced bubble concerns. The Nasdaq fell roughly 3% during the week, while the largest technology companies continued to struggle after an exceptionally strong rally earlier this year. Even SpaceX, which generated enormous excitement following its record-breaking IPO, has now fallen roughly 25% from its post-debut peak.

Far from universal, the weakness appears increasingly selective within technology rather than market-wide. The Dow Jones Industrial Average and Russell 2000 both posted gains, while the equal-weight S&P 500 continued to outperform its market-cap weighted counterpart year-to-date. Large-cap value stocks also significantly outpaced growth stocks. This widening participation suggests investors are rotating into other sectors rather than abandoning stocks altogether.

Created with TradingView

Several factors likely contributed to the pressure on technology shares. Concerns about speculative positioning, China’s AI pace, and signs of investor profit-taking after a rapid advance all played a role. The fundamentals behind artificial intelligence spending remain intact, so we can’t hang this on a thesis-breaking event. The story increasingly appears to be one of rotation rather than deterioration.

Micron, which reported earnings on Wednesday, delivered strong earnings and guidance, which should reinforce that demand for AI-related infrastructure remains robust. Yet even it ended the week lower after yo-yoing midweek.

Oil prices deliver refined optimism

One of the most important stories of the year happened outside the stock market.

Source: Bloomberg via Edward Jones

Based on the mostly stable US-Iran peace agreement and the rising traffic through the Strait, WTI crude fell below $70 per barrel, down nearly $25 from a month ago and more than $40 below its 2026 peak. If sustained, lower energy prices could have significant implications for global economic conditions.

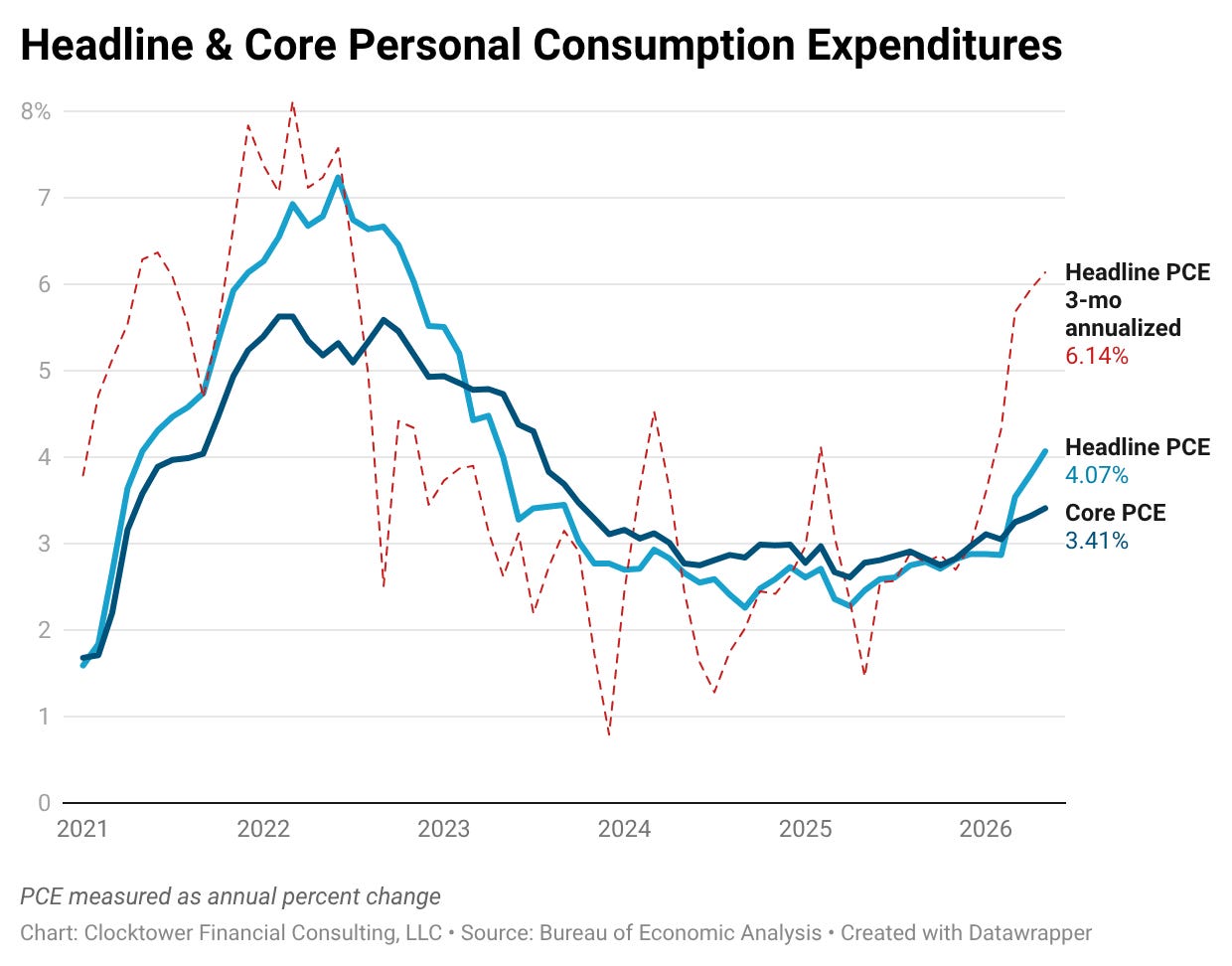

Inflation has been heavily influenced by higher energy costs this year, with energy contributing roughly 60% of the increase to the rise in headline consumer prices between April and May. The recent decline in oil prices should help reverse part of that inflation surge over the coming months, creating what could become a much-needed disinflationary trend through the summer.

Consumers may be among the biggest beneficiaries of the reduced tensions in the Middle East. Despite elevated inflation, household spending remained resilient through May, supported by lower savings rates and continued confidence. Falling gasoline prices should ease pressure on household budgets just in time.

The final GDP estimate for Q1 showed a weak contribution from consumer spending, while AI infrastructure carried the quarter. Combined with an improving labor market, a rejuvenated consumer could further lift GDP growth. Healthy business activity, lower energy costs, and continued spending will provide more reasons to remain constructive on the economic outlook.

The Fed remains cautious

Bond yields moved lower during the week, with the 10-year Treasury yield falling below 4.40% for the first time in over a month. Investors have modestly reduced expectations for future rate hikes as energy-driven inflation pressures begin to ease. However, the Federal Reserve is in no mood to declare victory just yet.

While headline inflation may improve, core inflation remains elevated. The Fed’s preferred inflation measure (Core PCE) showed prices rising 3.4% year-over-year in May, well above its 2% target. Policymakers are likely to remain cautious until they see broader evidence that underlying inflation pressures are moderating.

The Fed appears positioned to stay on hold rather than move toward either additional tightening or easing. Fed officials continue to signal they are prepared to act if inflation proves more persistent than expected, which currently puts the hawks in the driver’s seat.

What this means for investors and what’s next

The coming week will provide another important test of the economy with the monthly employment report and the start of a holiday-shortened trading week. Investors should pay attention to whether the recent rotation away from technology into other sectors fades or accelerates for clues on investor sentiment changes.

For long-term investors, the bigger picture hasn’t changed. The economy is taking these hits like Rocky and keeps punching back.

Lower oil prices, resilient economic growth, improving market breadth, and expanding earnings participation all point toward a healthier market environment than gloomy headlines might suggest. While technology may continue to experience volatility after its powerful rally, broader participation across sectors and company sizes is often a positive development during bull markets.

As I’ve said before, some healthy sell-offs can be healthy long-term, and markets rarely move in a straight line. If you’re feeling your nerves, this is just the price of admission. Don’t forget how far the market has come since March 30th.

-

Russell 2000 +25%

-

Nasdaq +22%

-

S&P +16%

-

Dow +15%

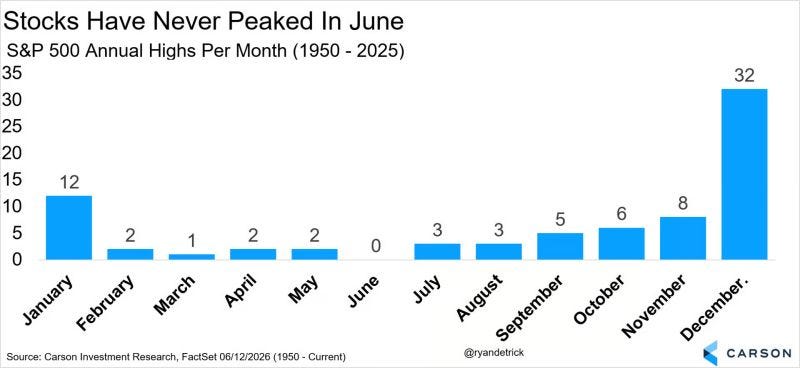

Lastly, although it offers zero prediction power, this chart from Carson Wealth is a nice little stat to lean on.

Source: Carson Wealth, @RyanDetrick

Thanks for reading—Stephen

Related: Stocks Rise Despite a Hawkish Fed and Middle East Uncertainty