Trending

Data recently released by the Census Bureau show that the age distribution of the U.S. population has shifted in the last 10 years: the bloc of Americans aged 30-39 grew by over 4% between 2010 and 2020, and of the top 10 ages by frequency, not one is above the age of 35. This is the rise of the “Millennial.”

This rise has been reflected in soaring home prices and broader spending data (Millennials and their younger counterparts, Gen-Z, account for roughly a third of U.S. credit card spend)1. This trend looks set to continue: Millennials are poised to inherit roughly $68 trillion from their parents by 20302. The net result of this generational shift is that money management conversations are changing, with the asset management industry paying closer attention to younger Americans.

However, generational differences and, in some cases, a distrust of the financial services industry stemming from coming of age during the GFC, can make navigating these conversations a challenge. Below are series of “best practices” that can make these conversations more fruitful:

- Communication preferences: “digital first” – but not “digital only”

“Cold calls” on the phone are unwelcome, and communication preferences tend to skew digital for first contact, either with a text message or an email; however, most social media is to be avoided, the result of a clear delineation between “professional” and “personal” channels. These texts or emails should be brief and to the point, but can result in a more in-depth conversations, either over the phone, virtually or in person.

- Experiences are valued and “perks” are welcomed

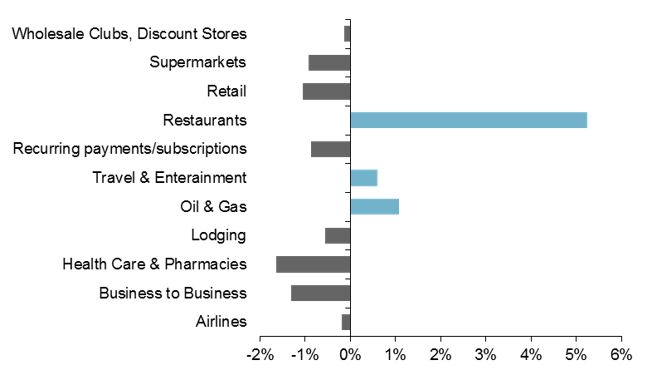

Younger Americans tend to gravitate more toward experiences rather than goods: according to credit card spending data, Millennials and Gen-Z spend more on restaurants, travel and entertainment, and less on retail and supermarkets, than older cohorts. Moreover, membership “perks” – like those associated with a high-end credit card – are welcomed, especially since cash flow can be constrained at younger ages. These two things suggest a heightened interest in advisor-sponsored events, especially in a post-COVID world where many are eager to socialize.

- Being proactive is key, but beware the risk of oversaturation

Young professionals are busy; many are eager to distinguish themselves in their careers with long hours, and even those that aren’t can feel constantly on call, particularly now that working from home has been proven viable. For an advisor, being proactive can be helpful, but there’s a fine line between helpful, actionable insights and what some may consider spam. Communications should be infrequent and punchy – like a newsletter with “best ideas” or thought leadership on current market and macro conditions.

As Millennials and Gen-Z grow wealthier, so too will their financial needs grow more complex. The role of financial advice will, as a result, become of paramount importance. Should the traditional asset management industry hope to best serve this group, successful navigating both early conversations and ongoing relationships will be a key differentiator.

Millennials and Gen Z spend less on goods, more on experiences

Generational differences in credit card spend, 5/31/19 - 3/1/20

Source: J.P. Morgan Asset Management, based on internal Chase data. Data as of March 31, 2020.

Related: How Can I Prepare for a Market Correction?

1 Chase credit card spending data, May 2019 – March 2020.

2 Coldwell Banker, A Look at Wealth 2019: Millennial Millionaires.