Written by: Gabriela Santos and Anjali Balani

In mid-March, we argued that investing in emerging market (EM) equities still made sense due to: 1) high commodity prices, 2) China’s possible turnaround, and 3) discounted valuations. Since then, the Federal Reserve (Fed) has raised interest rates by 225bps, leaving investors wondering: is it a bad idea to invest in EM equities when the Fed is raising rates? Historically, EM equities have struggled in the first few months after the first rate hike, but subsequently recovered in the previous two tightening episodes. In the short-term, rate hikes may pressure EM equities, but not as much as investors may think due to: lower vulnerability to capital outflows, high interest rate differentials limiting outflows, and a greater dependence on China’s cycle versus the Fed. The broader macroeconomic backdrop also matters for EM performance: weak confidence in China and high commodity prices is not an easy environment to navigate. How to invest in EM is more important than ever in order to differentiate between winners and losers of these cyclical (and structural) themes.

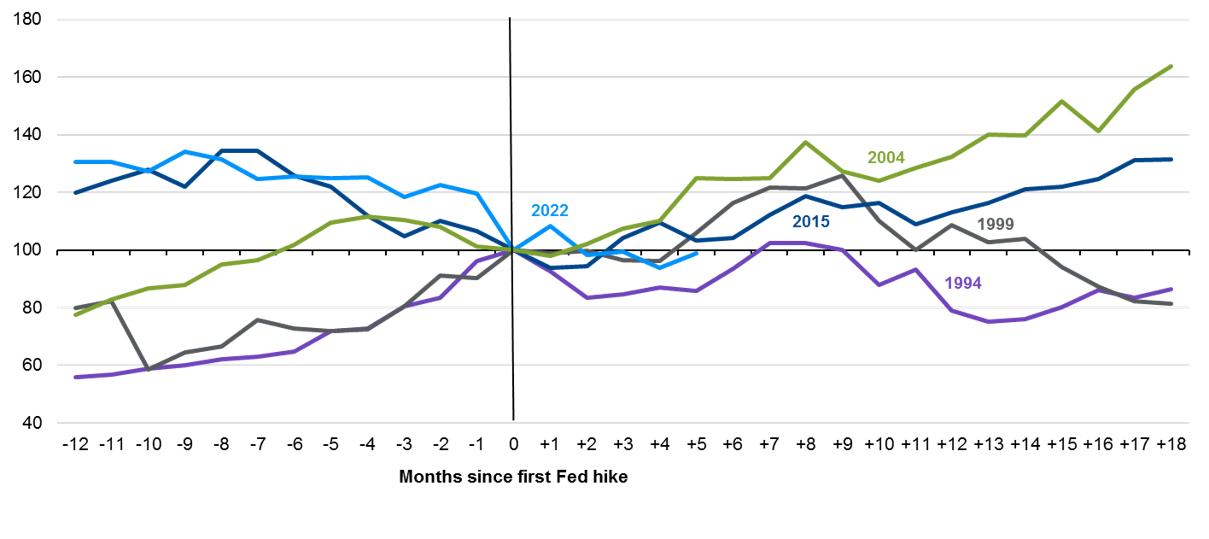

Five months after the first Fed rate hike, EM equities are down 1% in U.S. dollar price terms – actually representing 360bps of outperformance versus U.S. equities. Three variables explain EM’s resilience:

- Lower vulnerability to capital outflows vs. 2013’s “taper tantrum”: In 2013, the most fragile EM countries had a current account deficit of -3.3% versus -1.4% today.

- High interest rate differentials limiting outflows: Higher yielding (riskier) EM countries have been proactive about raising interest rates, leaving average interest rate differentials versus the U.S. at 681bps versus 578bps in 2013.

- Greater dependence on China’s cycle vs. the Fed: A decade ago, Chinese equities represented only 17% the equity universe versus 32% today.

With that said, the global backdrop is still challenging given questions about the strength of China’s economic acceleration and high commodity prices. Today, EM can be viewed across three lenses that impact our portfolio positioning within the International Equity portfolios: China, energy exporters, energy importers.

- China: Earnings revision ratios for China are already negative with a decline in earnings expected this year; thus, many of these risks are reflected in the outlook and in market performance year-to-date. While uncertainty surrounding regulations of the internet and tech sector remain, some idiosyncratic drivers make selective companies like Tencent attractive. In addition, we are closely monitoring areas that China is prioritizing, specifically within healthcare and enterprise software, where domestic players are quickly gaining market share globally.

- Energy exporters: High commodity prices are helping commodity exporting countries like Brazil and Indonesia overcome the headwinds of food inflation and slowing global growth. Indonesian banks like Bank Central Asia look attractive with strong demographic trends, including large underpenetrated markets for banking and far less foreign debt than previous cycles. The financial sector in Indonesia should also retain some of its attractiveness after the current energy market boom is over given the rise of a domestic consumption-led economy.

- Energy importers: High commodity prices have weighed on importing countries, such as Sri Lanka and Pakistan, which are more vulnerable to rising inflation, monetary tightening globally, and falling real incomes. India has been an exception; while it is a large importer of energy, India is emerging from an economic slump post the pandemic and the financial sector remains attractive with companies such as HDFC among our highest conviction names.

In addition to these cyclical considerations, emerging markets remain a rich and broad source of stock ideas tied to structural themes. We continue to find some best-in-class companies like TSMC, the world’s leading foundry, or Samsung, the lowest cost memory producer, that can hold their own versus developed market companies and provide high returns on capital and good governance. We also can access EM growth through developed market companies, like LVMH, L’Oréal, or even Hong-Kong listed insurer, AIA that generate a large source of their revenues from emerging markets. The cyclical backdrop for investing in EM will never be easy, but by focusing on stock selection and structural themes, investors can reap the rewards of investing in higher growth markets over the long-run.

EM equities may wobble the first few months after the first Fed hike, but the broader macro backdrop matters longer term

Index 100 = first Fed hike, MSCI Emerging Markets, U.S. dollars, price return

Source: MSCI, FactSet, J.P. Morgan Asset Management.

Data are as of August 30, 2022.