Trending

In case you’ve been living under a rock for the past few months, three of the world’s largest and most consequential private companies—SpaceX, Anthropic and OpenAI—are preparing to go public in the same year. Together, they could add nearly $4 trillion in market cap to public markets.

Without getting too dramatic, the last time something happened on this scale, the internet was still in its infancy.

I want to help you think through what this could really mean—for your retirement account, and for the indexes you probably own without realizing it.

Companies Staying Private for Longer

Some of you may remember a time when the initial public offering (IPO) was how companies funded growth. During the dotcom years, firms got listed early, sometimes before they had meaningful revenue, let alone profits. At the peak in 1995-1996, nearly 700 companies a year went public on U.S. exchanges, according to the IPO Initiative at the University of Florida. The median company was about six or seven years old at the time of its IPO.

That world is gone. Private capital markets have deepened significantly over the past two decades, and venture capital has scaled up. Meanwhile, the regulatory burden on public companies has increased.

Together, these forces have pushed companies toward staying private for longer. Annual IPO counts have fallen sharply from those mid-90s peaks, while the median age of companies the time of listing has roughly doubled, to around 12-14 years.

We’re seeing the consequences up close. SpaceX was founded in 2002. Anthropic was founded in 2021 but has grown faster than virtually any company in venture capital history. In other words, they’re mature, scaled businesses, and they’re coming to public markets only now, after private markets have funded years of growth.

For investors, this cuts both ways. On the one hand, the risk of early-stage companies is largely behind you. On the other hand, so is a large portion of the potential upside. The early believers in SpaceX, Anthropic and OpenAI have already made their fortunes.

The Numbers Are Hard to Ignore

Let’s briefly take a look at what’s actually on the table with SpaceX and Anthropic.

SpaceX is targeting a $1.75 trillion valuation in an IPO priced at $135 per share. It’s aiming to raise $75 billion, the largest public offering in history.

Before slamming this as unjustified, consider that SpaceX launched 83% of all mass sent into orbit last year. Its Starlink satellite broadband service now has over 12 million paid subscribers. According to the company, Starlink’s cumulative network capacity has grown from essentially zero in 2019 to over 600 terabits per second today, with the sharpest acceleration coming in the last 18 months.

As for SpaceX’s AI division, Goldman Sachs, the IPO’s lead underwriter, is projecting that it will grow roughly 100-fold by 2030, from $3.2 billion to $322 billion. I’d treat that figure as aspirational rather than a forecast, but it tells you what the pitch is based on.

Anthropic’s story may be even more remarkable in terms of velocity. The San Francisco-based company’s annualized revenue was $4 billion last July, and by year-end, it was $9 billion. By May of this year, it crossed a jaw-dropping $47 billion.

Its valuation, at $965 billion following its most recent round of funding, now exceeds OpenAI’s $852 billion. And according to Ramp, which tracks business payment data across tens of thousands of U.S. companies, Anthropic’s Claude passed OpenAI’s ChatGPT in business adoption for the first time in April. Over 34% of businesses said they subscribed to Claude, compared to 32% for OpenAI.

So why is the company seeking to go public? Anthropic President Daniela Amodei put it bluntly at a tech conference this week: training AI models is “a very capital-intensive business,” and public markets are “very well-suited” to funding that kind of long-cycle investment.

The Potential Index Problem

Most Americans who are saving for retirement are doing so through broad index funds. If you’re reading this, you’re likely one of them. These products are passive by design, meaning they own what the index tells them to own.

That works mostly smoothly when companies enter the index gradually, at sizes that don’t move the needle too much. SpaceX entering at $1.75 trillion is a different matter altogether.

The Nasdaq responded by creating a “fast entry” pathway, allowing companies that rank among the top 40 of its 100 constituents by market cap to get added sooner. Under that provision, SpaceX is expected to be in the Nasdaq 100 just 15 trading days after its June 12 IPO. That means every fund tracking that index will be forced to buy SpaceX. And to fund those purchases, they will have to trim existing positions in Apple, Microsoft, Nvidia and the rest.

The S&P 500 took a different path. S&P Dow Jones Indices announced it would not change its rules to fast-track mega-cap IPOs. Under existing methodology, SpaceX doesn’t qualify, as it hasn’t been public for 12 months, and it reported a $4.28 billion loss in the first quarter of this year. That keeps the company out of the S&P 500 for at least a year. So unlike QQQ investors, SPY investors won’t automatically own it, at least not now.

The broader point I’m making is that these massive listings create structural dislocations that are otherwise invisible to most investors. Capital will be reallocated to fund new positions. Rebalancing trades will move prices. And when lockup periods expire—typically 120 to 180 days after the IPO, though SpaceX may follow a staggered approach—there will be additional selling pressure as insiders access liquidity.

None of this makes these IPOs inherently bad investments. It just means the post-IPO price action will be more complex than a simple “up or down” read on the company’s fundamentals.

What History Says About IPO Returns

I don’t want to dissuade you from buying SpaceX or Anthropic when they list. But I’ve witnessed a lot of IPO cycles over my decadeslong career, and there are some risks you should be aware of.

Thomas Shipp, LPL Financial’s Head of Equity Research, looked at roughly 1,500 IPOs from April 1995 through April 2025 on the NYSE and Nasdaq and found that the average one-year return from the first day’s close was 10.5%. That sounds decent until you account for the extreme skew in that number.

When Shipp stripped out the occasional extraordinary winner, the median return fell to negative 4.7%.

Not only that, but around 60% of the companies in Shipp’s sample delivered zero or negative returns over the three years following their IPO. Only around 40% outperformed the S&P 500 in year one.

Also consider that the companies bringing these IPOs to market, and the investment banks underwriting them, have every incentive to price them at the upper bound of what investors will pay. The runway for publicly-funded growth has to justify the valuation already baked in the price.

For SpaceX specifically, that means believing not just in Starlink’s subscriber trajectory—which is genuinely impressive—but also in technologies that don’t exist yet, such as orbital data centers and Mars colonization. I look forward to seeing Elon Musk execute on two these fronts, but for now, the timeline is up in the air.

What we’re living through is a once-in-a-generation transfer of private market wealth into public markets.

The companies that have defined the last decade of technological progress—satellite communications, artificial intelligence, space infrastructure—are finally arriving on exchanges where ordinary investors can own them. If you’re thinking of participating, I hope you approach them the way you would any concentrated, high-conviction bet.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was EasyJet, up 17.2%. According to Morgan Stanley, Frontier indicated that 2–3 points of its 20%+ second quarter revenue per available seat mile (RASM) outlook are tied to Spirit’s exit, while the longer-term benefit could reach 3–5 points of RASM uplift on a go-forward basis, though given the strength since the bankruptcy, it is possible the eventual revenue benefit exceeds these expectations. Prior to Spirit’s bankruptcy, Frontier overlapped with Spirit on 30% of its network, and management noted markets abandoned by Spirit have often seen RASM improve 15–20 points rather quickly.

- The Shanghai Containerized Freight Index was higher by 15.9% week-over-week (WoW) for the week. Rates on European, Mediterranean, U.S. West, and U.S. East routes changed +29.9%, +16.9%, +31.5%, and +23.6% WoW, respectively, according to Morgan Stanley.

- Airbus deliveries have accelerated meaningfully in recent weeks, with May estimated at 70 aircraft, marking a clear inflection after a softer first quarter. Based on the gap between first flights and deliveries, Bank of America estimates a buffer of 25 aircraft that are ready for handover, which should underpin a further step-up in June.

Weaknesses

- The worst-performing airline stock for the week was Norwegian Air Shuttle, down 13.5%. TAP Air Portugal is canceling up to 300 flights and operating only 79 minimum-service flights. Recovery from a 500-flight cancellation day does not happen instantly. Aircraft and crews can end up out of position, which means June 4 and 5 may still see ripple delays, according to Morgan Stanley.

- May crude seaborne volume declined 5% month-over-month (MoM), implying delayed import demand potentially awaiting a reopening of the Strait of Hormuz. The reduction in global crude inventory may indicate better demand upon a reopening of the Strait, according to Goldman.

- Cebu Air may face near-term earnings pressure from elevated jet fuel prices and weaker seat load factors, with losses expected in 2Q26–3Q26 before a recovery in 1Q27 as fuel costs ease, according to CLSA.

Opportunities

- According to UBS, easyJet responded to the announcement by Castlelake that it is in the early stages of considering a possible offer for easyJet. The easyJet board believes the offer is opportunistic given the current situation in the Middle East and sees considerable regulatory, financial, and other execution challenges with a potential takeover.

- By analyzing high-frequency cargo transportation data, Goldman believes container shipping rates may see near-term upside risk from an earlier-than-usual peak season, driven by retailers’ inflation concerns and restocking amid a record-low inventory-to-sales ratio in the U.S., as well as reduced effective capacity from slower vessels and port congestion caused by weather and a surge in container volumes.

- According to Bank of America, Singapore Air has more than 45% of capacity on Australia and Europe routes, where pricing power appears strongest given lingering Gulf airline disruptions. The airline is also well positioned to gain market share on Europe routes, as shifts from risk-averse and time-sensitive travelers are likely to persist for some time, even if the war ends.

Threats

- Third quarter 2026 domestic capacity growth was reduced by another 40 basis points (bps) this week to +0.4%, as American Airlines led reductions. American reduced its 3Q26 domestic growth to +5.4%, down from +7.5% last week and +9.3% two weeks ago. Since early April, American has now reduced 3Q26 domestic growth by 690bps, the most among carriers, according to Bank of America.

- This past week, laden vessels from China to the U.S. were down sequentially (-13% WoW) and up on a year-over-year basis (+17% YoY), according to Goldman.

- UAE flag carrier Emirates has cut almost 500,000 seats from its June schedule as it rebuilds operations disrupted by the Iran conflict. The Dubai-based airline has reduced its June schedule by almost 16%, with daily outbound flights falling from 237 to 200, down 14% from June 2025, according to data from aviation analytics company Cirium.

Luxury Goods and International Markets

Strengths

- Victoria’s Secret shares surged by nearly 50% after the company reported much stronger-than-expected first-quarter results and raised its full-year sales and profit forecasts. Investors were encouraged by 15% sales growth, strong demand for core products, improving profitability, and management’s confidence that the turnaround strategy is gaining momentum.

- Recent services PMI data highlight resilient demand in the world’s two largest economies, the United States and China. May readings remained comfortably above the 50 threshold, with the U.S. Services PMI rising to 54.5 and the RatingDog China General Services PMI reaching 54.4. These expansionary readings suggest continued strength in service-sector activity and are consistent with healthy consumer spending on travel, leisure, dining, and other discretionary services.

- Shinsegae, a South Korean department store operator, was the best-performing stock in the S&P Global Luxury Index over the past five trading days, with shares surging more than 20%. Investors have grown more optimistic that South Korea’s strong equity market performance and rising real estate prices will boost luxury spending among affluent consumers, benefiting Shinsegae’s department store and duty-free businesses. Analysts have also raised expectations for the company’s earnings growth.

Weaknesses

- Swiss watch exports fell 16.6% year-over-year in April, driven by a 56% drop in U.S. shipments following a tariff-related surge a year earlier. Excluding the U.S., exports rose 3% and were up 1.7% year-to-date. The Middle East weakened, with exports to the UAE, Saudi Arabia, and Qatar down 9.5%, 17.3%, and 12%, respectively. Watches priced above CHF 3,000 saw the steepest decline, falling 19%.

- The Eurozone services PMI remained below the 50 threshold, signaling continued contraction in the services sector and highlighting the region’s fragile economic backdrop. Persistent weakness in business activity suggests that demand remains subdued.

- Lucid Group, an EV car maker, was the worst-performing stock in the S&P Global Luxury Index, with its shares falling 22% over the past five trading days. Investors remain concerned about the company’s large losses, heavy cash burn, and the possibility that it may need to raise additional capital in the future. Recent earnings showed weaker-than-expected revenue and deliveries, leading investors to question how quickly Lucid can become profitable.

Opportunities

- The 2026 FIFA World Cup begins next week on June 11 and will be the largest World Cup in history, featuring 48 national teams competing across the United States, Canada, and Mexico. The tournament is expected to drive a meaningful increase in travel, hospitality, and consumer discretionary spending as millions of fans travel to attend matches, book hotels, dine at restaurants, and purchase merchandise.

- First-quarter results suggest that China’s affluent consumers are beginning to spend more again, supported by improving equity markets and stronger consumer sentiment. According to data from Chinese analytics firm BigOne Lab, Louis Vuitton and Burberry returned to sales growth in mainland China during the quarter, while Kering, owner of Gucci, reported smaller declines, and Tapestry, best known for Coach, continued to gain momentum. The data also indicated that discounting activity is moderating, which may signal improving demand and a greater willingness among consumers to spend.

- Tesla is expected to begin Optimus humanoid robot production in late 2026 at its Fremont, California factory, with management targeting annual output of up to one million units. The company is also building a dedicated manufacturing facility in Texas that could eventually support production capacity of as many as 10 million robots per year. Initial deliveries are expected to begin in October next year. According to Andres Sheppard of Cantor Fitzgerald, Tesla could produce approximately 2,700 Optimus robots in the first year, with production ramping to roughly 18,000 units by 2029.

Threats

- According to Morgan Stanley’s research team, China’s housing market remains weak, with conditions deteriorating further year-over-year in May. The weak property market continues to be a concern for the European luxury sector. While Chinese households have diversified into financial assets in recent years, real estate remains a key component of household wealth and an important driver of consumer confidence. Continued weakness in the property market could therefore weigh on discretionary spending and luxury demand.

- U.S. economic growth slowed, with first-quarter GDP revised down to 1.6% and growth expected to ease to 1.8% by 2027. Higher oil prices are pushing up costs and inflation, prompting some companies to pause hiring. Consumer spending remains strong for now, but analysts expect it to slow as savings are depleted and lower-income households feel the impact of rising energy costs.

- Bloomberg consensus expects Eurozone GDP growth of just 0.1% quarter-over-quarter and 0.8% year-over-year in the first quarter of 2026, highlighting a weak domestic growth environment. Bloomberg surveys also point to European Central Bank policy rates of 2.25% for the deposit facility and 2.40% for the main refinancing rate. The combination of sluggish growth and elevated interest rates could weigh on consumer confidence and discretionary spending. Data will be released next week.

Energy and Natural Resources

Strengths

- The best-performing commodity for the week was WTI crude oil, up roughly 4%. Crude regained ground as a second round of U.S.–Iran peace talks failed to produce a durable breakthrough, leaving the Strait of Hormuz — normally a conduit for about 20% of global oil and gas flows — only partially open, with tanker traffic well below pre-conflict levels.

- Copper continues its rise, as it is prized for its high electrical and thermal conductivity, making it a critical input for data center infrastructure, power generation, and electrical wiring. Its demand is closely tied to construction and electrification trends, which can make prices sensitive to shifts in industrial and infrastructure spending. However, we note reasons for caution, including recent comments on cost efficiencies from Jensen Huang.

- Trafigura made a record payout to top traders and executives — over $3 billion in dividends for the half year, its largest half-year payout on record — after first-half profit more than doubled to $4.09 billion, its third-best half ever. Total balance sheet assets rose 40% to $111 billion as the Strait of Hormuz disruption inflated cargo values, though CEO Richard Holtum noted much of the profit was booked before the war began.

Weaknesses

- The worst-performing commodity of the week was lithium, declining approximately 8.79%. BloombergNEF’s New Energy Outlook 2026 reinforced a structurally bearish demand backdrop for the U.S. battery market, projecting that China and India will dominate global energy storage over the next two decades, while U.S. installed capacity grows only threefold by mid-century—held back by policies that make it more difficult for utility-scale developers to secure tax credits and subsidies for lower-cost Chinese batteries. With global storage forecast to increase 17-fold to 3.8 terawatts by 2050 from 223 gigawatts in 2025, demand concentration in Asia—where Chinese manufacturers like CATL and BYD hold a commanding lead—undercuts the investment case for Western-aligned lithium supply chains, according to BloombergNEF.

- North American natural gas remained a laggard within the energy complex, with Henry Hub drifting to around $2.80–$3.16/MMBtu despite acute global LNG tightness. Well-supplied domestic storage, rising Permian associated gas, and limited near-term export capacity have decoupled U.S. prices from international markets, where reduced Strait of Hormuz flows keep landed LNG elevated. The wide domestic-to-international spread underscores how the U.S. lacks sufficient liquefaction capacity to monetize the global shortfall in the near term.

- Coal supply chains showed fresh fragility as Glencore’s Cerrejón mine in Colombia—one of the world’s largest open-pit thermal coal operations—declared force majeure on June 1 and suspended mining, rail, and port operations after a community blockade cut off shipments and fuel. Cerrejón has now faced nearly 80 blockades this year following 333 in 2024, and Colombian national output has already fallen to a two-decade low of 53.9 million tonnes in 2025 amid a new export tax and soft thermal coal markets, deepening pressure on an export-dependent producer.

Opportunities

- Grid modernization and gas turbine capacity remain a multi-year investment theme as AI and data center demand collides with aging infrastructure. JPMorgan has flagged the aging U.S. grid as a “national security risk” and sees roughly $5.8 trillion of global grid spending through 2035, while equipment bottlenecks persist among turbine manufacturers. In India, the strain is already visible: power generators have quadrupled natural gas purchases on the Indian Gas Exchange to meet record heatwave-driven demand, buying 4.5 trillion BTU between April 1 and May 26—an almost 350% year-over-year increase—reinforcing the structural case for power generation, storage, and transmission buildout.

- Critical minerals supply chain diversification continues to attract project-level capital and policy support. The Democratic Republic of Congo—the largest global producer of tantalum—added lithium, tantalum, niobium, tungsten, uranium, and rare earths to its “strategic minerals” list by decree, raising royalties on those metals to 10% from the usual 3.5%, a move that could increase fiscal revenue but also pressure project economics. The reclassification underscores resource-holder leverage and the premium placed on securing non-China supply of battery and defense-related inputs.

- Suzlon Energy is expanding beyond wind turbines into round-the-clock clean energy parks that integrate solar, wind, and batteries, offering full lifecycle project design, construction, and maintenance. The company also plans to build a battery storage manufacturing facility by next year. Vice Chairman Girish Tanti said the firm aims to quadruple its managed energy assets to 70 gigawatts within five years, positioning storage-backed, dispatchable renewables as a response to India’s energy security pressures amid the Middle East conflict.

Threats

- The fragile U.S.–Iran ceasefire remains the dominant tail risk for the entire complex. With the Strait of Hormuz only partially reopened, talks stalled, and Israeli operations in Lebanon clouding the truce, any renewed escalation threatens to disrupt roughly a fifth of global crude and LNG flows—and, by extension, the fertilizer, sulfur, and refined product supply chains that transit the strait. The EIA still expects Brent to average around $106/b through June before Middle East output recovers, but the range of outcomes remains wide and highly headline-driven.

- Renewable integration is forcing some grids backward toward older, higher-emission generation. India’s largest power producer, NTPC Ltd., is considering reviving older sub-critical coal plants (maximum 250 MW, able to run as low as 25% of capacity) because modern ultra-supercritical units degrade more quickly when cycled below full load. This paradox—using older coal as a flexibility tool to absorb solar—highlights how insufficient hydropower, gas, and battery storage capacity is slowing the clean energy transition and risks locking in higher-emission baseload generation where storage economics remain challenged.

- NVIDIA’s shift to 800-volt power architecture allows the same wire gauge to carry roughly 157% more power, and CEO Jensen Huang’s “optics where you must, copper where you can” approach signals the industry is actively engineering copper out of data centers—challenging the view that AI buildouts will drive a sustained copper supercycle. With high-bandwidth links above 400 Gbps driving a shift to fiber and silicon photonics, alongside grid constraints, deployment delays, and overstated capacity projections, S&P’s forecast of data center copper demand rising from 1.1Mt in 2025 to 2.5Mt by 2040 may overstate assumptions tied to copper-intensive infrastructure.

Bitcoin and Digital Assets

Strengths

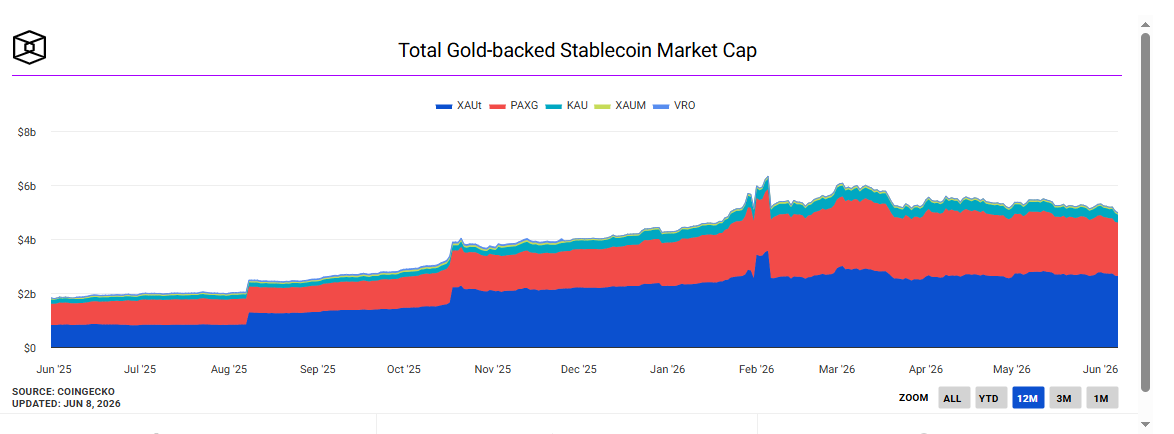

- Tether announced the launch of a Visa card that rewards users with XAUT, its gold-backed digital asset with a market capitalization of approximately $2.6 billion. The card allows users to spend fiat globally while earning up to 6% cashback in tokenized gold and automatically investing spare change into XAUT. Backed by roughly 24 tons of physical gold, the initiative expands the real-world utility of digital assets and highlights growing efforts to integrate tokenized commodities into everyday payment systems.

- Visa partnered with Brale to test institutional settlement using SBC, a U.S. dollar-backed stablecoin, on the Canton Network. The initiative is designed to evaluate how blockchain technology can support faster, programmable, and privacy-enabled payment settlement for financial institutions. Visa’s stablecoin settlement program reached a $7 billion annualized run rate as of April, up 50% from the previous quarter, highlighting the growing role of stablecoins as a next-generation payment and settlement infrastructure.

- Coinbase and Better Home & Finance announced plans to allow qualified borrowers to use Bitcoin and USDC as collateral for mortgage downpayments beginning this summer. The initiative, which supports Fannie Mae-backed mortgages, marks another step toward integrating digital assets into traditional financial services. By enabling homebuyers to leverage their crypto holdings without first converting them into cash, the program highlights the growing acceptance of digital assets within the U.S. housing and mortgage markets.

Weaknesses

- Professional investors significantly reduced their exposure to U.S. spot Bitcoin ETFs during the first quarter as market conditions weakened. According to CoinShares, holdings reported through regulatory filings fell from 313,000 BTC to 261,000 BTC, representing a decline of approximately 52,000 BTC. The reduction was driven primarily by hedge funds and brokerages, which cut their positions by 39% and 53%, respectively. The data suggests that trading-oriented institutions pulled back from the market as Bitcoin’s downturn intensified, contributing to selling pressure across the digital asset sector.

- Bitcoin faced mounting pressure this week as weakening investor sentiment triggered nearly $1.5 billion in crypto liquidations over a 24-hour period, the largest wave of forced deleveraging since February. At the same time, U.S. spot Bitcoin ETFs extended their record redemption streak to 11 consecutive days, with approximately $3.5 billion in net outflows. The decline in institutional demand, combined with heightened geopolitical uncertainty and Strategy’s first Bitcoin sale since 2022, has weighed heavily on market confidence and contributed to Bitcoin’s slide to a two-month low.

- The cryptocurrency market experienced its weakest week since July 2024, with Bitcoin and Ether posting double-digit declines as investor activity continued to slow. According to CryptoQuant, spot trading volume fell to approximately $679 billion in April, its lowest monthly level since October 2023, signaling weaker demand across digital asset markets. The decline was accompanied by broad deleveraging, rising liquidations, and reduced institutional risk appetite, highlighting the challenging environment facing the crypto sector.

Opportunities

- Goldman Sachs partnered with Apex Group, Archax, Ownera, and LRC Group to launch a blockchain-native real estate fund, marking another step forward in the institutional adoption of tokenized real-world assets (RWAs). The fund leverages Goldman Sachs’ GS DAP blockchain platform to tokenize fund shares while maintaining traditional governance and regulatory oversight. The initiative highlights growing interest from major financial institutions in using blockchain technology to improve efficiency, transparency, and future transferability of traditionally illiquid assets such as real estate.

- Ether.fi, a leading Ethereum staking platform, allocated $100 million to a new real-world asset (RWA) vault developed with Plume, a blockchain platform focused on bringing traditional financial assets on-chain, providing users access to yield generated from tokenized traditional financial assets. The move reflects growing investor demand for more stable, institutional-grade income opportunities on blockchain networks. The vault offers exposure to diversified assets, including investment-grade credit, collateralized loan obligations, and bond exchange-traded funds, highlighting how tokenization is expanding access to financial products that were traditionally available only to institutional investors.

- Travala, a crypto-native travel platform backed by Binance, launched an AI-powered travel protocol that enables autonomous software agents to search, book, and pay for travel services using USDC on Coinbase’s Base blockchain. The system combines artificial intelligence with low-cost blockchain payments, allowing transactions to settle almost instantly with fees of approximately $0.01. The launch highlights the growing potential for stablecoins and AI agents to support real-world commerce beyond traditional crypto use cases.

Threats

- JPMorgan Chase warned that the window to pass the U.S. crypto market structure bill, known as the Clarity Act, is narrowing as lawmakers face a crowded legislative calendar ahead of the midterm elections. The bill, which would establish a comprehensive regulatory framework for digital assets, still faces several hurdles and ongoing disagreements over stablecoin yield provisions. A delay in passage could prolong regulatory uncertainty for crypto companies and investors, potentially slowing institutional adoption and investment in the digital asset sector.

- A coordinated anti-scam operation involving the U.S. Department of Justice and major private-sector firms, including Coinbase, SpaceX, Meta Platforms, Google, Microsoft, and Apple, led to the freezing of more than $3.8 million in cryptocurrency, the disabling of 1.4 million accounts, and dozens of arrests linked to fraud networks operating in Southeast Asia. Despite these enforcement efforts, cryptocurrency investment fraud remains a growing challenge, with reported losses exceeding $7.2 billion in 2025, up 24% from 2024, according to FBI data. The persistence of large-scale scam operations continues to pose risks to investor confidence and the broader adoption of digital assets.

- Weaker-than-expected U.S. economic data increased concerns that the Federal Reserve could keep interest rates elevated for longer than anticipated. The U.S. economy added 172,000 jobs in May, nearly double economists’ expectations, while the 10-year Treasury yield rose to 4.52% following the report. Higher interest rates typically reduce investor appetite for risk assets, creating additional headwinds for cryptocurrencies and other speculative investments.

Defense and Cybersecurity

Strengths

- At Computex 2026, Nvidia CEO Jensen Huang explicitly named Marvell Technology as “the next trillion-dollar company,” sparking a 60% weekly rally driven by strong demand for AI connectivity hardware. This momentum is further supported by Wall Street expectations that Marvell could be added to the S&P 500 during the latest quarterly rebalancing. Capping off the week, Marvell reported strong Q1 earnings and launched its Teralynx 100 terabit switch, challenging Broadcom’s position in the market.

- KBR secured an $8 billion contract from the U.S. National Science Foundation to manage operations for the U.S. Antarctic Program, marking a significant government services award.

- RTX secured a $515.82 million contract modification for its AN/SPY-6 air and missile defense radar system, supporting the U.S. Navy and the German government, with work scheduled through May 2027.

Weaknesses

- A whistleblower lawsuit alleges that IBM and AT&T covered up cybersecurity breaches affecting systems used by the U.S. military. The case remains active in federal court.

- A weak revenue outlook from Broadcom triggered a sharp sell-off in semiconductor stocks, as investors reacted to softer third-quarter guidance and ongoing geopolitical concerns involving the U.S. and Iran.

- Satellite imagery has revealed that China is building a network of more than 80 concrete launch pads, bunkers, and communication hubs near its Hami nuclear missile silo field in Xinjiang. Analysts reviewing the data, provided by Colorado-based spatial intelligence firm Vantor to Reuters, say this infrastructure could support mobile missile launchers and command operations, potentially strengthening Beijing’s retaliatory nuclear strike capabilities.

Opportunities

- Nvidia announced the acquisition of Kumo AI, a specialist in highly accurate predictive AI software, to strengthen its AI capabilities and broaden its enterprise solutions portfolio.

- The newly drafted U.S. defense bill preserves the $1.0 billion base funding request for the Pentagon’s high-priority Defense Autonomous Warfare Group (DAWG). However, an additional $53.6 billion in advanced research funding remains tied up in unresolved legislative reconciliation bills, creating execution uncertainty for tier-one autonomous drone manufacturers.

- Nutanix’s Unified Storage receiving Nvidia-Certified status enhances its position in the AI infrastructure market and supports potential growth, while Microsoft is addressing a critical Windows Server vulnerability that requires immediate patching to prevent remote code execution threats.

Threats

- The breakdown of recent peace initiatives following Putin’s refusal to hold direct talks has contributed to an escalation in the Russia–Ukraine conflict, reinforcing expectations of a prolonged, attritional war and sustained defense spending. At the same time, Western immigration policies have tightened, with European authorities restricting protections for military-aged migrants and the U.S. increasing administrative hurdles for Ukrainian refugees, adding broader humanitarian and policy pressure to the conflict backdrop.

- Lockheed Martin’s receipt of $43.8 billion in new U.S. government contracts has raised some concerns around potential conflicts of interest linked to political donations, adding a layer of oversight risk for defense contractors.

- WIRED reported on hidden code in Meta’s AI app called “NameTag,” designed to detect faces and convert them into biometric profiles via smart glasses. While Meta describes it as an internal test to help users remember people they meet, privacy advocates have raised concerns about potential real-time surveillance implications.

Gold Market

This week gold futures closed the week at $4,338.30, down $254.70 per ounce, or 5.55%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 10.51%. The S&P/TSX Venture Index came off 5.36%. The U.S. Trade-Weighted Dollar rose 1.14%.

Strengths

-

The best-performing precious metal for the week was gold, declining the least, off 5.55%. Barrick Mining is exploring strategic moves on multiple fronts, including a potential London listing of its African business via an all-share deal with Endeavour Mining, while also conducting a formal review of security and procurement plans for its Reko Diq copper-gold project in Pakistan. Analyst valuations of the African assets range widely from roughly $14 billion to $33 billion, and lenders have expressed confidence in Reko Diq’s existing security protocols as new financiers show interest in joining, with the market pricing in renewed optimism.

- India’s central bank said a report that it is selling gold is “not correct,” pointing to data showing its physical gold stock has remained unchanged. Latest figures in the Reserve Bank of India’s Monthly Bulletin show physical gold holdings were steady at 880.52 metric tons as of April. The central bank reiterated the level in a statement on Wednesday, according to Bloomberg.

- The 140-year-old Idaho-based silver producer Sunshine Silver Mining & Refining IPO’d this week, raising $270 million at a $1.9 billion valuation. Proceeds will fund feasibility studies, equipment, and exploration to restart the long-dormant mine, with production targeted for 2028 to lift U.S. silver output by over 15%. The deal comes amid one of the strongest IPO markets in years and silver trading near $73 per ounce, still more than double year-ago levels despite a pullback of more than 30% from January’s all-time high. The company is also exploring antimony processing, a defense-critical byproduct currently dominated by China.

Weaknesses

- The worst-performing precious metal for the week was silver, down 10.47%. Markets are increasingly pricing in a potential Federal Reserve rate hike later in 2026, with strong jobs data and inflation running near 3.8% prompting economists at firms like BNP Paribas to forecast tightening as early as December. Auto demand could weaken amid declining consumer confidence and higher rates, although some consumers may opt for an EV for their next vehicle purchase given rising gasoline prices.

- London-listed shares in Pan African Resources slid to their lowest intraday level since March after the precious metals miner projected full-year production at the lower end of its guidance range. The firm expects record half-year gold production of 147,000 ounces, bringing full-year output to 275,000 ounces, at the low end of its 275,000 to 292,000-ounce guidance range, according to Bloomberg.

- Gold declined as investors began another week without a clear path to a Middle East peace deal that could reopen the Strait of Hormuz and ease inflation concerns. Bullion traded lower on Friday after U.S. nonfarm payrolls rose by 172,000, nearly double the consensus estimate of 88,000. Leisure led employment gains, while government hiring posted the largest percentage increase. The 2-year Treasury yield rose 16 basis points to 4.16%, and gold fell roughly 3.5% on expectations that the Federal Reserve may be more likely to raise rates later in the year if inflation remains elevated.

Opportunities

- According to Reuters, Barrick is weighing a possible listing for its African business and is considering a potential all-share transaction with Endeavour as one exit option. The discussions are at an early stage and no decision has yet been taken. Barrick could retain its Toronto listing while owning shares in both a North America-listed entity in New York and a separate Africa-focused company listed in London.

- Ray Dalio said the United States has crossed a debt threshold from which it cannot return, and that the Federal Reserve may soon be forced into a 1930s-style policy of holding interest rates artificially low. Speaking at the Forbes Iconoclast Summit, the Bridgewater Associates founder told Bloomberg’s Dani Burger that $7 trillion in federal spending against $5 trillion in revenue is squeezing the economy “like plaque in the arteries.”

- Northern Star Resources has hinted in a strategic review that its mines in Western Australia’s Yandal region could be sold, as it faces pressure from a prominent activist hedge fund to improve performance or risk being acquired by a larger gold miner, according to the Financial Review.

Threats

- Gold continues to show signs of weakness, with the bias remaining toward further declines following three consecutive monthly losses. The precious metal is being weighed down by elevated bond yields, continued outflows from bullion-backed exchange-traded funds, and speculation that the Federal Reserve will be forced to confront persistently high U.S. inflation, according to Bloomberg.

- Bank of America calculates a weighted average reserve life index of 14.5 years, up from 14.1 years for the same companies in 2024. In their view, the extension in reserve life is primarily driven by lower production levels, with reserve growth playing a smaller but still positive role.

- Precious metals continue to struggle to attract sustained demand as inflation concerns persist, reinforced by a sticky core PCE print last week that has kept Treasury yields elevated. Gold continues to underperform the broader complex, with CFTC futures net length falling to multi-month lows and ETF outflows re-emerging, led by North America and China. Despite strong April gold imports from China and India, signs of demand softness are emerging: Indian dealer discounts widened sharply in May as jewelers avoided restocking, while Chinese premiums narrowed and the Shanghai gold premium to London turned negative, according to BMO.

Related: What a $13.7 Billion Hedge Fund Sees in the Future of AGI Infrastructure