Trending

Written by: Teresa Keane, David Wong and Kent Hargis, PhD

Human behavior isn’t always rational. Perhaps that’s why so many otherwise thoughtful investors make irrational decisions—locking in losses by selling at the worst possible times or chasing stocks with overextended valuations. Is there an investment strategy that can help offset emotional behaviors that can lead an investor astray?

The Three Layers of the Human Brain

To get to the heart of why investors make irrational decisions, it’s instructive to consider the human brain and its response to pleasure and pain.

Our brains have evolved over millions of years and consist of three layers. At the core is our primitive brain, which provides the fight-or-flight instincts that keep us alive. Overlaying this is a more evolved mammal brain—the source of emotions, memories and habits that aid our decision-making. The highest level of brain function is the neocortex, which helps us process thought, reasoning and self-reflection. This is what essentially makes us human.

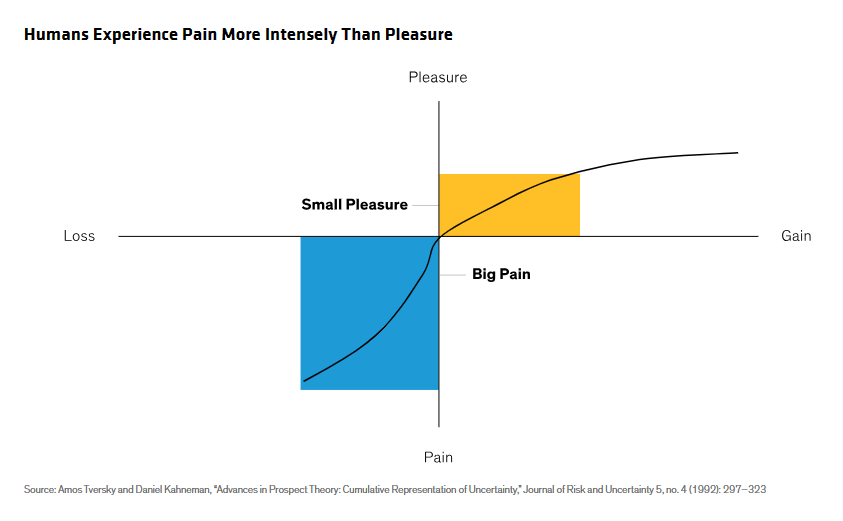

Signals from the primitive regions of our brains prompt us to seek pleasure while avoiding pain. But these same signals can overwhelm the neocortex and cause us to behave irrationally. Further knocking our reasoning out of kilter is the human propensity to fear pain much more than we enjoy pleasure.

In the investment world, this can result in some puzzling decisions.

The Loss-Aversion Bias in Action

Here’s an example, based on pioneering research by Israeli behavioral economists Amos Tversky and Daniel Kahneman.

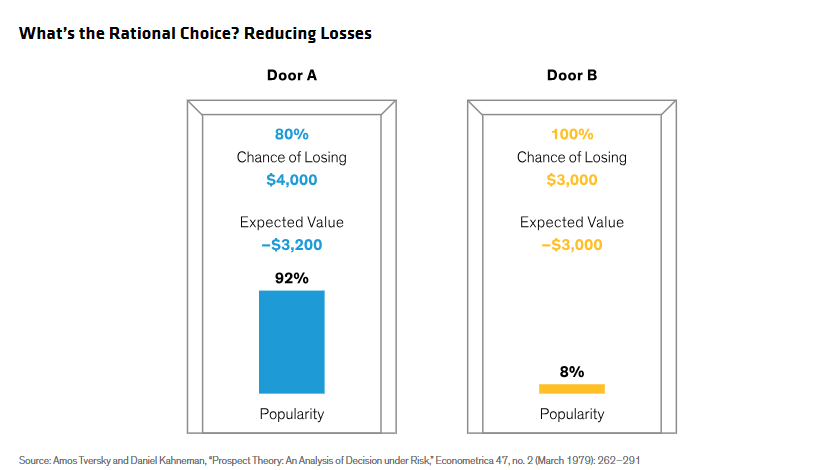

Suppose you have a choice of two doors to enter. You’re told that you have an 80% of winning $4,000 if you open Door A. (Since there’s an 80% likelihood of winning, the expected value is $3,200.) But if you open Door B, you’re guaranteed to win only $3,000. Which would you choose? Tversky and Kahneman found that most participants would choose Door B, which seems an understandable, if not profit-maximizing choice—why gamble if you can get the sure thing? Better to play it safe (Display).

The takeaway, borne out time and again in research studies, is that loss aversion trumps risk aversion. People will assume more risk to avoid losing money than they will to make money. In fact, Tversky and Kahneman concluded that humans feel the pain of loss two to three times more acutely than they feel pleasure of gain (Display).

This ratio can clearly have implications on investment decisions. Defensive equity strategies offering a pattern of performance that gives up a little bit of upside in rising markets in return for downside risk reduction that’s two to three times as much may be aligned with human nature. More on that idea shortly.

Investors Can Overestimate Their Stock-Picking Prowess

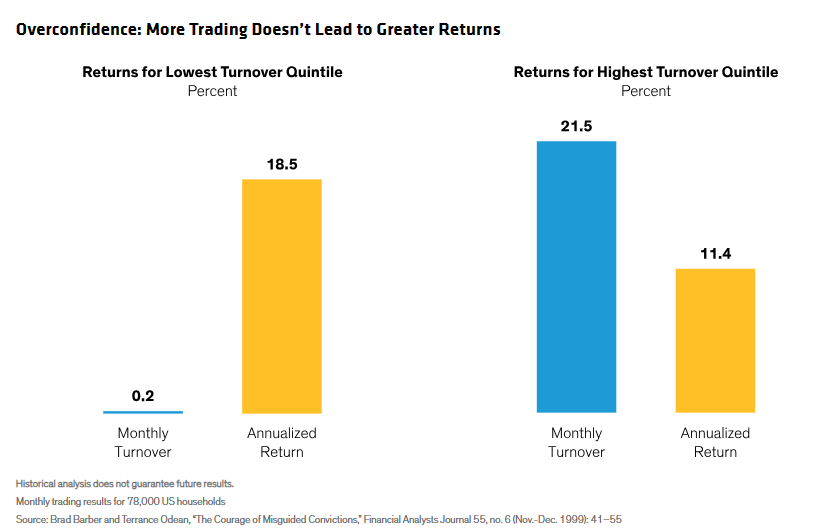

Another human bias is overconfidence. A 1999 study of nearly 80,000 US households found that households that traded the least frequently—as measured by portfolio turnover—enjoyed annualized returns 7 percentage points higher than households that traded the most. Researchers attributed this difference to investors’ overconfidence in their own stock-picking ability—overconfidence that resulted in lower returns (Display).

All too often, investors let behavioral biases like loss aversion and overconfidence affect their investment decisions. Fortunately, there’s an investment philosophy that can help overcome both overconfidence and risk-aversion biases.

The Case for Low-Vol Equity Investing

Consider an equity investment strategy that aims to limit downside capture—that is to say, exposure to falling markets—while participating in market gains, but not fully. This theoretical portfolio could be designed to capture 90% of the market’s gains in rallies, while falling only 70% as much as the market during downturns.

How does this 90%/70% defensive strategy help mitigate behavioral biases?

By targeting stocks that strike a balance between offense and defense, low-volatility investing reduces exposure to overvalued stocks that investors might chase due to overconfidence.

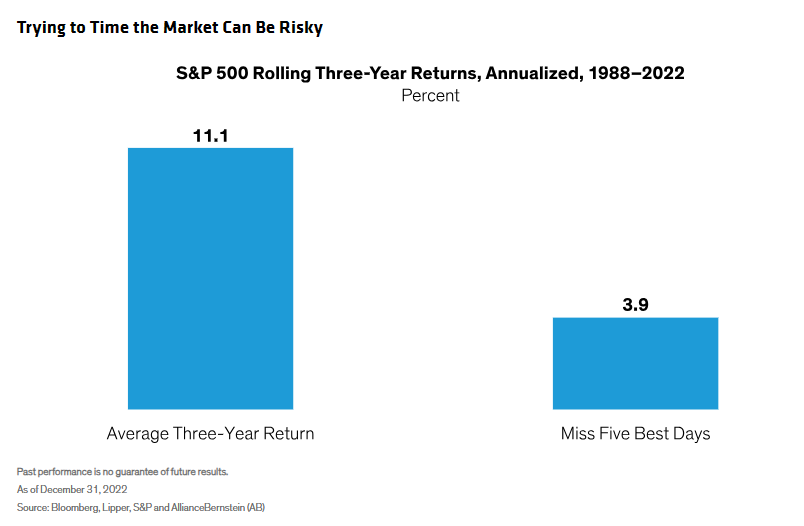

But this strategy really shows its mettle during falling markets. If successful, the portfolio would fall, on average, only 70% as much as the broader market. This helps takes the sting out of losses—counteracting the loss-aversion bias that might prompt investors to pull out of the market prematurely. It can also help counteract investors’ overconfidence in their ability to time turning points in the market, which is almost impossible to do consistently. Research shows that missing the five best days of a market rebound can have a profound impact on long-term returns (Display).

That’s because stocks that lose less in market downturns have less ground to regain when the market recovers. As a result, they can compound from a higher base during subsequent rallies.

While you might expect a low-volatility strategy to underperform over time, historically just the opposite has occurred.

Active Management Can Help Balance Risk and Return

Using data from March 1986 through June 2023, we found that a hypothetical 90%/70% portfolio would generate annual returns 3.1% higher than the MSCI World Index over this period—with less volatility in the process. We believe that the key to building such a portfolio is to focus on high-quality stocks with stable trading patterns at attractive prices (QSP stocks). Active management that utilizes thoughtful, fundamental research to find QSP stocks provides investors with more levers to manage volatility—critical in today’s environment of higher rates, macroeconomic uncertainty and geopolitical instability.

Humans are going to be human. But by understanding how inborn emotional responses can be an investor’s worst enemy, we believe that a low-volatility strategy can be constructed that counteracts behavioral biases and helps deliver better investment outcomes over time.

Related: Seeking Balance in Sustainable Multi-Asset Investing