Trending

Japan holds over $1 trillion of US Treasury securities, making it the largest sovereign holder by a significant amount. Thus, the possibility has arisen that Japan might use its extensive holdings as leverage in tariff negotiations. Japanese Foreign Minister Katsunobu Kato said Japan has not made a decision on whether to include its holdings as part of the negotiations, but he did state the following:

It does exist as a card. Whether or not we use that card is a different decision.

Given Japan’s historical purchases and strong demand at recent Treasury auctions, Japan might opt to buy more Treasuries to signal goodwill and stabilize markets. Moreover, they could codify Treasury purchase or holdings minimums into an agreement. A deal could also be structured so that Japan agrees to hold more long-term debt as a percentage of its total holdings. The problem facing Japan with any requirements is that its Treasury holdings result from its currency market interventions. If Japan wished to support the yen versus the dollar, it would need to sell Treasuries and convert the dollars to yen.

Looking ahead, Japan may not be the only country able to use Treasury holdings as leverage in negotiations with the US. A deal with Japan or another major holder, as shown below, could be instrumental in other similar deals. Such deals involving Treasuries could be a creative way for the Treasury Department to drum up demand for its bonds, thus lowering its interest expenses.

Market Trading Update

Last week, we discussed that the market backdrop improved markedly following commentary from the White House that eased concerns about tariffs. To wit:

“The market rallied above the 20-DMA this past week as investors found some “silver linings” to the ongoing tariff dispute. Despite China saying “no negotiations” had started with the U.S., comments from both President Trump and Scott Bessent suggested that the Administration would “be nice” to China and that a “very good deal” could be done between the two countries. As we have noted previously, given the more extreme oversold condition of the market, any “good news” would allow investors to push stocks higher.”

This past week, two reports confirmed the economy is slowing. First, there was the weak GDP report, which showed growth of roughly one percent, after discounting the impact of the trade deficit. Secondly, while the employment number was higher than expected, the job growth trend is also slowing. However, those reports should have tempered market enthusiasm as they reduced hopes for Fed rate cuts. However, the market pushed higher as investors raced to jump back into “risk assets” as the market cleared initial resistance at the 20-DMA and reversed all of the “Liberation Day” losses.

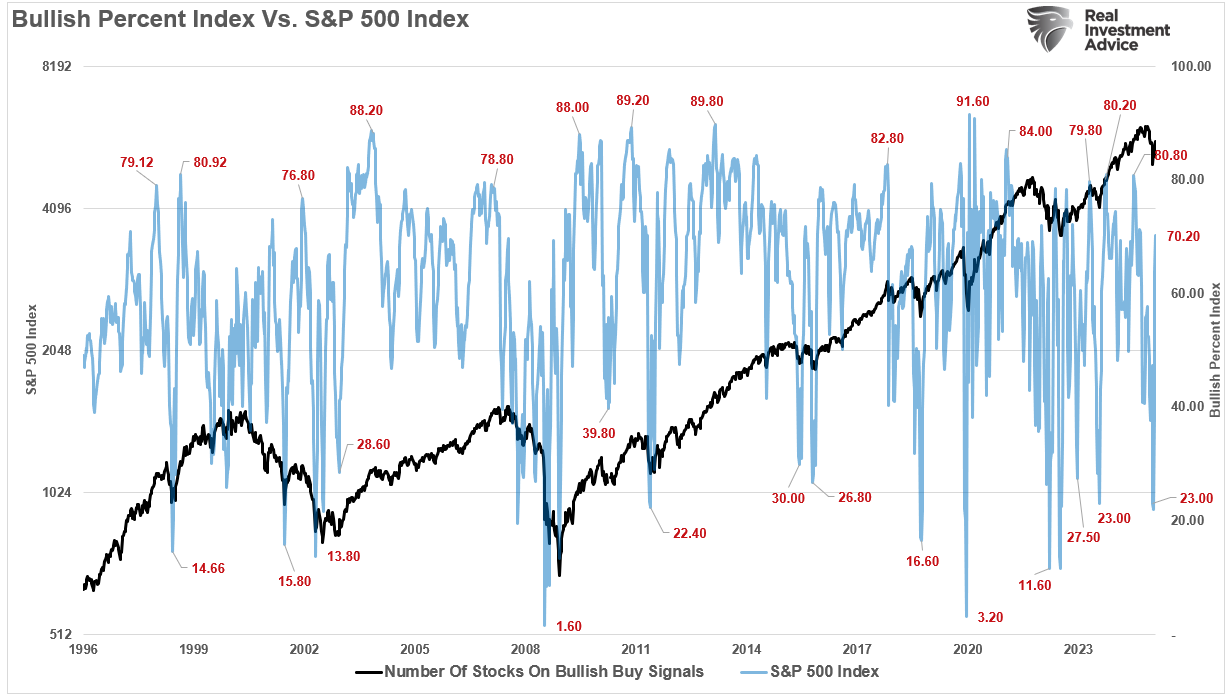

As we noted in “Hope In The Fear,” it would take much for the market to mount a sizeable rally given the extremely negative sentiment and positioning. Last week, the potential break in the China stalemate and non-recessionary data fed the “short-covering” rally, and pushed the index above the 50-DMA. That rally has also reversed the more extreme bearish sentiment and pushed the number of stocks on “bullish buy signals” back to 70%.

Notably, the rally from the recent lows, which has seen the market rise for 9 consecutive days, is one of the longest win streaks in 20 years.

What should be notable about that statement is that all “win streaks” end, eventually. That statement does not mean the markets will crash, but given that the rally has pushed markets back into short-term overbought conditions. Furthermore, the 200- and 100-DMA will provide notable resistance to the continuation of this rally without a pullback first. As we noted previously, many “trapped longs” will look to exit the market as we approach full recovery from the “tariff breakdown.”

Two Reasons To Be More Bullish

While bullish that the market has recovered 61.8% of its recent correction, a pullback should be expected. If you haven’t rebalanced allocations and reduced risk somewhat, now is the time. However, look for retracements to the 50-DMA, then the recent support, and finally the 20-DMA as areas to rebuild equity exposure. Lastly, move stop losses in portfolios up to the 20-DMA for trading positions.

There are two reasons to be more constructive about the market over the coming month. First, May tends to be a better-performing month following Presidential elections, while June tends to be weak (hence the Wall Street axiom “Sell In May.”)

Secondly, after a sharp reversal in April, which fueled the market selloff, share repurchases return next week as the bulk of the S&P 500 has announced earnings.

Optimism is returning to the market with economic data mainly remaining stable, earnings season coming in “better-than-expected,” and the near-term tariff threat residing. However, as noted, we suggest being somewhat cautious following the recent sharp advance and using short-term pullbacks to recent support to reduce hedges and increase equity risk as needed.

As we advance into 2025, we expect volatility to remain a constant companion. This will be a function of both the realization that economic growth is slowing and the repricing of valuations as earnings estimates are revised lower to meet reality.

Employment & The Week Ahead

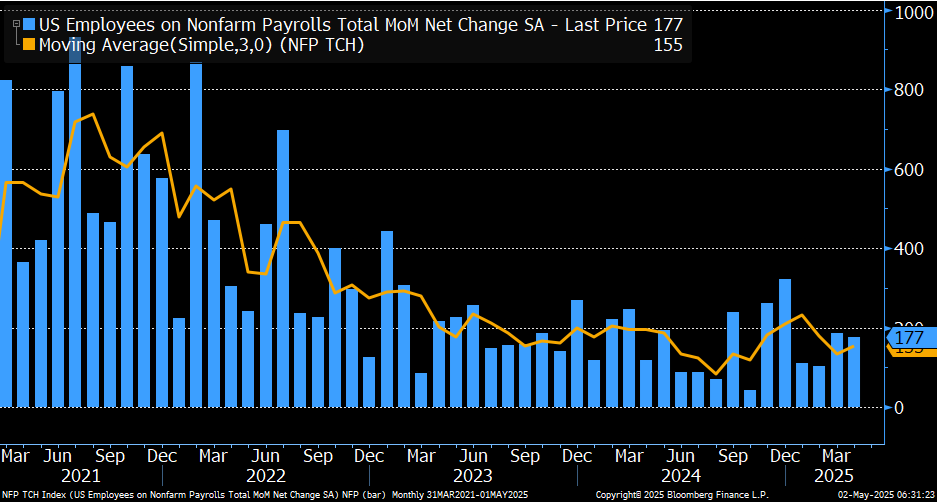

The economy added 177k jobs last month, about 35k above estimates. However, the two prior months were revised lower by 58k jobs. The unemployment rate was unchanged at 4.2%. As judged by this report, the labor market seems in good health, albeit slowing.

This morning, ISM will release its service sector survey. Estimates are for slight economic expansion at 50.8. Traders will focus on the prices and employment components to see if tariffs impact jobs and prices. The ISM survey is a little more real-time than most federal economic data, so it may be more of a market-mover event than is typical.

The big event this week will be the Fed’s FOMC rate decision. The market seems firmly in the camp that they will not cut rates. However, a reduction or end to QT is possible given some signs that liquidity is problematic. We think the market will key in on their discussion on whether they cut rates at the June meeting.

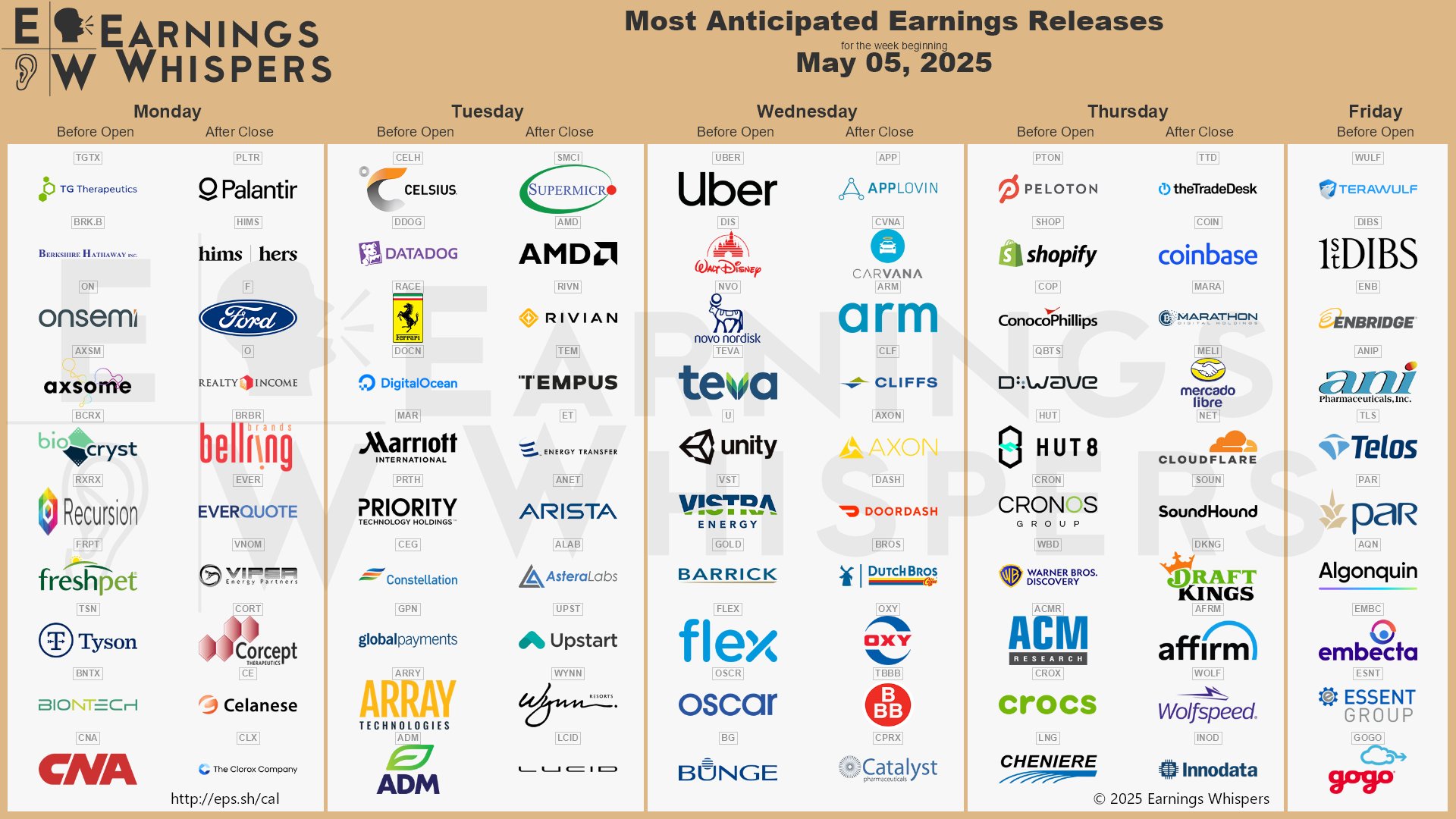

The second graphic below, courtesy of Earnings Whispers, shows a slew of earnings announcements on the docket. However, most of the largest companies have already reported. Therefore, we suspect that earnings will have less impact from now on.

The Awards You Never Get When Investing

In investing, success is often judged by numbers—returns on investment, percentage gains, and the ability to outperform benchmarks like the S&P 500. However, some investors frequently pursue a peculiar set of “awards” without realizing the pitfalls they embody. These unspoken goals, while tempting, rarely lead to sustainable investment success. If there were awards for some of these common but ill-advised behaviors, they would likely cause more harm than good. Here are some of the “investing awards” you’ll never receive, because chasing them isn’t worth the cost.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: What McDonald’s and Starbucks Are Telling Us About Consumer Confidence