Trending

A strong emergency fund can turn a crisis into a mere inconvenience. This foundation allows you to build all other wealth, which is why it is so important to get it right.

The fallacy of the static emergency fund

One of the biggest enemies of good financial planning is complacency. Checking a box and never thinking about it leaves you open to unexpected surprises when circumstances or financial needs change. This applies as much to investing as it does to everyday personal finance.

Emergency funds are one of these categories, and I see many people caught off guard when they are not adequately prepared for financial difficulties despite meeting the standard definitions of a solid emergency fund. The most common guideline for emergency funds is “aim for between three and six months of essential expenses.”

That begs the question, when is it three and when is it six? There is little solid advice here, although some say that when you have two or more sources of income, then three months is enough, while six months is appropriate if you have less than two sources of income.

This distinction is helpful and does have logic to it. It is far more likely that you could lose one income than two, but this approach still doesn’t go far enough. The “between three and six months of expenses” guideline is simply too general and doesn’t account for either red hot or ice-cold labor markets or lifestyle inflation.

A bad labor market has the potential to challenge even the “healthy” six-month emergency fund, especially when you checked the box on your emergency fund years ago and never re-budgeted your cash allocation based on today’s expenses.

The importance of measuring labor trends

The economy has been through a lot in the 2020s, and the labor market has been a tempest. The speed with which the employment conditions have changed has caught many people (especially in technology positions) off guard over the past few years. This is why an emergency fund needs to align with labor market conditions to truly offer the right protection. When there are wide differences between industries, more granular benchmarks may be needed.

Over the past three years, the median length of unemployment has been rising as the labor market weakened and hiring became scarcer. The median and average length of unemployment now lasts 12 weeks and 26 weeks, respectively. These figures are up from 10 weeks and 21 weeks in January 2023. Even more concerning is that the percentage of unemployed people who have been unemployed for more than 26 weeks (the upper limit for state unemployment benefits) has risen to over 27%, up over 7 percentage points since January 2023.

Someone who holds the same number of months of expenses, or worse the same amount of cash in nominal terms, as they did in 2023 has a less robust safety net than they used to. Between inflation and the weakened labor market, a proper safety net needs to move with the prevailing conditions.

An analytical approach to emergency savings

The purpose of the Emergency Fund Resilience Index (EFRI) is to help zero in on the number of months an emergency fund should last, given the latest conditions in the labor market. Every month the Bureau of Labor Statistics tells us how long it took people to find jobs. The EFRI estimates how long the line is today, and the amount of savings you need to try to comfortably withstand it.

Building an emergency fund that aligns with the estimated search duration for a new job keeps a household nimble and fortified for changing circumstances. The four inputs for this reference index vary in their purpose but together provide a balanced view of both the flow rate of workers into and out of the labor and the total size of the pool of un/underemployed workers.

Flow Rate

-

Initial jobless claims (labor outflow): This measures the velocity of new competition for open jobs. High or increasing claims mean the waiting room of the labor market is getting crowded. If claims are spiking, your search duration increases because businesses are flooded with fresh applicants simultaneously.

-

Hiring rate (labor inflow): This is a critical variable that shows how wide or narrow the entry door to employment has become. If the hiring rate slows, the general wait time within unemployment will lengthen regardless of how rapid layoffs may be.

Overall Pool Size

-

U-6 unemployment (the crowd): The headline unemployment rate (U-3) is not comprehensive enough. U-6 unemployment includes underemployed and discouraged workers. Both unemployed and underemployed workers are possible competition for open positions. High U-6 unemployment, regardless of how low headline U-3 unemployment is, means the crowd is denser than it looks and will add friction to your search.

-

27+ weeks of unemployment (stagnation): When this percentage rises, it signals that employers are becoming pickier and a larger portion of workers are inert and without supplementary income benefits. Odds of an unemployed person becoming “long-term unemployed” (and losing their unemployment benefits) is statistically higher as this figure grows. The more common stagnant unemployment is, the more drastically the size of an emergency fund may need to change.

Taking action

Your emergency fund isn’t a savings account, although you should be using a high-yield savings account to keep the money growing. The real purpose is a bridge between stable income sources. If long-term unemployment is rising and hiring is falling, your bridge literally needs to be longer to reach the other side of unemployment or income losses. If you are building a 3-month bridge for a 6-month chasm, you aren’t safe, you’re just prolonging a fall.

Building an emergency fund is a process and if you find that you’re underprepared, start putting a plan in place to top it up. You may not be able to do it immediately, but shifting money from other purposes, or making periodic payments into the fund can put you back on track.

As the labor market improves, this money could travel in the other direction. One benefit of this approach is that you can avoid “over-insurance” against financial emergencies. Excess money can be put to work on more productive investments.

There is still a baseline level of savings that everyone should keep, but in a tight labor market, the risk of a lengthy income gap shrinks and therefore so could your layer of protection.

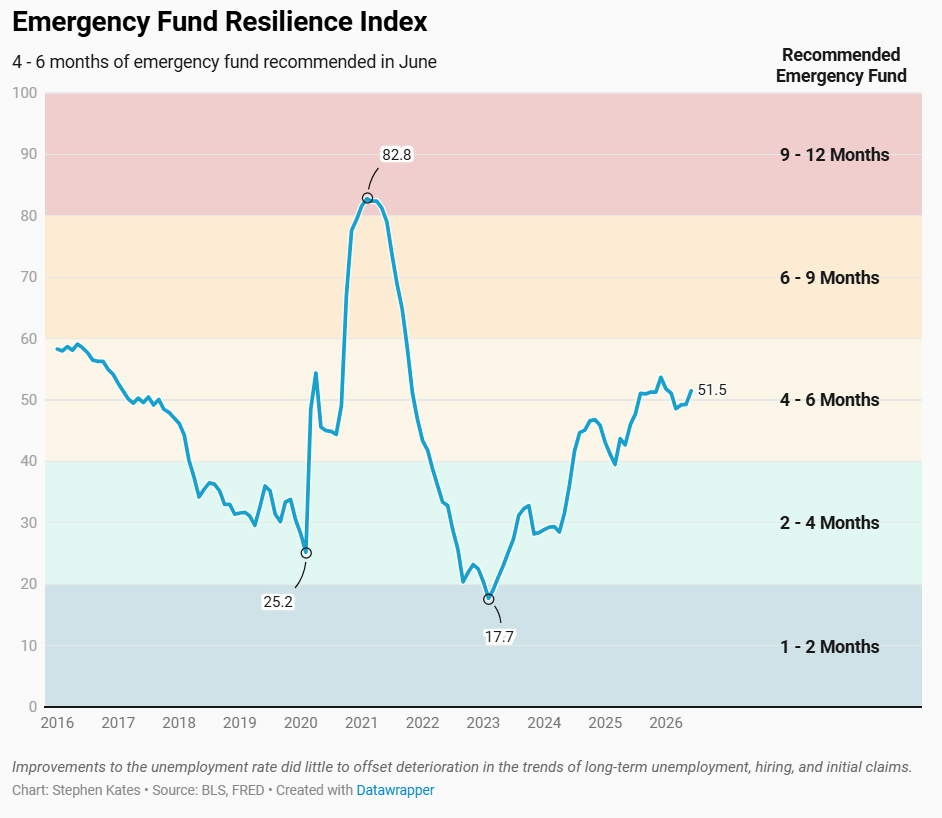

Emergency Fund Resilience Index (June): 51.5

The recent labor market reports offer mixed signals for the health of the labor market, but little good news for unemployed job seekers. Businesses continued adding jobs, but fewer people participated in the workforce. The employment-to-population ratio slipped, which is why the unemployment rate fell despite persistently weak hiring.

Most concerningly, the number of people unemployed for more than six months has persistently risen over the past year. None of these signals point to an imminent downturn, but together they point to a labor market that is less forgiving than it was a year ago.

The Emergency Fund Resilience Index (EFRI) rose 2.2 points to 51.5 in June. Although the U-6 unemployment rate has improved, it did little to offset the high share of long-term (27+ weeks) unemployed, higher initial jobless claims, and the weak hiring rate.

There are few historical months that show a worse hiring rate than right now. May’s most recent hiring rate from the JOLTS report is equal to that of April 2020 and mirrors the environment of early 2010. Neither were hiring environments we want to emulate.

An output of 51.5 is squarely in the 4-6 month emergency fund recommendation range. Although layoffs and overall unemployment are low, the hiring rate is punishingly low. For workers in industries with traditionally long hiring cycles or an already competitive hiring environment such as professional services or information, the upper end of this range is highly recommended.