Trending

If I have to type the words “renewed tensions in the Middle East” one more time…anyway, round and round we go.

Revived hostilities with Iran are still sending oil prices dancing on good and bad news. While headlines also lifted Treasury yields, investors mostly focused on positive, and mostly domestic, factors that have driven U.S. markets for most of the year: technology, AI investments, and the second-quarter earnings.

The Nasdaq Composite led the way with a 1.74% gain, while the S&P 500 rose 1.23%. The Dow Jones Industrial Average slipped 0.50%, and the small-cap Russell 2000 fell 0.61%. Within the S&P 500, information technology was the week’s strongest performer, joined by energy and communication services, while health care and materials lagged.

Oil’s grip on market performance is slipping

The biggest news outside of markets came from the strikes launched by both the U.S. and Iran. Escalating military action reignites fears of supply disruptions through the Strait of Hormuz, which sent oil prices sharply higher before the promise of more negotiations helped prices retreat by the end of the week. Geopolitical risks have not disappeared, but the market appears to be tired of this story and seems to be dismissing it more easily than they did earlier this year.

Time and again, this dance of strikes and negotiations has lulled investors into the view that these events are temporary headline risks rather than long-term threats to economic growth. Short of massive escalations, this conflict appears to be destined to simmer for quite a while longer as the global economy attempts to work around it.

While higher oil prices will still pressure inflation expectations and bond yields, it would likely take a much larger and more sustained increase to materially change the outlook for consumers or corporate profits. Slowly strengthening labor market conditions and continued investment in AI infrastructure are providing important support for the U.S. economy.

That changing reaction was evident throughout the week. Despite several sharp swings in oil prices and a series of geopolitical headlines, stocks repeatedly recovered as investors shifted their attention back toward earnings and technology. Investors are bullish right now, and they are craving supporting data to keep it that way. Bad news is only attracting TikTok-length attention spans now that Q2 earnings season is right around the corner.

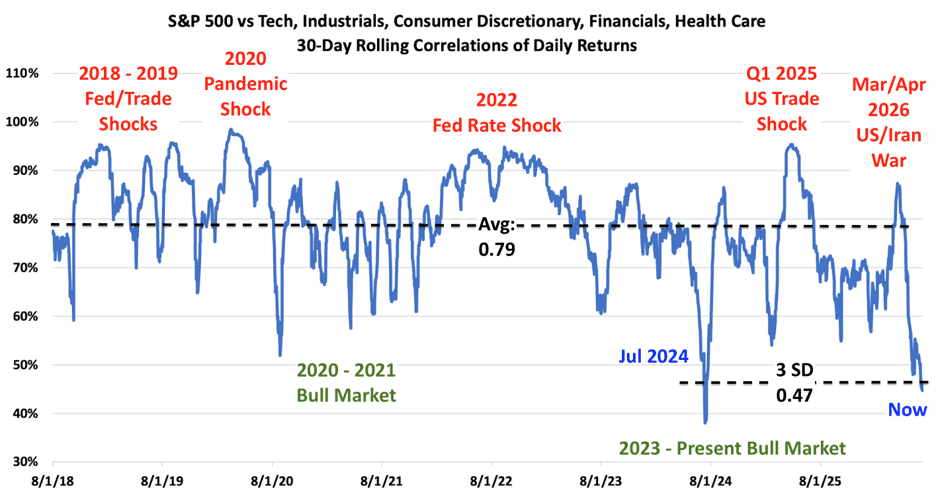

Investors are heavily focused on high-flying sectors in search of performance; Source: DataTrek via Daily Chartbook

Earnings and AI continue to lead

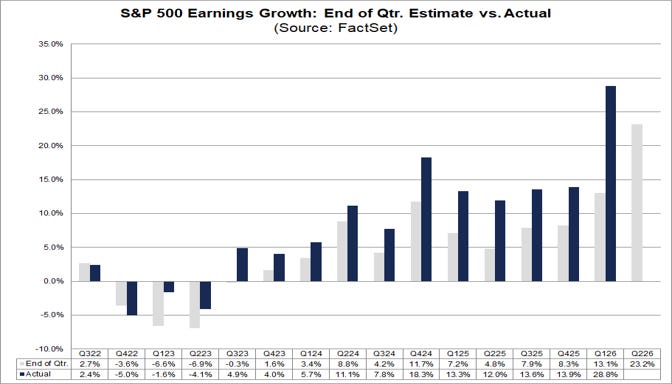

The second quarter earnings season begins next week with reports from major banks before expanding into industrial and technology companies later in the month. Expectations remain high, with technology once again expected to account for much of the market’s earnings growth.

Earnings expectations are very high; Source: FactSet

Past quarters have set the bar high, and the current optimism comes with even higher expectations. AI-related companies continue to report strong demand, but investors have become more selective about how much they are willing to reward. Earnings growth can only grow so fast for so long, and investors in many of the high-fliers know this.

Take Samsung earnings, for example. After reporting a 19x (19x!) jump in profits on memory chip sales, shares fell. The math is cruel here, and investors know that Samsung won’t be able to 19x again.

After an exceptional run, semiconductor stocks have experienced more volatility as markets begin asking whether future returns can keep matching lofty expectations. That does not necessarily mean this is the end of the AI story. The market is simply becoming more focused on profitability and execution rather than simply rewarding companies for increasing AI spending. This is healthy, and it is a good sign because this is not how euphoria behaves.

Outside of technology, investors are looking for broader leadership. Areas such as industrials, communication services, and mid- or small-cap stocks could benefit if market participation expands during the second half of the year, reducing the market’s heavy reliance on a relatively small group of technology leaders.

What this means for investors and what’s next

The coming week could provide several important tests for investors. The second-quarter earnings season begins, while inflation data and retail sales will offer fresh clues about the strength of the economy and the Federal Reserve’s next move.

Treasury yields also remain in focus after the 10-year Treasury yield climbed from roughly 4.49% to 4.56% following the hawkish Fed meeting minutes. Later in the month, we can expect to hear more about the Federal Reserve’s Task Forces, which were announced on Thursday and include some heavy hitters from the U.S. and abroad.

Portfolio Positioning

Strong earnings remain the foundation of the market, but valuations and diversification will become increasingly important as the year progresses. Staying invested while maintaining a balanced portfolio could prove more rewarding than simply chasing this year’s biggest winners into the stratosphere.

AI remains a powerful long-term driver, supported by strong earnings growth and continued investment, yet the sector's impressive gains have also increased concentration risk. Rather than abandoning technology, investors may benefit from broadening their exposure.

Mid-cap companies and industrials stand to benefit from economic growth, on-going infrastructure investment, and onshoring. Communication services also offer another way to participate in the AI theme, with attractive earnings prospects and less demanding valuations than some of the most crowded technology stocks.

If you aren’t already, underweighting fixed income is an opportunistic bet if you have the stomach for the stock market’s volatility. High inflation, fiscal malfeasance, and geopolitical tensions aren’t bullish for bonds. At the same time, conservative investors may be happy with TIPS given the stubborn inflation.