Trending

Recent months have tested even the most patient luxury sector investors. Concerns over tariffs, currency fluctuations and a slower-than-hoped-for Chinese recovery have weighed on stocks.

However, I believe the luxury sector is merely catching its breath after an exhilarating post-pandemic surge. Investors who understand the long-term fundamentals of this market should see today’s pause not as a warning sign but an opportunity.

The Luxury Lull Could Be Coming to an End

The global luxury industry has been one of the most impressive wealth-creation engines of the past two decades. According to Kantar’s BrandZ report for 2025, the value of the luxury category has grown an astounding 477% since 2006, driven by pricing power and scarcity. Unlike fast fashion or tech gadgets that depreciate the moment they’re unboxed, luxury goods have held—and have increased—their value over time.

Iconic companies such as LVMH, Hermès and Richemont have spent decades cultivating heritage and desirability. Across generations, luxury consumption has signaled success and good taste.

Demand in Western economies might be moderating, but global wealth continues to expand. From the U.S. to China, India and the Middle East, the number of high-net-worth individuals (HNWIs) keeps growing.

So why the current lull? According to Morningstar’s Jelena Sokolova and Swetlana Menshchikova, it appears to be a cyclical cooldown following the post-COVID spending binge. Consumers who splurged on handbags, watches and travel experiences in 2021 through 2023 are now being more selective. But as Sokolova and Menshchikova point out, this pause could be temporary.

Awaiting the Return of Chinese Travelers

The single most important catalyst for luxury’s next wave could very well be the return of Chinese travelers.

Before the pandemic, Chinese consumers accounted for roughly one-third of global luxury spending. Their absence over the past few years has left a noticeable void, but that could be starting to change.

According to Dragon Trail Research, outbound travel from mainland China is on track to reach 155 million trips by the end of this year, nearly matching the pre-pandemic record. International flight capacity has recovered to about 90% of 2019 levels, and there are now 160 million valid Chinese passports in circulation, or around 11% of the population. Almost every Chinese traveler shops while abroad, with nearly half spending at least $700 on gifts, Dragon Trail found.

Bloomberg recently reported that Chinese households are sitting on $23 trillion in savings. As real estate prices stabilize and confidence returns, some of that mountain of cash is expected to be unleashed on travel, experiences and, yes, luxury goods.

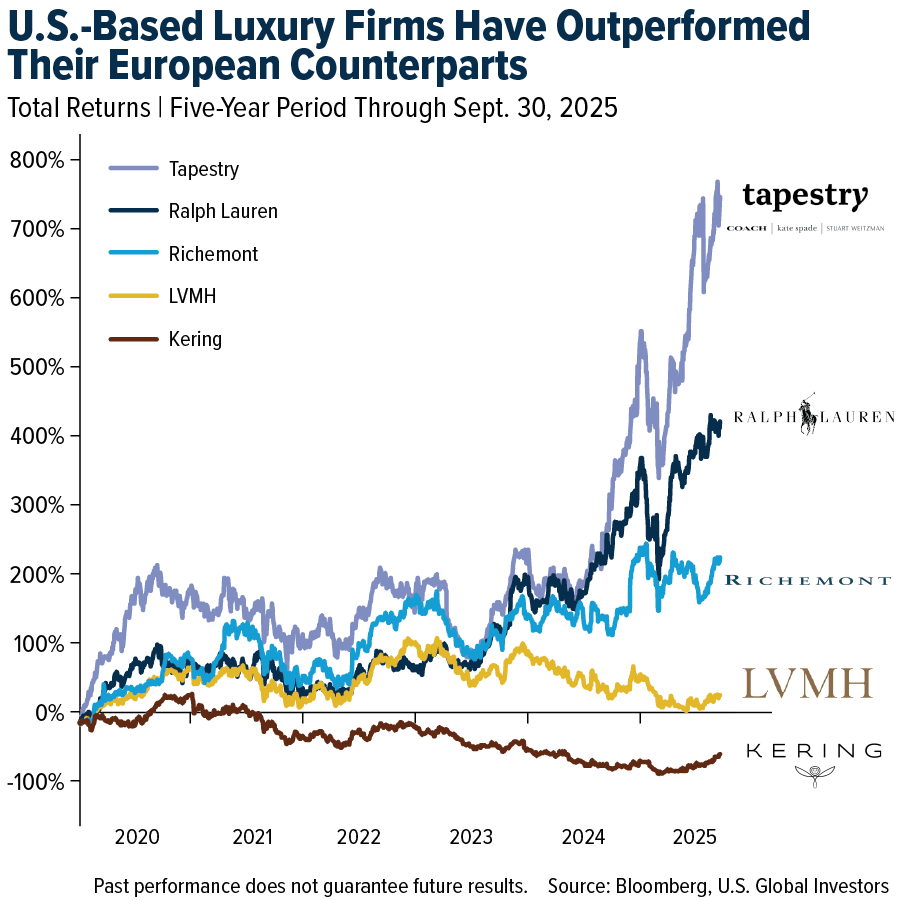

American Luxury Names Have Outperformed

While Europe and Asia wait for a rebound, the U.S. has quietly become luxury’s surprise growth engine. European brands have priced themselves aggressively in recent years, leaving daylight for American names to shine.

Those include Coach and Ralph Lauren. Once seen as “affordable luxury,” these companies have transformed into powerful global competitors, outpacing the better-known European houses over the past five years. Coach’s parent company, Tapestry, has outlined an ambitious “Amplify” strategy to return $4 billion to shareholders through 2028, while Ralph Lauren forecasts steady revenue growth and expanding margins.

Luxury Stocks on the Move

After a rocky first half of the year, luxury stocks are back on the move. LVMH, the world’s largest luxury group, recently reported improved trends in Asia and stable performance in the U.S., even as Europe felt some currency-related drag.

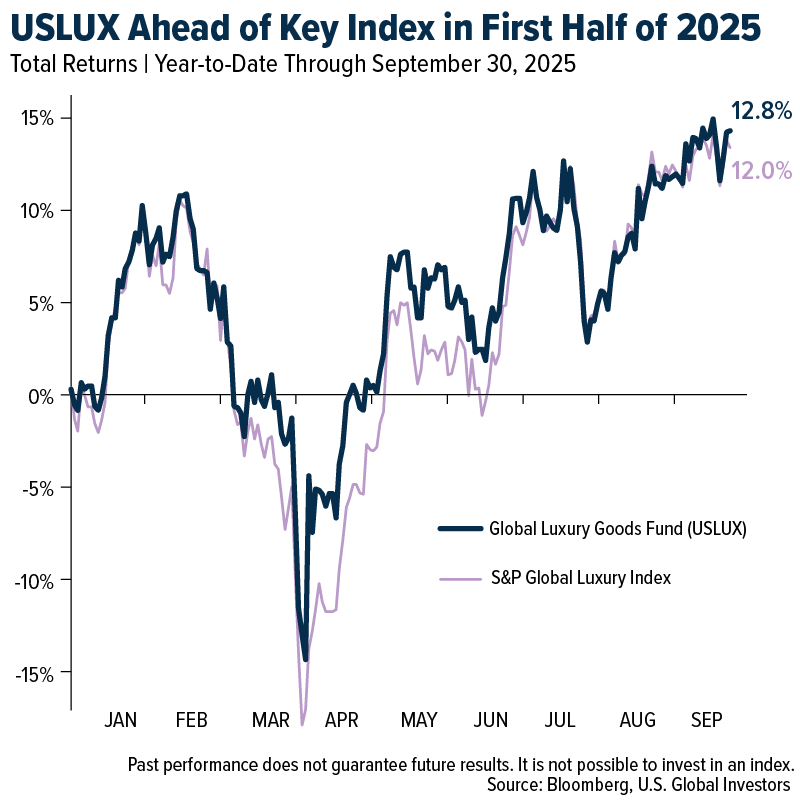

As of September 30, 2025, the Global Luxury Goods Fund (USLUX) was up 12.8% year-to-date, outpacing its benchmark, the S&P Global Luxury Index, which gained 12.0%.

Meet USLUX

We designed USLUX to give investors diversified access to companies across the luxury value chain, from fashion and jewelry to leisure and automobiles. We believe luxury’s cyclical dips present opportunities to accumulate shares in global franchises with household names, wide moats and loyal customers.

Morningstar has recognized USLUX with an overall rating of 4 stars (out of 47 funds in the mid-cap growth category) and a 5-star rating for the five-year period (out of 45 funds), based on risk-adjusted performance through September 30, 2025.

The fund’s holdings include many of the world’s most recognizable names, including not just LVMH, Hermès and Richemont but also Mercedes-Benz and Royal Caribbean Cruises, which benefits from affluent travelers.

Luxury Based on Love

When it comes to gold investing, I often talk about the Love Trade and Fear Trade. The yellow metal responds to both.

But luxury is the purest expression of the Love Trade: people buy these goods not out of fear but aspiration, pride and joy. That’s part of why I remain bullish on the industry.

To learn more about the Global Luxury Goods Fund (USLUX) and how you can participate in the long-term trend, click here!

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com. Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Past performance does not guarantee future results. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Past performance does not guarantee future results.

Total Annualized Returns as of 9/30/2025:

Performance data quoted above is historical. Past performance is no guarantee of future results. Results reflect the reinvestment of dividends and other earnings. For a portion of periods, the fund had expense limitations, without which returns would have been lower. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance does not include the effect of any direct fees described in the fund’s prospectus which, if applicable, would lower your total returns. Performance quoted for periods of one year or less is cumulative and not annualized. Obtain performance data current to the most recent month-end at www.usfunds.com or 1-800-US-FUNDS.

Related: Turbulence Ahead? Why Airline Investors Shouldn’t Panic Over the Shutdown