Trending

“Cash Is Trash” is a common theme as of late as inflation rages from the massive monetary interventions of 2020 and 2021. However, is “cash really trash?” Or, does cash still provide a valuable benefit to portfolios in terms of risk management?

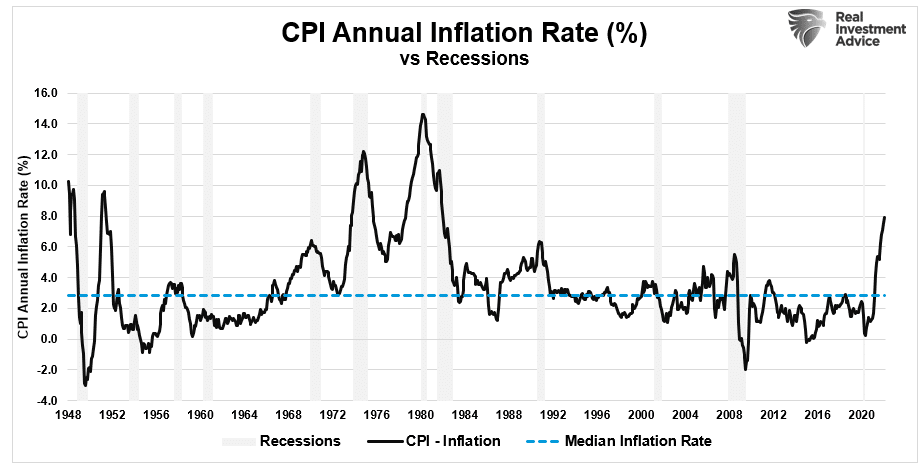

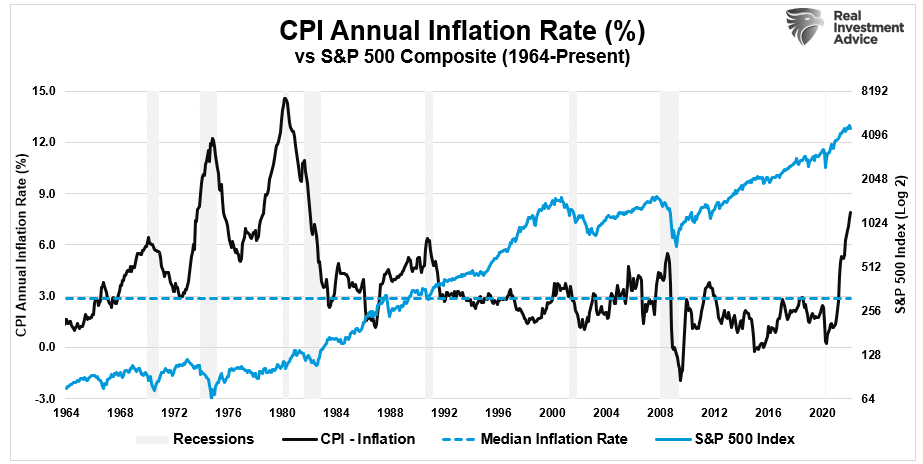

One of the common mistakes that individuals make regarding inflation is to assume that current inflationary pressures are now permanent. As shown below, while bouts of inflation can last for extended periods, it is never permanent. Notably, periods of “spiking” inflation lead to recessions and deflation, as consumption contracts and economic growth slows.

In the 60s-70s, rising inflation got offset by high savings rates, strong economic growth, and low household leverage. The current bout of inflation is the direct result of monetary interventions creating excess demand versus supply. However, while economic growth got an artificial bump, household savings are low, coupled with high household leverage.

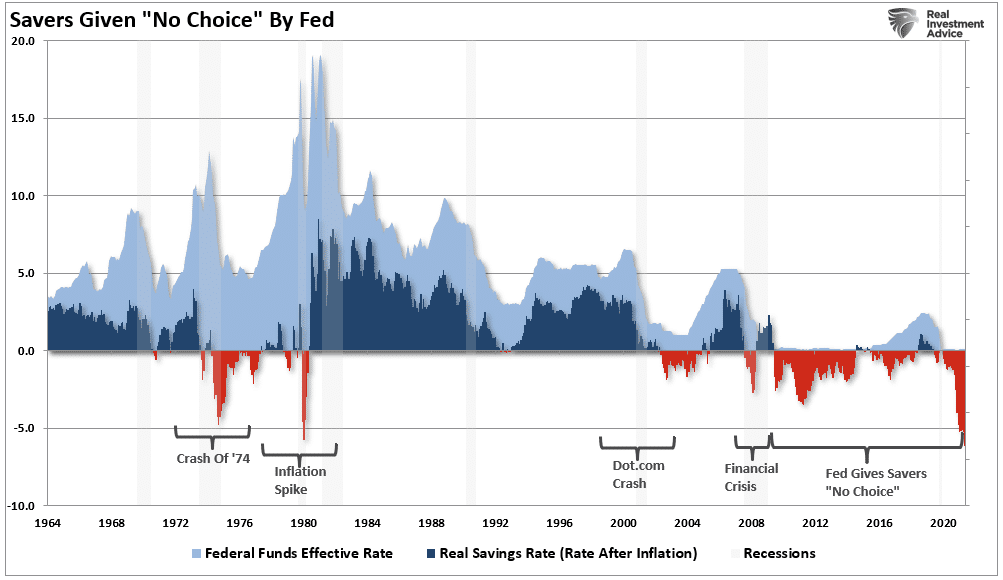

The consequence of a decade of monetary policy by the Fed forced “savers” into “risk assets” by pushing rates to zero.

With “zero interest rates” on savings, and inflation running nearly 8% as of this writing, it is no wonder that many believe “cash is trash.”

However, that isn’t necessarily true.

A Function Of Perspective

Let’s start with the obvious.

Inflation directly impacts your purchasing power parity over time. For example, I have savings in my bank account solely for the purchase of food and gas. Today, I can buy one tank of gas and a whole week of groceries to feed my family. If prices rise, I can still buy one tank of gas but only 4-days of groceries for the same amount of money.

In this example, my “savings” need to grow by a rate sufficient to pay for an additional 3-days of groceries.

Notably, this is how we tend to view our “savings” in their entirety.

However, there is an essential distinction regarding our investment accounts.

In our portfolio accounts (IRA’s, 401k’s, Taxable), the “savings” held ARE NOT for buying groceries, gas, or clothing. Those funds are there to invest in assets at times that we believe the rate of return on our capital will be higher than the inflation rate.

Notably, during periods of spiking inflation, asset prices tend to experience “deflation” and become cheaper, thereby increasing the purchasing power parity of our cash.

As is always the case when it comes to investing, capital preservation is always the most important. However, in periods of high inflation, holding “investment cash” can be a benefit as the purchasing power of that cash increases as asset prices decline.

When it comes to the “cash is trash” argument, the intended use is critical to the discussion.

Such brings me to something I discussed previously but is worth repeating.

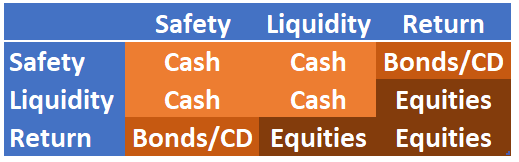

The 3-Components Of All Investments

In portfolio management, you can ONLY have 2-of-3 components of any investment or asset class: Safety, Liquidity & Return. The table below is the matrix of your options.

The takeaway is that cash is the only asset class that provides safety and liquidity. Obviously, “safety” comes at the cost of the return. However, during a period of capital destruction or inflation, the “safety” of the principal becomes the primary goal.

But what about other options?

- Fixed Annuities (Indexed) – safety and return, no liquidity.

- ETF’s – liquidity and return, no safety.

- Mutual Funds – liquidity and return, no safety.

- Real Estate – safety and return, no liquidity.

- Traded REIT’s – liquidity and return, no safety.

- Commodities – liquidity and return, no safety.

- Gold – liquidity and return, no safety.

You get the idea. No matter what you choose to invest in – you can only have 2-of-the-3 components. Such is a crucial and often overlooked consideration when determining portfolio construction and allocation. Notably, the mainstream media doesn’t tell you that “Liquidity” and “Safety” provide options.

I learned a long time ago that while a “rising tide lifts all boats,” eventually, the “tide recedes.” I made one simple adjustment to my portfolio management over the years, which has served me well. When risks begin to outweigh the potential for reward, I raise cash.

The great thing about holding extra cash is that if I’m wrong, I simply make the proper adjustments to increase the risk in my portfolios. However, if I am right, I protect investment capital from destruction and spend far less time ‘getting back to even.’ Despite media commentary to the contrary, regaining losses is not an investment strategy.

8-Reasons To Hold Cash

1) We are speculators, not investors. We buy pieces of paper at one price with hopes of selling at a higher price. Such is speculation in its purest form. When risk outweighs rewards, cash is a good option.

2) 80% of stocks move in the direction of the market. If the market is falling, regardless of the fundamentals, most stocks will also decline.

3) The best traders understand the value of cash. From Jesse Livermore to Gerald Loeb, each believed in “buying low and selling high.” If you “sell high,” you have raised cash to “buy low.”

4) Roughly 90% of what we think about investing is wrong. Two 50% declines since 2000 should have taught us to respect investment risks.

5) 80% of individual traders lose money over ANY 10-year period. Why? Investor psychology, emotional biases, lack of capital, etc. Repeated studies by Dalbar prove this.

6) Raising cash is often a better hedge than shorting. While shorting the market, or a position, to hedge risk in a portfolio is reasonable, it also merely transfers the “risk of being wrong” from one side of the ledger to the other. Cash protects capital and eliminates risk.

7) You can’t “buy low” if you don’t have anything to “buy with.” While the media chastises individuals for holding cash, it should be somewhat evident that you can’t take advantage of opportunities without cash.

8) Cash protects against forced liquidations. One of the biggest problems for Americans is a lack of cash to meet emergencies. Having a cash cushion allows for handling life’s “curve-balls” without being forced to liquidate retirement plans. Layoffs, employment changes, etc., are economically driven and tend to occur with downturns that coincide with market losses. Having cash allows you to weather the storms.

Conclusion

I want to stress that I am not talking about being 100% in cash.

Being “all-in” or “all-out” of the market is never wise in the portfolio management process. While you may “time” the exit or entry perfectly once or twice, it is an impossibility to replicate it over time successfully. However, you can successfully manage risk by increasing cash during uncertainty or increasing risk when the opportunity is present.

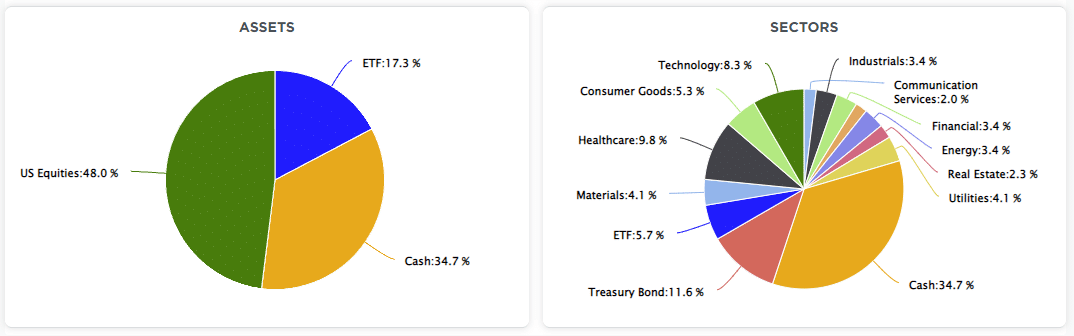

As shown, we are holding higher cash levels because of the current uncertainty. That cash provides both stability and opportunity.

With the geopolitical, fundamental, and economic backdrop becoming increasingly hostile toward investors in the future, understanding the value of cash as a “hedge” against loss becomes dramatically more important.

For us, “cash is not trash” regarding portfolio and risk management.

But, since Wall Street doesn’t make fees on cash, maybe there is another reason they are so adamant you remain invested all the time.

Just something to consider.

Related: Recession Risk is Rising Rapidly