Trending

A new Fed chair and a tentative peace agreement turn the page on a rocky few months. Easing oil prices and a hawkish Fed competed for market control this week.

Markets spent the holiday-shortened week balancing two major developments: the first Federal Reserve meeting led by Chair Kevin Warsh and a diplomatic breakthrough in the Middle East. While both events reduced some economic uncertainty, there are still plenty of unknowns.

The biggest market-moving event came from the Federal Reserve. Kevin Warsh put his particular stamp on his first press conference and set himself apart from his most recent predecessors by moving away from forward guidance and back toward more opaque communication. He held firm against substantial coaxing from the journalists.

Investor sentiment improved after the U.S. and Iran signed a memorandum of understanding, helping push oil prices lower and easing some inflation concerns. However, the US is only just beginning the high-stakes negotiation phase over Iran’s nuclear program and tensions between Israel and Lebanon risk upsetting the current peace.

The news of the week caused stocks to slide from their weekly highs by the close of Thursday. Despite those challenges, stocks still finished the week higher. The Nasdaq Composite led the major indexes with a 2.43% gain, followed by the Russell 2000 and S&P 500, which rose 1.21% and 0.93%, respectively.

A Hawkish Pause Under New Leadership

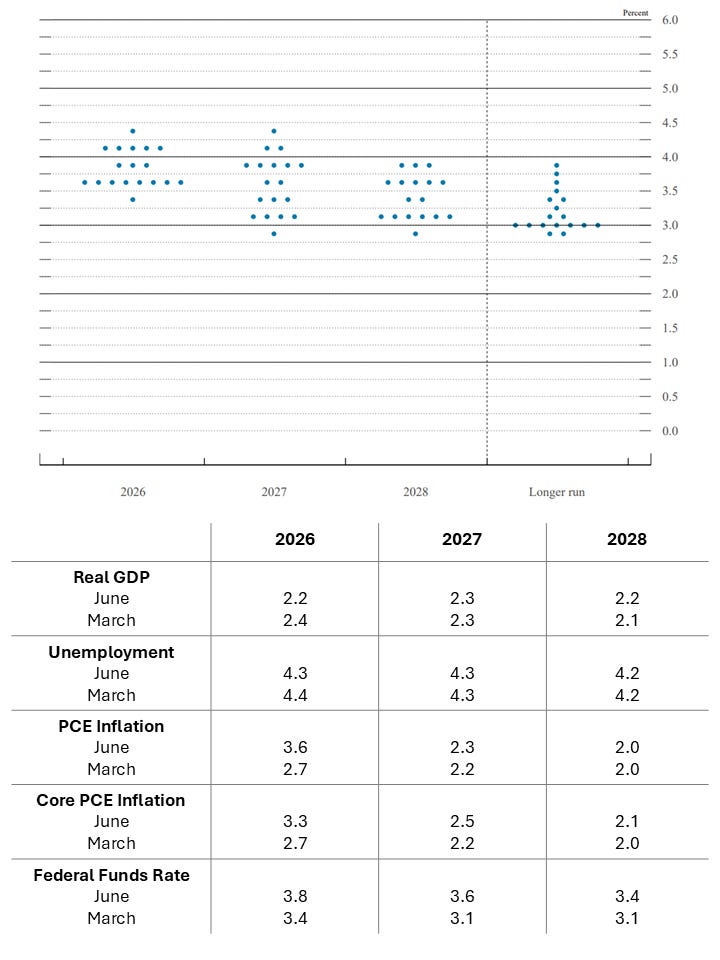

As expected, the Federal Reserve left the federal funds rate unchanged at 3.50% - 3.75%. Although the brevity of the policy statement raised some eyebrows, the real story was found in the Fed’s updated projections and Warsh’s first press conference appearance as chair.

Policymakers raised their inflation forecasts, removed a previously expected rate cut from their outlook, and signaled a greater willingness to keep policy restrictive if inflation remains elevated. GDP and unemployment projections fell 0.2 percentage points and 0.1 percentage points, respectively.

Nine Fed officials now expect at least one rate hike in 2026. Of those expecting a hike:

-

Three expect one hike

-

Five expect two hikes

-

One expects three hikes

Eight others expect to hold rates steady. Only one member expects a cut by the end of the year. Also, Warsh abstained from placing any dots of his own.

Just a few months ago, investors were asking when the Fed would begin cutting rates. Today, the question is how long will rates need to stay elevated to bring inflation back toward the central bank’s target. Warsh made it clear with no ambiguity that his Federal Reserve intends to bring inflation down.

“This committee will deliver price stability.”

The markets reacted accordingly. Short-term Treasury yields moved higher as investors repriced expectations for future policy, and stocks briefly sold off following the announcement before recovering to close out the week.

Inflation Remains the Key Variable

The Fed’s more cautious stance reflects a recent pickup in inflation and a labor market that is healthy enough to let the Fed focus on the worsening inflation. Unemployment remains relatively low at 4.3%, job openings continue to exceed the number of unemployed workers, and wage growth remains contained at a rate below inflation.

Headline inflation has been moving higher due largely to rising energy prices, while core inflation has increased more modestly. Policymakers do not appear overly concerned about the inflation driven solely by oil prices. Inflation that spreads into goods and services could cause a reset of long-term inflation expectations and that should rightly be keeping them up at night. Inflation expectations are still frighteningly high but appear to be rolling over in the most recent University of Michigan and New York Fed reports.

The June meeting was baked in for a hold from the get-go, and the convenient news that the war may be winding down lowers the urgency on inflation slightly. This combination supports the view that the Fed is likely to stay on hold rather than rush into another rate hike. While policymakers have clearly adopted a more hawkish tone, they are not yet signaling the need to begin of a new tightening cycle.

At this point higher for longer does not necessarily mean higher and higher. I continue to be deeply concerned by the inflation trends, but it could be (I hope) that the worst is behind us.

Markets Look Beyond the Fed

As big as the Fed meeting was this week, investors gave equal attention to improving geopolitical developments.

The agreement between the U.S. and Iran helped lower oil prices throughout the week, with crude falling sharply from recent highs. The prospect of reopening the Strait of Hormuz reduced fears of prolonged supply disruptions and eased pressure on inflation expectations.

Lower energy prices helped support risk appetite, particularly in technology stocks. Semiconductor shares remained volatile, but the technology sector was among the week’s strongest performers. Meanwhile, broader market participation continued to improve, a trend that has become increasingly important as investors look beyond a handful of mega-cap leaders.

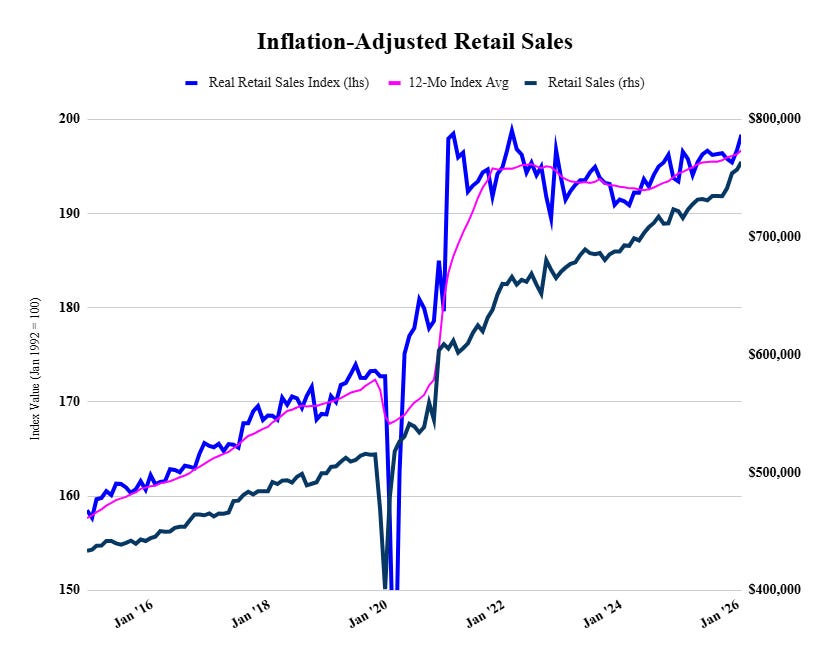

Economic data painted a mixed but generally resilient picture. Retail sales rose more than expected in May and even rose on an inflation-adjusted basis which highlights relatively healthy consumer spending despite the elevated prices and borrowing costs.

Housing starts disappointed badly while pending home sales showed some strength. Overall housing activity continues to be in a depression, reflecting the ongoing challenges of affordability, higher mortgage rates, and poor builder sentiment.

Overall, the collection of available data suggests the economy continues to expand, even as certain parts feel the weight of higher interest rates and weak labor demand.

What this means for investors and what’s next

The market moved on from the will-they-or-won’t-they drama in the Middle East months ago, but is still likely to celebrate easing tensions. The market’s primary focus now shifts from when the Fed will hike rates to whether inflation can cool enough to keep hikes off the table.

For investors, the key takeaway is that higher interest rates are not necessarily a problem if they are accompanied by resilient growth and solid earnings. So far, check and check. While policy uncertainty could continue to create bouts of volatility, the Fed is not on pace for an aggressive tightening campaign.

I continue to see opportunities in U.S. large- and mid-cap stocks, particularly as market leadership broadens beyond a narrow group of technology names. At the same time, rising short-term bond yields may offer attractive opportunities for investors holding excess cash and seeking additional income.

Markets rarely move in a straight line, but this week’s action suggests investors are still willing to look through near-term uncertainty when economic fundamentals remain intact. The path forward is bumpier than investors might have hoped earlier this year, but the broader trend still appears constructive.

That said, as many of the clouds clear on our geopolitical environment, the small pessimist in me is starting to wonder what the next challenge will be. The 2020s don’t seem likely to phone in the back half and let us all relax.

Related: Bull Market Rotation Has Begun. Is It Built To Last?